“Listen to many, speak to few.”

-William Shakespeare

I love to read, write, and rant. But, other than our top institutional customers and my research team, I speak to few during a typical market day. While I love my best friend (my brother Ryan), our phone conversations are usually 140 words or less.

If you read voraciously, you can listen to the #history of many. If you create the right contra-streams on Twitter, you can watch the sentiment of the crowd. If you embrace uncertainty of timing market sentiment, you’ll always be prepared to change your mind.

But macro markets don’t care about what I think about all of that. Markets are non-linear. They are structured to pulverize the largest number of people at the most inconvenient time. So listen to Mr. Macro Market’s signals very closely. He’s a front-runner of risk.

Back to the Global Macro Grind…

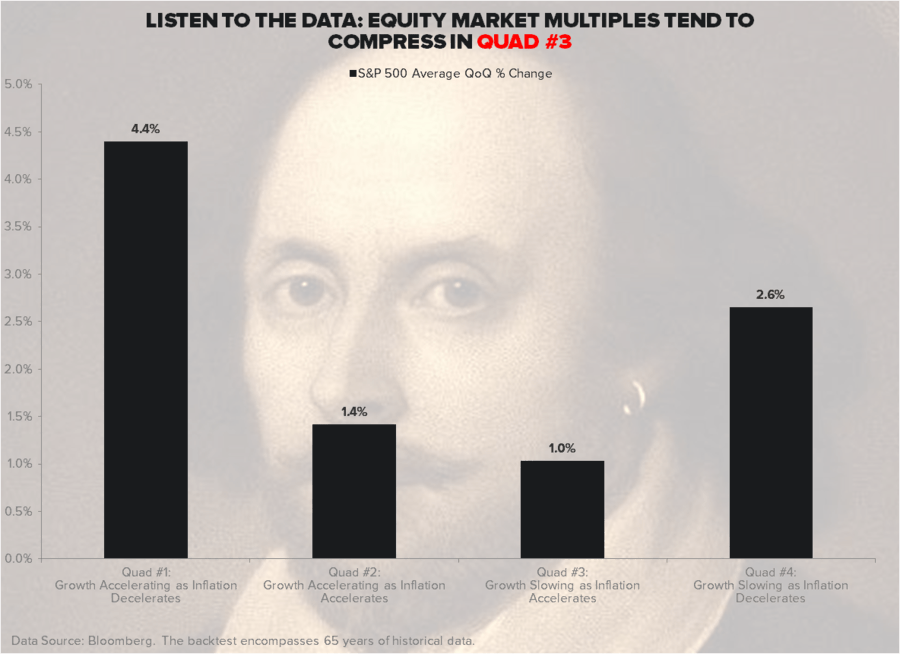

With Japanese, Chinese, and American #GrowthSlowing (oh, and Russia crashing to -22.6% YTD), what could possibly go wrong? Rather than have some character tell you “the market is cheap”, you can listen to #history’s lesson on that:

1. When Inflation Accelerates, and

2. Real (inflation adjusted) Growth slows…

You get:

A) Multiple compression in Equities

B) Multiple expansion in Bonds

And, since:

1. #OldWall consensus is still looking for implied multiple expansion (to 17-18x EPS) for the SP500 this yr

2. #OldWall consensus is still looking for implied multiple compression (higher bond yields) for Treasuries this yr

You have yourself basically the opposite consensus to listen to that you had only 1 year ago today. While last year seems like forever ago to a consensus that missed US #GrowthAccelerating, on March 12, 2013:

1. The Dow and SP500 were at 14,450 and 1552, respectively

2. The 10yr US Treasury Yield was at 1.90% (tracking towards its all-time low of 1.7% in April)

Sentiment then wasn’t off by a little bit – it was off by a country mile.

By year-end of 2013:

1. The Dow and SP500 closed at 16,576 and 1848, respectively

2. The 10yr US Treasury Yield has its biggest % move in 50yrs (closing the yr at 3.03%)

Fast-forward to today, with the US Dollar on its YTD lows and #InflationAccelerating, the Dow Jones is actually DOWN -0.6% YTD and US 10yr Treasury Yield is DOWN -28 basis points to 2.75%. But the SP500 is up a whopping +1.0% (plus or minus whatever happens today), so let’s turn on the tube and keep talking up what was supposed to be a US Equity multiple expansion party!

If you’ve studied the #history of debtor nations devaluing their currencies in order to inflate asset prices, you’ll note that the non-government people living in those countries generally develop miserable sentiment. There’s this thing called the Misery Index (inflation + unemployment). This morning, Japan’s Misery Index hit a 33 year high.

So, let’s encourage consensus to keep cheering on a Policy to Inflate but call it by any other name. This is really the only way to envision being really right versus what you read and hear from consensus every day (consensus #OldWall estimates are still looking for both US and Global GDP to accelerate sequentially to new multi-year highs, and for inflation to be benign).

A few other mathematical realities we’ve back-tested as relevant sentiment checks are:

1. Front-month Equity Fear (VIX) versus the term structure of the VIX curve

2. The II Bull/Bear Spread

This morning front-month VIX has A) established yet another higher-low on our TREND duration and B) the term structure of implied volatility is nowhere near as fearful as it was 12-15 months ago.

On the II Bull/Bear Spread, 2013 bears were eviscerated. On today’s reading, Bulls are +3,770 basis points (55.1%) higher than the Bears (17.4%). That’s not the all-time high in terms of the Bull/Bear spread – but December 31st, 2013 was (when the Dow topped).

I’m not saying I’m nailing everything macro this year. I’m simply saying what very few want to listen to when complacency sets in – and that’s that the US stock market “is cheap, multiple expansion” bulls might get nailed in the coming months.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.58-2.80%

SPX 1

Nikkei 144

VIX 13.22-15.72

USD 79.39-79.98

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer