A return to all-time highs for US stocks is putting sentiment right back to where it was on 12/31.

#frothy

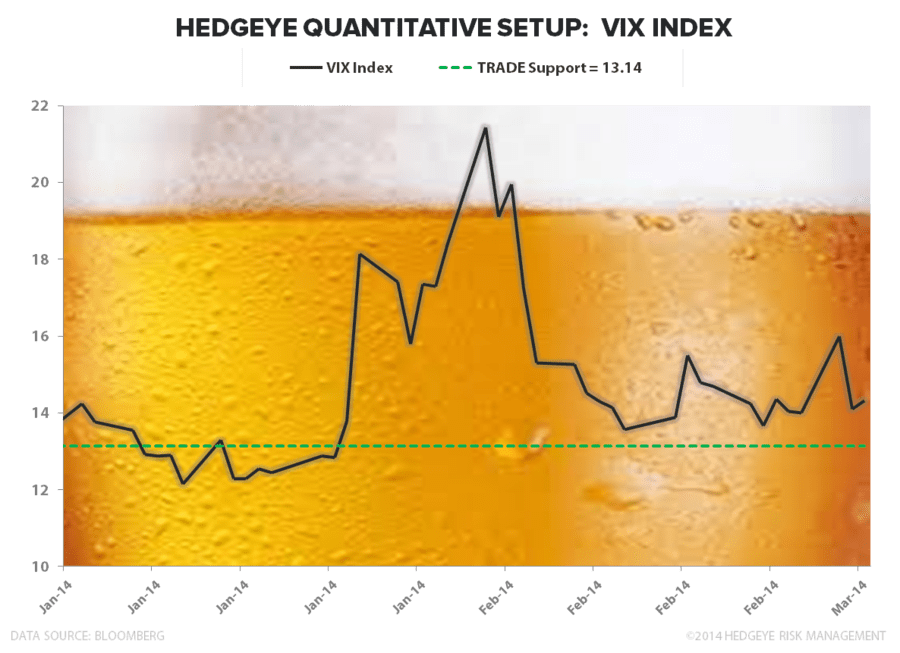

Both front month VIX (volatility) and the bear side of the II Bull/Bear survey have dropped right back to where they were on January 1. No, that’s not a good thing.

The Bull/Bear Spread has ripped right back towards its all-time highs at +3950 basis points wide to the bull side. Only 15% admit they’re bearish. That is a generational low.

Remember. Risk happens fast.