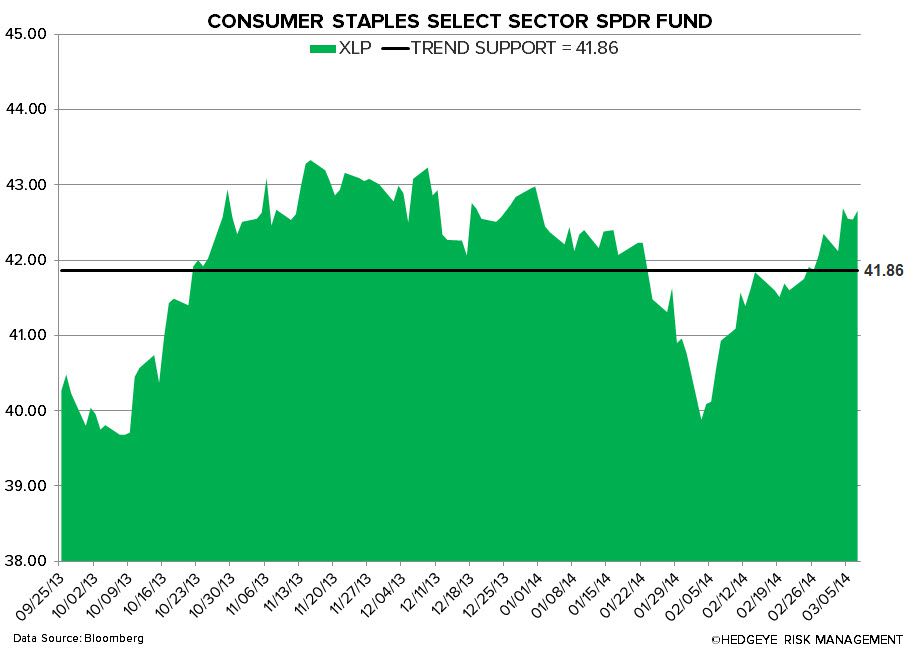

Consumer Staples mildly underperformed the broader market last week, rising +0.7% versus the S&P500 at +1.0%. XLP is down -0.7% year-to-date.

From a quantitative set-up the sector moved to bullish immediate term TRADE and intermediate term TREND durations this week, our language for a bullish medium term sector outlook. This is a material change compared to year-to-date in which it has traded bearish TRADE and TREND.

We continue to believe that the sector is facing numerous headwinds, including:

- U.S. consumption growth is slowing as inflation rises, in-line with the Macro team’s 1Q14 theme of #InflationAccelerating

- The economies and currencies of the emerging market – once the sector’s greatest growth engine – remain weak with the prospect of higher inflation in 2014 eroding real growth

- The sector is loaded with a premium valuation (P/E of 19.4x)

- Less sector Yield Chasing as Fed continues its tapering program

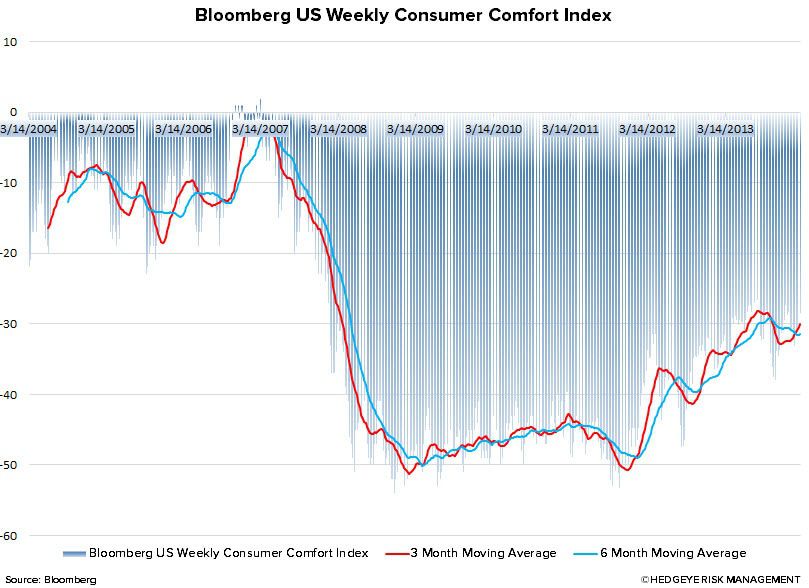

- The high frequency Bloomberg weekly U.S. Consumer Comfort Index has not seen any real improvement over the past 6 months, but expanded to -28.5 versus -28.6 in the prior week

There are a number of companies presenting at consumer conference this week (more below). If you missed our Best Idea Call on Lorillard on March 4th you can click below for a replay:

Podcast: CLICK HERE

Presentation: CLICK HERE

***A supplemental expert report on menthol by a top Washington, DC law firm involved in tobacco public policy is available by request***

Top 5 Week-over-Week Divergent Performances:

Positive Divergence: LO +8.0%; BNNY +5.9%; HAIN +5.5%; RAI +5.4%; BF/B +5.1%

Negative Divergence: NUS -8.6%; HLF -2.8%; SJM -2.5%; NWL -2.5%; AVP -1.9%

Last Week’s Research Notes

Recent News Flow

RAI & LO - last Monday, RAI was rumored to be interested in acquiring LO. The rumor sent LO’s stock soaring. As we discussed in our Best Idea Call on Lorillard, we’re uncertain if the deal would go through given anti-trust concerns. A combined RAI + LO would own 67% of the U.S. menthol market, and make it the second largest U.S. tobacco company, behind PM.

Over the weekend there were also rumors that BAT may buy the 58% of RAI it doesn’t already own. We think the uptick in news flow in the tobacco space is additive to our fundamental long call on LO.

BF/B – Brown Foreman reported Q3 earnings on 3/5, beating consensus estimates of $0.75 by 7 cents, and top-line met consensus at $1.08B.

Events This Week (in EST):

Wednesday (3/12)

RBC Capital Markets Consumer & Retail Conference: ENR (8:30am); CPB (8:30am); RAI (11:30am)

Goldman Sachs Agribusiness Conference: BG (11:30am); SAFM (1:50pm); TSN (2:50pm)

UBS Global Consumer Conference: DPS (8:50am)

Bank of America Merrill Lynch Consumer & Retail Conference: HAIN (11am)

Thursday (3/13)

RBC Capital Markets Consumer & Retail Conference: TSN (8am); BNNY (9am); HAIN (10am); NWL (11am)

UBS Global Consumer Conference: CL (8:50am)

Matt Hedrick

Food, Beverage, Tobacco, and Alcohol

Howard Penney

Household Products

(o)

Quantitative Setup

In the charts below we look at the largest companies by market cap in the Consumer Staples space from both a quantitative perspective and fundamental aspect where we can offer one. As you will see over time, sometimes our fundamental view does not align with the quantitative setup (though not often).

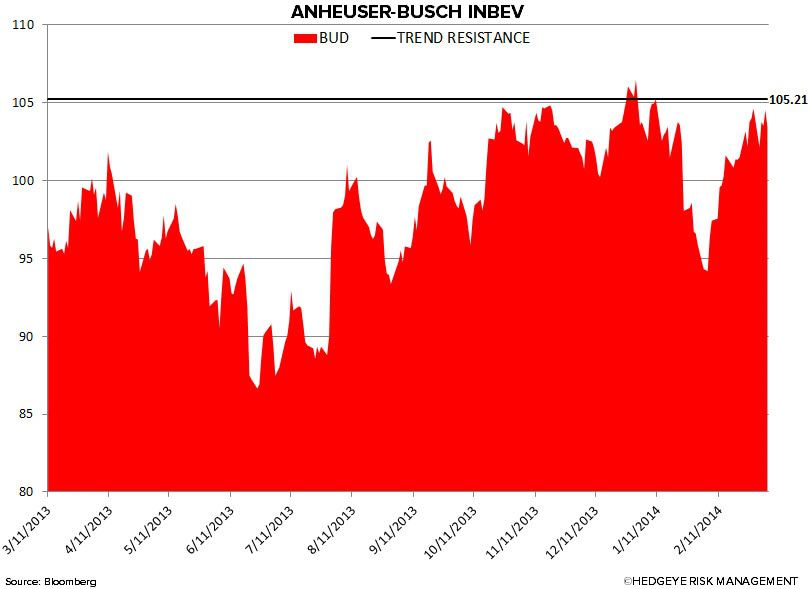

BUD – trying to breakout back above its TREND line of 105.21 resistance but not getting it done – rally to lower-highs has been on weak volume signals too

DEO – looks a lot like BUD, but worse; bearish TREND resistance firmly intact up at 127.21

KO – still one of the ugliest big cap quantitative setups in America; TREND resistance remains intact up at 39.81

PEP – beta chase was on @Pepsi last week, but on really weak volume signals; stock would need to close > 82.29 to go bullish TREND

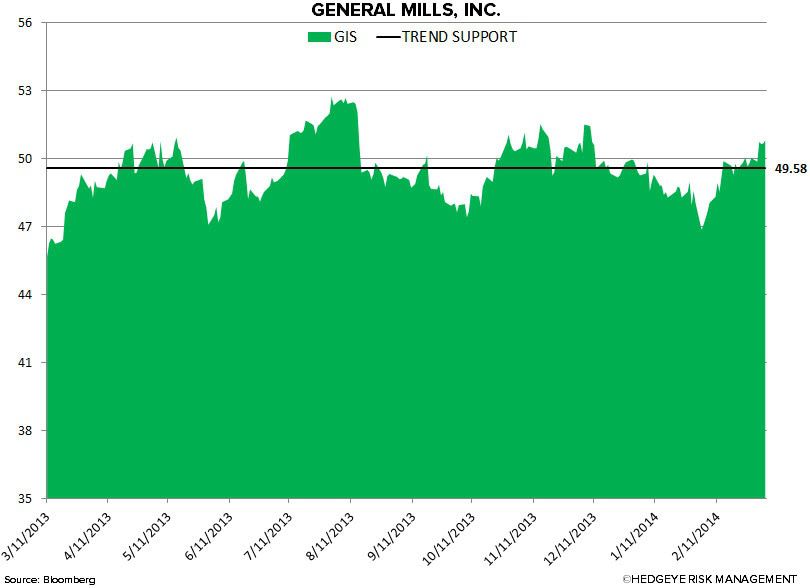

GIS – our risk management signal sniffed this one out when it signaled a bearish to bullish TREND reversal 3 weeks ago; what was TREND resistance is now support at 49.58

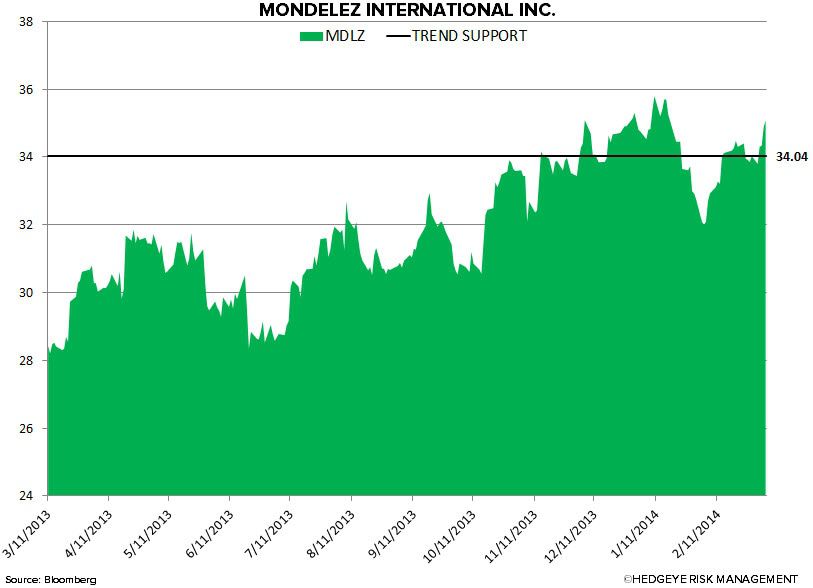

MDLZ – solid breakout confirming bullish TREND this week; stock needs to hold 34.04 for it to remain bullish TREND

KMB – still the best looking combined quant/research setup on this list; TREND support firmly intact down at 105.49

PG – almost looks as bad as KO (which is really bad); @Hedgeye TREND resistance = 81.05

MO – starting to improve from the thralls of bearishness in early FEB; if the stock can hold 36.39, it has a shot at going bullish TREND in our model

PM – does not look at all like MO; bearish TREND is pervasive for PM (resistance = 83.67)