***********************************************************************************

"Legging into Legg Mason"

Invitation to Best Ideas Long Conference Call Tomorrow

Please join us tomorrow, March 4th at 1 pm EST for a conference call detailing our newest Long idea in Financials, Legg Mason (LM).

Participant Dialing Instructions:

- Toll Free Number:

- Direct Dial Number:

- Conference Code: 824597#

- Materials: CLICK HERE (Slides will be available approximately one hour prior to the start of the call)

***********************************************************************************

Not So Fast:

Just when it was looking like it was safe to get back in the water. The Ukraine suddenly matters (a lot) to investors, with Europe off 2-3% and S&P 500 futures down ~20 handles. We've been, on the margin, arguing for a more defensive posturing in light of what had been rising interbank, systemic risk measures, rising commodity prices and falling yield spreads. The concerns were initially prompted by the EM fears that surfaced roughly a month ago. Since then we've been erring on the side of caution while the XLF has grinded a few percent higher. This morning, serendipitously, that call appears to have been right. The reality is that through the end of last week some of the risk measures we track were starting to flash the all clear, but in light of the Ukraine situation, we'll hold the line. It doesn't hurt to wait and watch in the short term.

Key Points:

* 2-10 Spread – Last week the 2-10 spread tightened to 233 bps, -9 bps tighter than a week ago, and the 10-year yield is down a further 4 bps this morning.

* Euribor-OIS Spread – The Euribor-OIS spread tightened by 1 bps to 15 bps. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

* CRB Commodity Price Index – The CRB index rose 0.2% last week, ending the week at 302. As compared with the prior month, commodity prices have increased 6.7%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

* TED Spread – The TED spread fell 0.9 basis points last week, ending the week at 18.8 bps this week versus last week’s print of 19.7 bps.

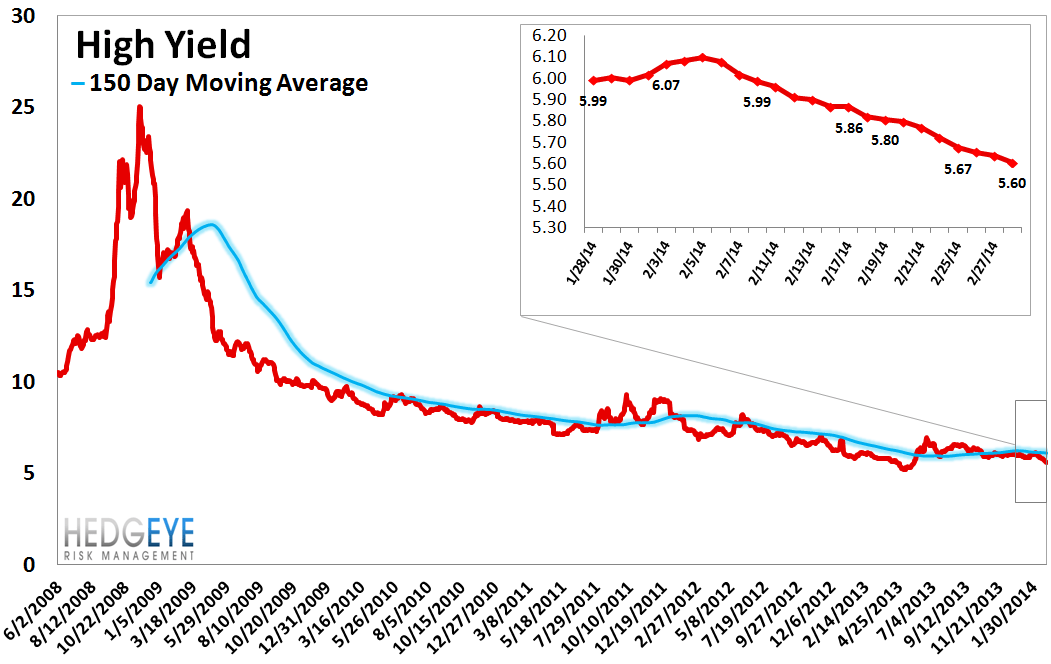

* High Yield (YTM) – High yield rates fell 16.2 bps last week, ending the week at 5.60% versus 5.77% the prior week.

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 5 of 13 improved / 3 out of 13 worsened / 5 of 13 unchanged

• Intermediate-term(WoW): Positive / 7 of 13 improved / 3 out of 13 worsened / 3 of 13 unchanged

• Long-term(WoW): Positive / 5 of 13 improved / 1 out of 13 worsened / 7 of 13 unchanged

1. U.S. Financial CDS - Swaps tightened for 24 out of 27 domestic financial institutions. Wells Fargo and Allstate went wrong the way last week, but by a mere +1 bps, and GS was unchanged. Otherwise the US Financials were tighter across the board.

Tightened the most WoW: SLM, AGO, COF

Widened the most WoW: WFC, ALL, GS

Tightened the most WoW: BAC, PRU, AGO

Tightened the least MoM: TRV, AXP, AON

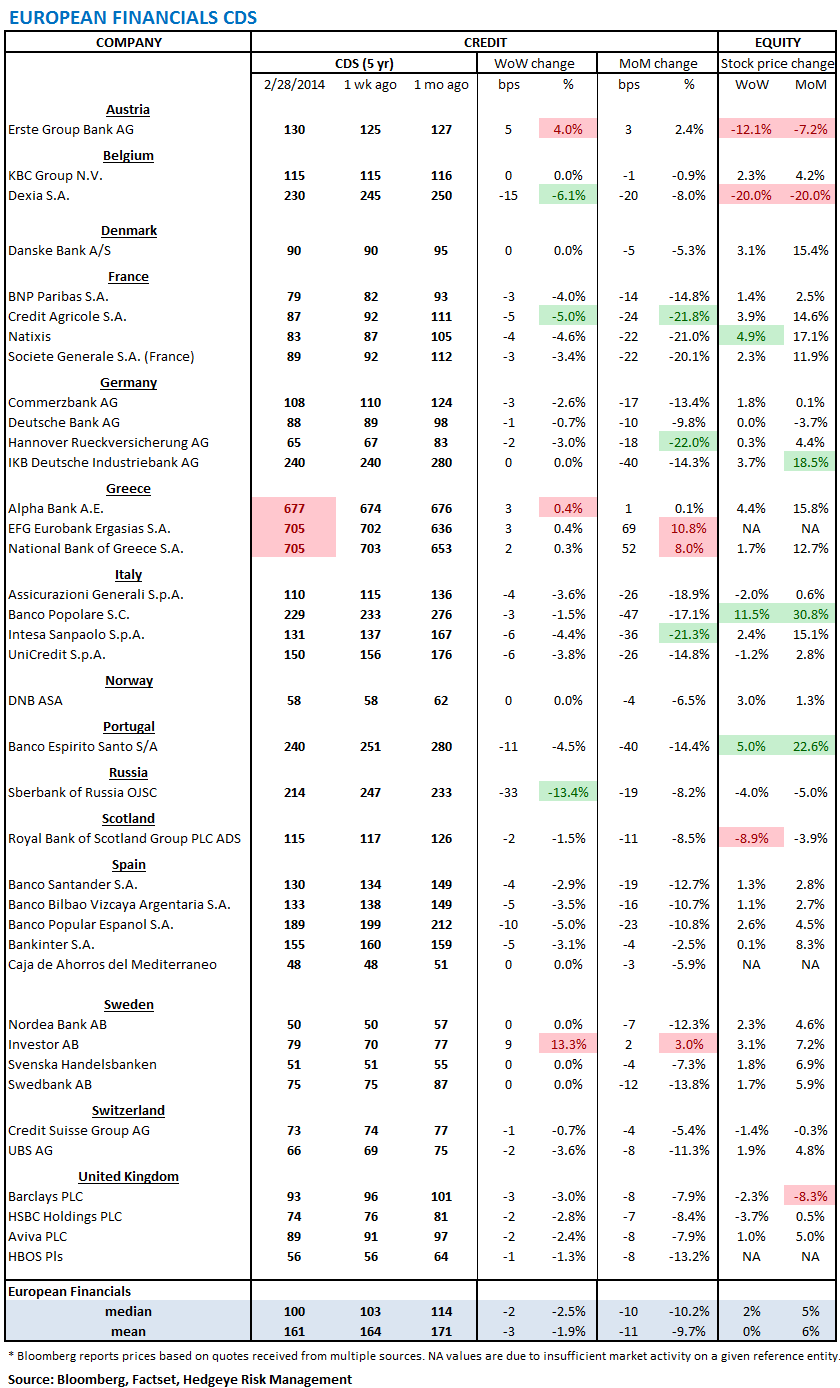

2. European Financial CDS - Aside from a few minor exceptions, European bank swaps were tighter last week, compressing by an average 3 bps (2 bps median decline). The month-over-month change in Europe is more impressive, as much of the Continent's banking system is now seeing double digit M/M declines.

3. Asian Financial CDS - It was another mixed, though largely unexceptional week for Asian financials. Two out of three Indian banks were notably tighter, while in China the Export-Import Bank widened by 11 bps. Across Japan, the only notable mover was Nomura at +11 bps.

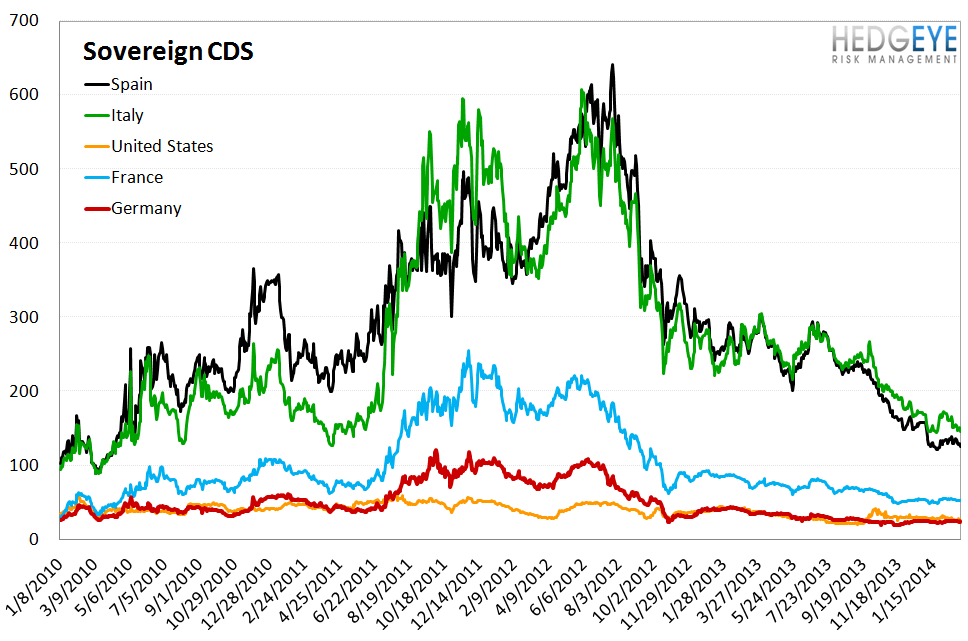

4. Sovereign CDS – Sovereign swaps across Europe tightened notably last week, while the rest of the world was largely uneventful with the US and Japan widening just one basis point.

5. High Yield (YTM) Monitor – High Yield rates fell 16.2 bps last week, ending the week at 5.60% versus 5.77% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 1.0 point last week, ending at 1850.

7. TED Spread Monitor – The TED spread fell 0.9 basis points last week, ending the week at 18.8 bps this week versus last week’s print of 19.69 bps.

8. CRB Commodity Price Index – The CRB index rose 0.2% last week, ending the week at 302. As compared with the prior month, commodity prices have increased 6.7%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

9. Euribor-OIS Spread – The Euribor-OIS spread tightened by 1 bps to 15 bps. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

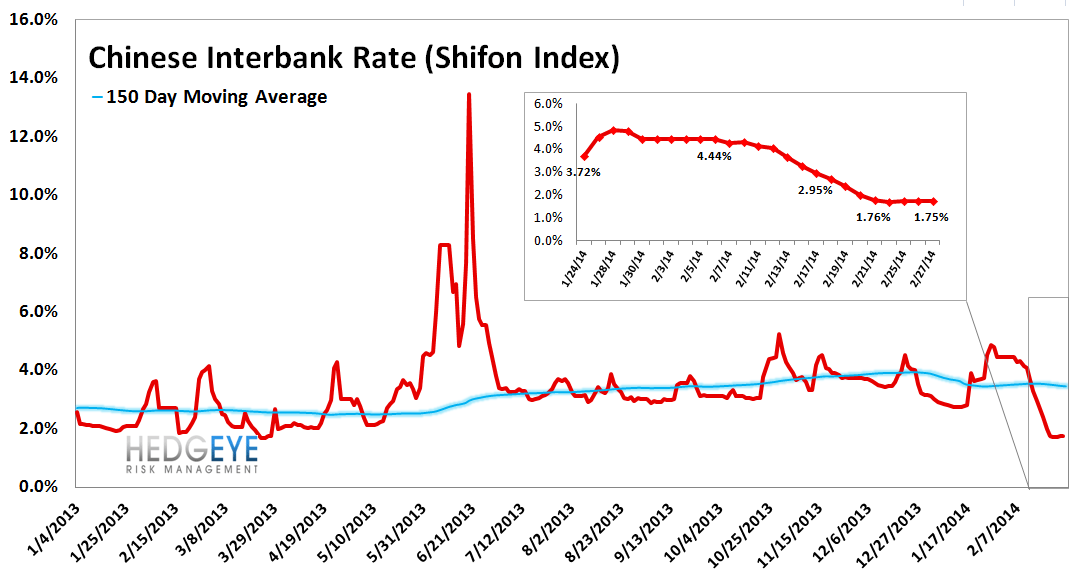

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index fell 1 basis points last week, ending the week at 1.75% versus last week’s print of 1.76%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Markit MCDX Index Monitor – Last week spreads tightened -3 bps, ending the week at 73 bps versus 76 bps the prior week. The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. We track the 16-V1.

12. Chinese Steel – Steel prices in China fell 1.0% last week, or 32 yuan/ton, to 3,302 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 233 bps, -9 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 0.2% upside to TRADE resistance of $21.75 and 1.7% downside to TREND support of $21.34.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT