Higher hold contributed to the record setting February but not as much as originally thought.

We estimate above normal hold contributed only 4% of the 40% YoY growth and less than 1% if you normalize both Februarys. No way around it, February was a blowout which is very strange considering the relative weakness of January, weakness that the 10 day Chinese New Year shift cannot explain alone. In the last few years, we’ve heard that the CNY celebration is becoming less of a seasonal factor. Remember that January grew only 7% on only slightly lower hold. CNY occurred on 1/31 this year vs 2/10 last year.

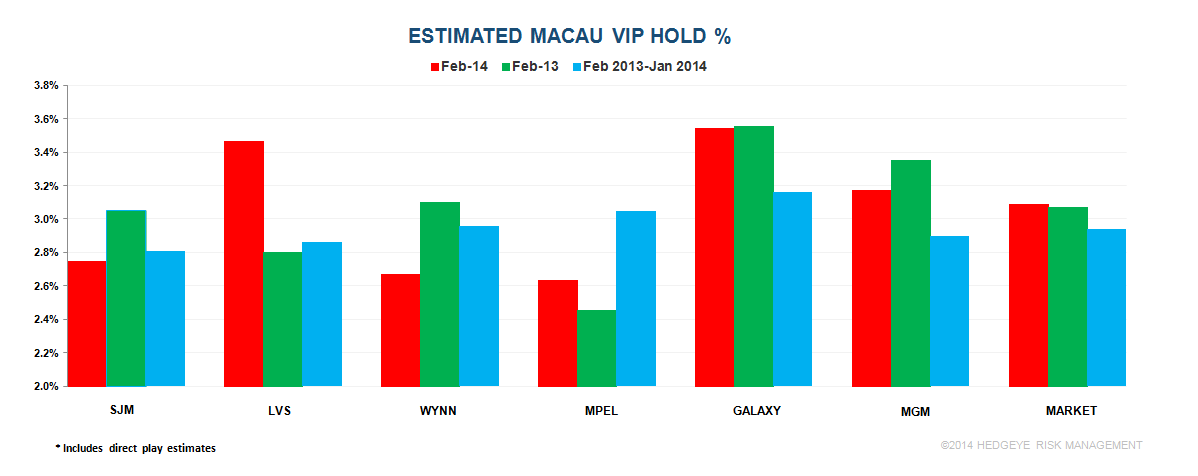

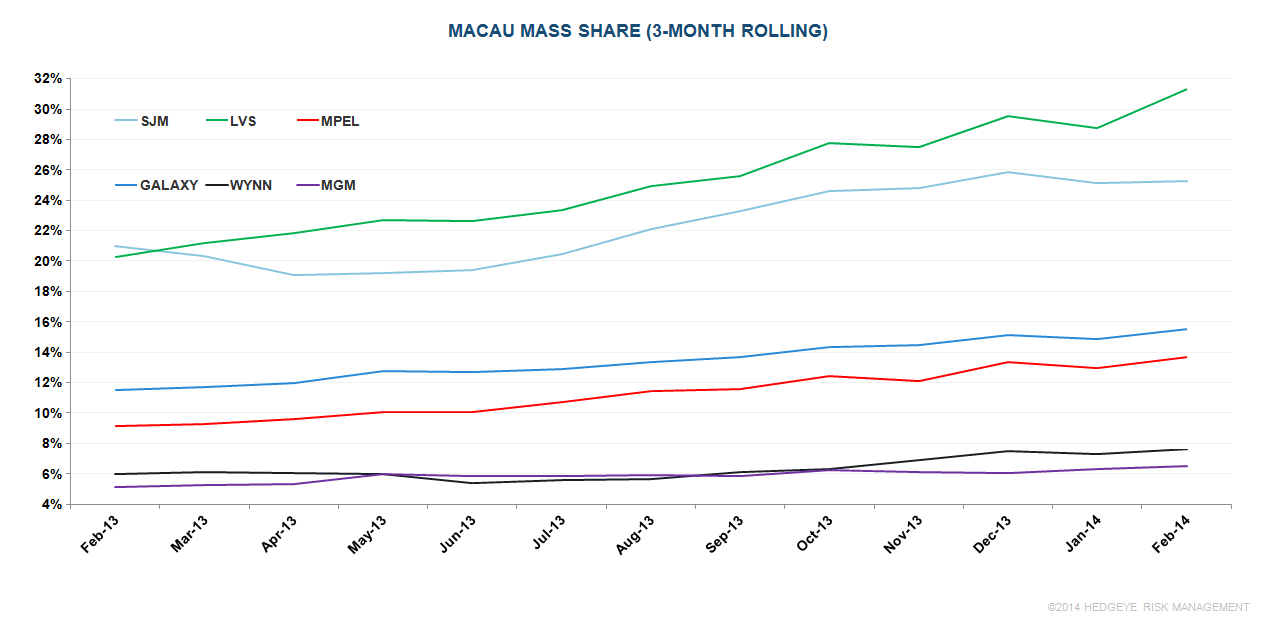

As we already knew, LVS was the big winner in February and not surprisingly, some of the upside was hold related. However, LVS gained Mass share and Rolling Chip volume share as well. As we suspected, Wynn Macau got clocked in terms of luck but Mass and RC share was better than trend. Surprisingly, MGM actually held high but market share was well below trend. MPEL held the lowest in February, which drove GGR share to the lowest level since Dec 2009.

Market Observations:

- Mass drove most of the growth with revenue up 51% YoY in February and up 38% combined for January and February.

- While VIP revenue climbed 37% in February, January’s VIP actually declined 1% holding back combined Jan/Feb revenues to +18%.

- Even slots performed well, although not nearly as strong as Mass growth, up 24%. Slot growth was the highest in almost 2 years.

- The March comparison is very difficult (1 and 2yr) and we are only projecting 13-17% growth

LVS: Terrific month and it wasn’t just high hold

- 64% GGR growth YoY in February led the market

- 68% Mass growth led the market

- If hold had been normal, YoY growth would’ve been 49%. Normalizing hold for both Februarys yields YoY growth of 44%, which would’ve still led the market on a hold adjusted basis

- LVS’s GGR, Mass, RC, and slot revenue share all increased relative to recent trend

- QTD, LVS’s GGR is up 40%

WYNN: Solid month excluding the hold impact

- While January GGR was down 13%, Wynn Macau rebounded to up 29% in February

- Mass revenue grew 48% YoY – the 2nd highest growth rate in 2 ½ years

- While VIP revenue grew 24%, RC climbed 48% as hold was 20-30bps below normal

- QTD, WYNN’s GGR has grown 9%

MGM: Not one of MGM’s finest months

- GGR share fell to its lowest level in almost a year and Mass fell to a record low as well

- Despite lucky play from its patrons, MGM’s RC share was at its lowest in a year and a half

- MGM held high for the 2nd consecutive month

- YoY GGR growth of 25% was the 2nd lowest in the market next to SJM

- QTD MGM’s GGR is up 29% but with constant hold the growth rate drops to 22%

MPEL: CoD mass strength offset relative VIP bad luck

- GGR share hit its lowest level since December 2009 at 12%

- Low VIP hold was mostly to blame at 2.63% (inclusive of direct play) but the hold comp was low as well (2.45%)

- Mass share fell 0.3% bps MoM to 13.2%

- VIP volume share grew 0.6% bps MoM to 12%, highest level since Sept 2013

Galaxy: Another strong month with share at a recent high

- Galaxy held well above normal but exactly in line with last year

- Mass share was in line with trend while RC share was slightly above trend

- YoY GGR growth of 60% was 2nd to only LVS

- QTD GGR grew 38%