SUMMARY:

- At current levels, the ability for incremental savings reductions to drive further improvement in consumption growth remains very much constrained.

- Rising profligacy on luxury durables by the top income levels – which supported consumption growth in 2013 - occurred alongside peak gains in both housing and equities and is now collapsing as those same measures weaken.

- Given last years distortions, we’d argue that the 2Y comps still offer the cleanest read on the Trend in personal income growth – and on that basis, income growth continues to decelerate.

- With Inflation accelerating and growth slowing (which are reflexive, non-mutually exclusive dynamics) and geopolitical risk percolating, we’ll cover opportunistically on red, but will remain better sellers/shorters of domestic equity strength in the immediate term.

SPENDING & INCOME

Spending grew at a premium to income for a fourth consecutive month as Services expenditures led the gains, accelerating on a MoM, 1Y and 2Y while spending growth on Durables and NonDurables declined MoM and decelerated on both a 1Y and 2Y basis.

The savings rate held at 12 month lows and remains near the low end of the historical range.

At current levels, the ability for incremental savings reductions to drive further improvement in consumption growth remains very much constrained.

HIGH END IN RETREAT?

The acceleration in Durable Goods expenditures led the strength in household spending last year. Demand for durables is generally more elastic than that for NonDurables and rising, broad based demand for durable goods can offer insight into emergent strength in household consumerism.

What’s notable, however, is that last year’s acceleration in durable goods spending was driven largely by demand for luxury and high-end items.

In fact, as can be seen in the chart below, demand for luxury durables (Pleasure Boats/Aircraft and Watches/Jewelry) accelerated in 2H13, supporting headline durables growth even as broader durables demand began to slow.

Spending on the same luxury items has collapsed since hitting peak growth in October.

Coincidently (or not), rising profligacy on luxury durables by the top income levels occurred alongside peak gains in both housing and equities and is now tracking the same measures lower.

With home price gains decelerating since October and domestic equities down YTD, it appears increasingly unlikely that the rich provide an incremental boost to consumption growth – at least not at the magnitude of last year’s contribution.

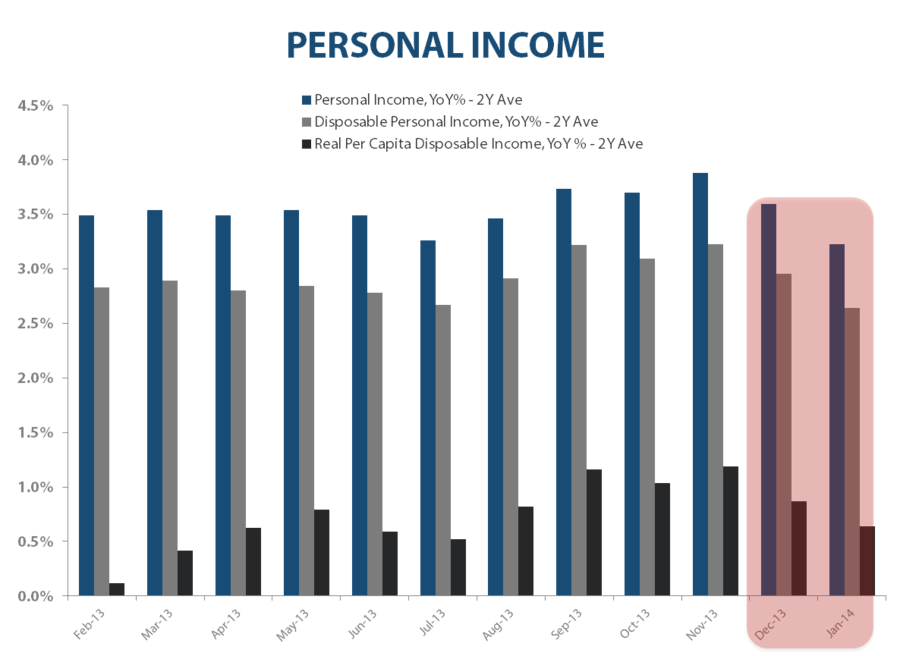

INCOME: Use the 1Y or 2Y comps?

Optically, personal income growth improved sequentially as Disposable Income (DPI), Real Per Capita DPI, Private Sector Salaries and Government Salaries and Wages all accelerated YoY in January.

Recall, however, that personal income figures over the peri-fiscal cliff period from Nov-12 to Jan-13 were distorted as individuals pulled forward compensation and companies ramped special dividend payments ahead of the impending tax law changes.

Given the noisy comp dynamics we’d argue that the 2Y comps still offer a cleaner read on the Trend in personal income growth currently.

Growth on a 2Y average basis showed a second consecutive month of deceleration across all the aforementioned income measures and stands in direct contrast to the positive income dynamics suggested by the YoY figures.

2014 TAILWIND:

While hourly earnings growth and weekly hours continue to track sideways, at the margin, the spending friendly budget deal and positive employment growth at the State and Local Government level should support salary and wage growth for the 17% of the labor force that is government workers.

Indeed, aggregate, government sourced wage and salary income showed positive YoY growth for the first time in 11 months in January.

Further, from a comp perspective, the annualization of the (higher-earner) tax increases and the end of the payroll tax holiday that occurred in January of last year both setup as positive dynamics supporting consumer spending for 2014.

So, similar to the February ISM report this morning, the January income and spending data extended the broader Trend towards decelerating growth.

With Inflation accelerating and growth slowing (which are reflexive, non-mutually exclusive dynamics) and geopolitical risk percolating we’ll cover opportunistically on red, but will remain better sellers/shorters of domestic equity strength in the immediate term.

Christian B. Drake

@HedgeyeUSA