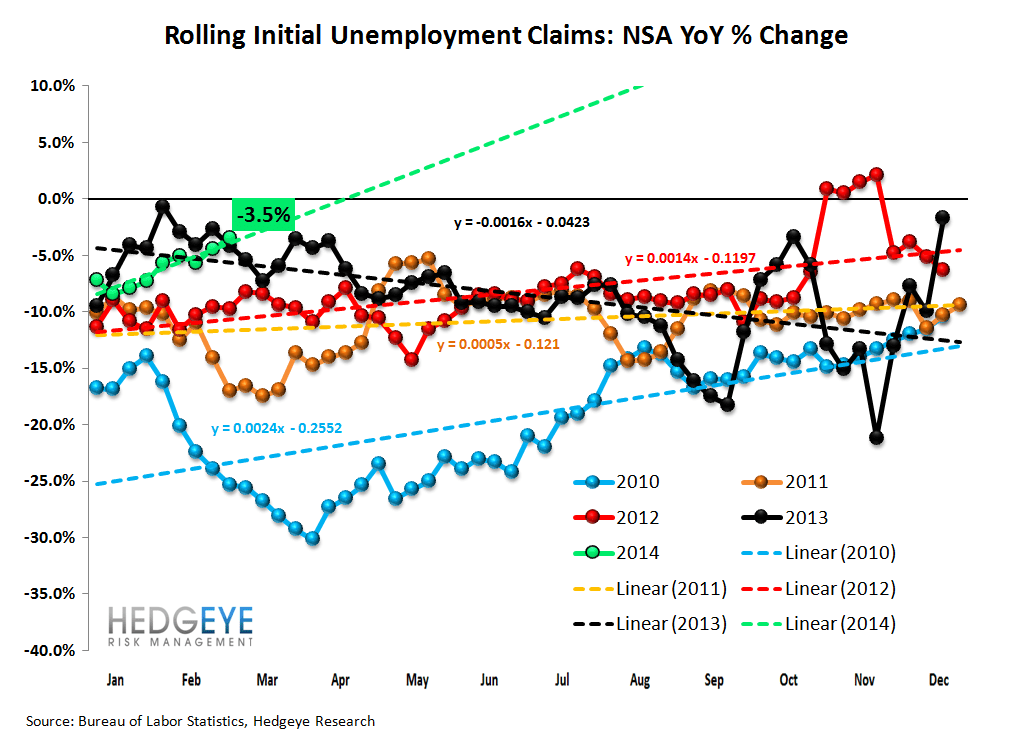

The Labor Market Continues its YTD Cooling Trend

Labor market data continued its deteriorating trend this past week, bringing to almost seven the number of consecutive weeks this has been happening. Notwithstanding a brief studder-step two weeks ago the progression of the labor market data has been progressively negative every week for almost the last two months, or, alternatively, since the start of the year. As a reminder, we look at the year-over-year rate of change in the rolling NSA initial claims. Specifically, we look for inflections in the trendline rate of improvement as the series naturally converges towards zero as the economy reaches full steam. Here are the last seven data points with the most recent data point first: -3.5%, -4.4%, -5.6%, -5.1%, -5.7%, -7.3%, -7.9%, -8.5%. Since we're looking at the rate of change in year-over-year initial jobless claims a more negative number is better as it implies a faster rate of improvement.

To be clear, we're not yet sounding the alarm on the labor market, but it's important to note that the rate of improvement is decelerating steadily and if that trend continues then we could see, in the not too distant future, the labor market reverse course, i.e. claims begin to rise.

The Numbers

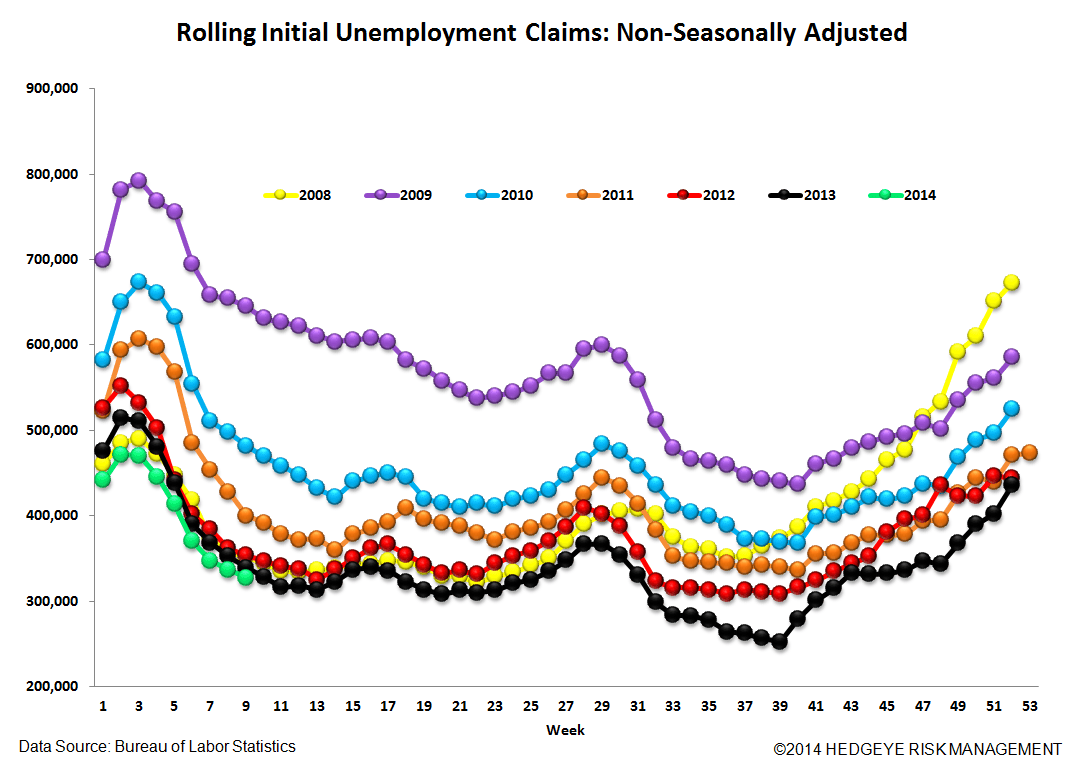

Prior to revision, initial jobless claims fell 25k to 323k from 348k WoW, as the prior week's number was revised up by 1k to 349k.

The headline (unrevised) number shows claims were lower by 26k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -2k WoW to 336.25k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -3.5% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -4.4%

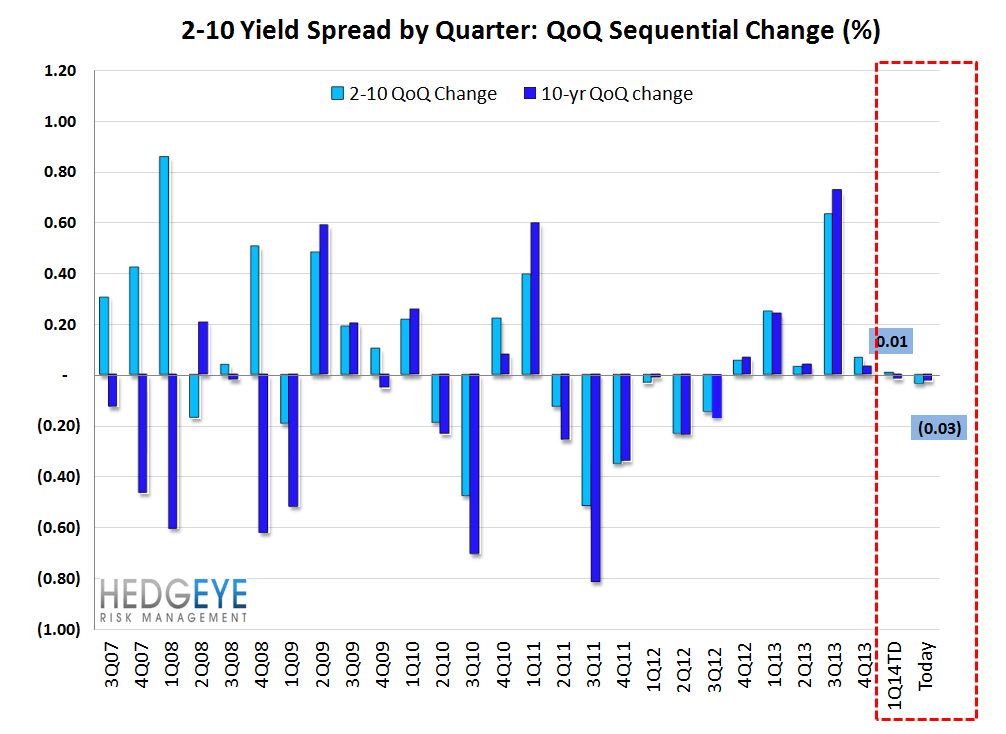

Yield Spreads

The 2-10 spread rose 4 basis points WoW to 238 bps. 1Q14TD, the 2-10 spread is averaging 242 bps, which is higher by 1 bps relative to 4Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT