Editor’s Note: This is part of a research piece originally published on March, 5 2014 at 3:40 PM in Gaming, Lodging & Leisure. For more information on how Hedgeye can help you, click here.

Have you been outside lately? It’s been a brutal winter for most Americans. But now, with snowstorms abating, are consumers still booking vacation cruises to sunnier destinations?

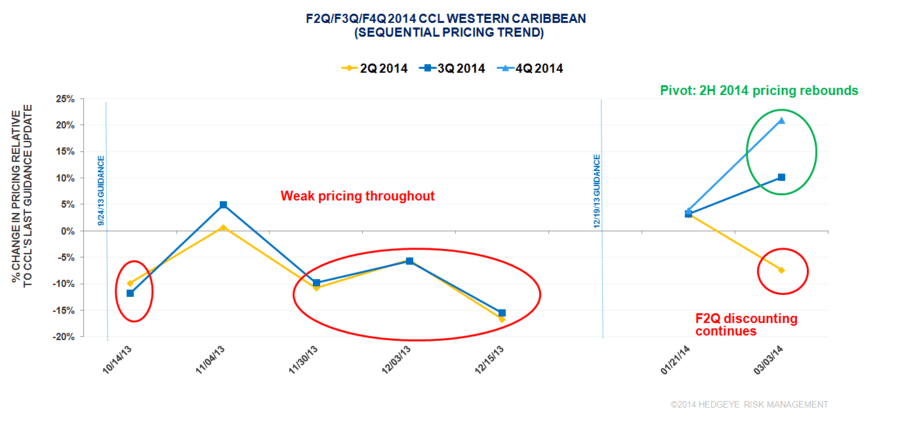

In the Caribbean, we saw discounting across the board among the lower priced itineraries in the Caribbean in mid-February, but the Carnival (CCL) brand pricing stood out in March, outperforming its peers.

Carnival sequential pricing picked up among the Eastern Caribbean itineraries. More importantly, sequential pricing rose among the Western Caribbean itineraries for 2H 2014.

This is encouraging given that Western Caribbean pricing has lagged. While Caribbean pricing overall remains sluggish and pricing has been quite volatile in the busy, promotional period of Wave Season, we continue to see Carnival as best positioned due to easy comps and low Street expectations.

Not surprisingly, the picture is starkly different in Europe. The Royal Caribbean (RCL) brand and Norwegian (NCLH) are leading the charge in a rosy booking and pricing environment. CCL has the most exposure to Europe but it is still trying to find a solid footing there with mixed pricing performance in March.

The Ukraine-Russia situation could be a wild card.

So far, no Black Sea sailings have been rescheduled or canceled on RCL and CCL brands. There’s speculation that Baltic Sea itineraries could eventually be impacted; that would be significant for CCL and RCL if it happens.

Alaska will be the weakest market pricing wise in 2014 – who wants to go somewhere cold nowadays?

While our study focused on sequential pricing trends and pivots, we would point out that YoY pricing for Carnival is up significantly due to the lapping of the Triumph fire incident in 2013. RCL and NCLH face more difficult comparisons in the Caribbean.

The Street is finally catching onto the low bar set by Carnival as even the most bearish sell-side have been raising yield and EPS estimates for CCL before they report earnings in three weeks. According to Factset, recent FY2014 estimate changes have trended around the $1.75 EPS range (at the upper end of CCL’s $1.40-$1.80 guidance). Our $1.90 EPS and 0.3% yield forecast for FY2014 remains unchanged from our note in December “CCL: $2 ON THE HORIZON.”