This note was originally published March 06, 2014 at 08:08 in Morning Newsletter

“What’s in a name? That which we call a rose by any other name would smell as sweet.” -William Shakespeare

The big picture

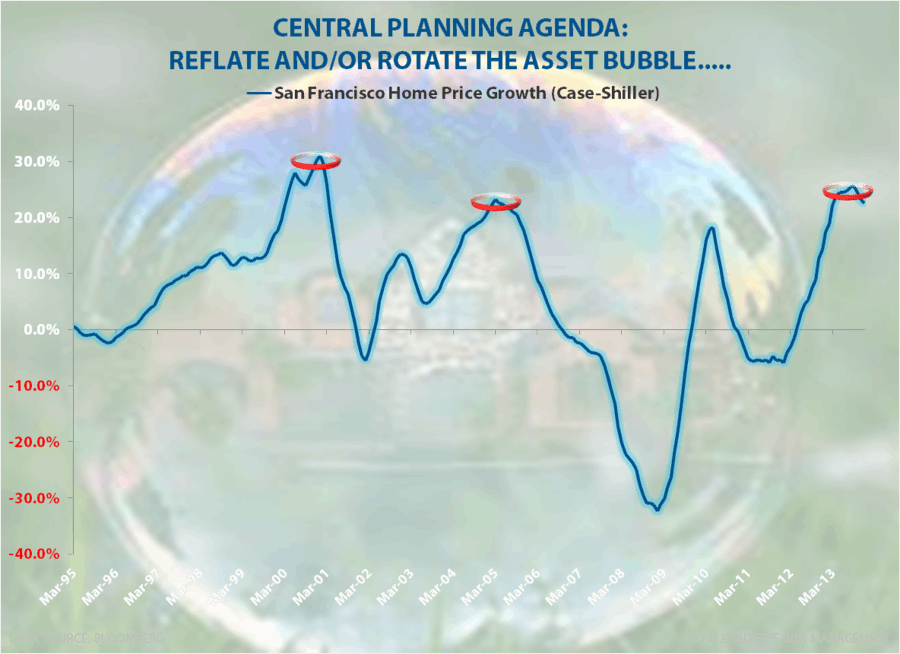

What’s in a bubble?

I’ve been channeling my inner 1999 for the last 3-days in California. I’ve done Los Angeles, San Diego, and San Francisco. And while it would be cute to tell you that I can actually smell a bubble, these types of things don’t have a particular scent.

At the all-time highs, they just look sweet.

Macro grind

All-time highs? Yep. It’s not just Yelp (YELP) and Facebook (FB). It’s Barney Frank’s American Housing dream. The all-time highs in the largest component of American cost of living are here. It’s called rent.

Oh, you don’t rent? Ok, you’re like me then. You’re big time – you own. But don’t confuse the 20% of us who are long asset price inflation with the rest of them (80% of Americans) who get pulverized by Policies to Inflate. The cost to live in this country has never been bubblier.

What’s in the cost of living?

- Shelter

- Food

- Transportation

Unless you’re like the “folks” in Washington who take car service to work, you have to put gas in the transportation thing too. And if you can’t afford a car, you can always save some money and take the bus, or walk…

What’s in the all-time high in American “inequality”?

- The Housing Bubble

- The Commodity Bubble

- The Bond Bubble

One by one, central planners at the Fed blow these bubbles up so big that, like Jim Carey in The Truman Show, we start to live inside them. There’s an effervescence to that, I guess.

Or at least that’s what Oaktree’s Howard Marks said in our back to back presentations at the CFA Society’s Annual Forecast Dinner in San Diego on Monday night. He called the cov-light-pik-toggle-bond thing being “back” – an “effervescent bubble.”

As we went back and forth in the Q&A part of the event, Marks made an astute observation about real-world life. The average American has $20,000 in post tax income, but spends approximately $22,000 a year.

So, if you ramp up the Top 3 things Americans have to pay for (if they don’t pay for their kids to go to school), the Bush/Obama/Bernanke/Yellen Policy to Inflate should drive cost of living up to say $25,000-30,000/year. That’s why the US Savings (as a % of disposable income) is retracing its 2008 crisis lows. Like their government, Americans once again have to borrow to spend.

In other news, inflation slowed US consumption growth again in February:

- USA’s ISM Services report for FEB (reported yesterday) slowed to its lowest level since FEB of 2010

- The Employment component of the ISM Services Series dropped < 50 (largest m/m drop since NOV 2008)

- US Services PMI (Markit data series) slowed from 56.7 in JAN to 53.3 in FEB

No worries though, it’s all “weather.”

If you want to join the Federal Reserve and believe that (and tell the 80% that inflation doesn’t slow growth), you can start turning on the Weather Channel and buying the all-time highs in social media every day they forecast yesterday’s sunny news.

I’ll be selling stocks (and buying Commodities, Bonds, and Foreign Currencies) into that. Because, like in Q1 of 2011, Down Dollar and Down Rates were signaling a US consumption growth slowdown inasmuch as they did in Q1 of 2008.

As for retracing my California travels of 1999, Q1 of 2000 wasn’t exactly the time to be wearing rose colored glasses either.

Asset Allocation

- CASH: 31%

- US EQUITIES: 3%

- INTL EQUITIES: 10%

- COMMODITIES: 16%

- FIXED INCOME: 20%

- INTL CURRENCIES: 20%

Our levels

Our immediate-term Macro Risk Ranges are now:

UST 10yr Yield 2.59-2.75%

SPX 1848-1879

VIX 13.01-15.64

USD 79.86-80.43

Brent 107.31-110.02

Gold 1319-1351

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer