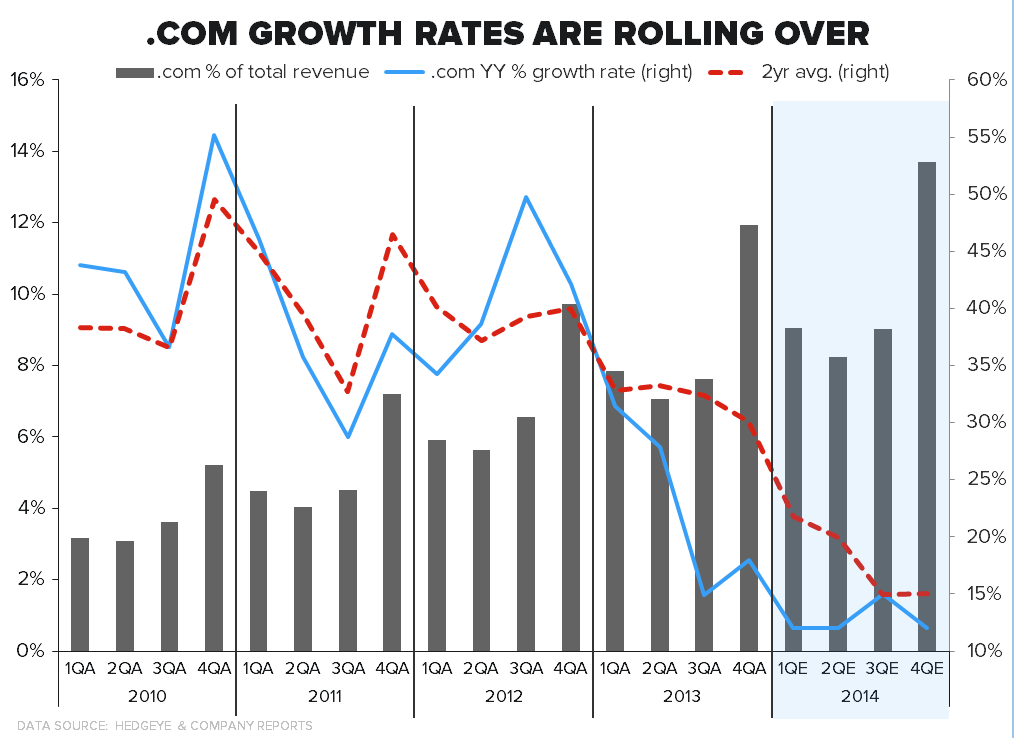

Conclusion: We already stated our belief that KSS 2014 guidance is too aggressive – in fact, we don’t even think it will comp positive. While the crux of our argument rests in $800mm in revenue that we think is at risk to JCP, we found the company’s e-commerce trends to be troubling as well. E-commerce sales have protected KSS' comp for the past 9 quarters. With dot.com growth slowing, we seriously question the company’s 2014 comp guidance. If we estimate a (4%) brick and mortar comp with a 15% .com growth rate, we are looking at a (3%) blended comp in FY14 -- representing about half of what is at risk for the year.

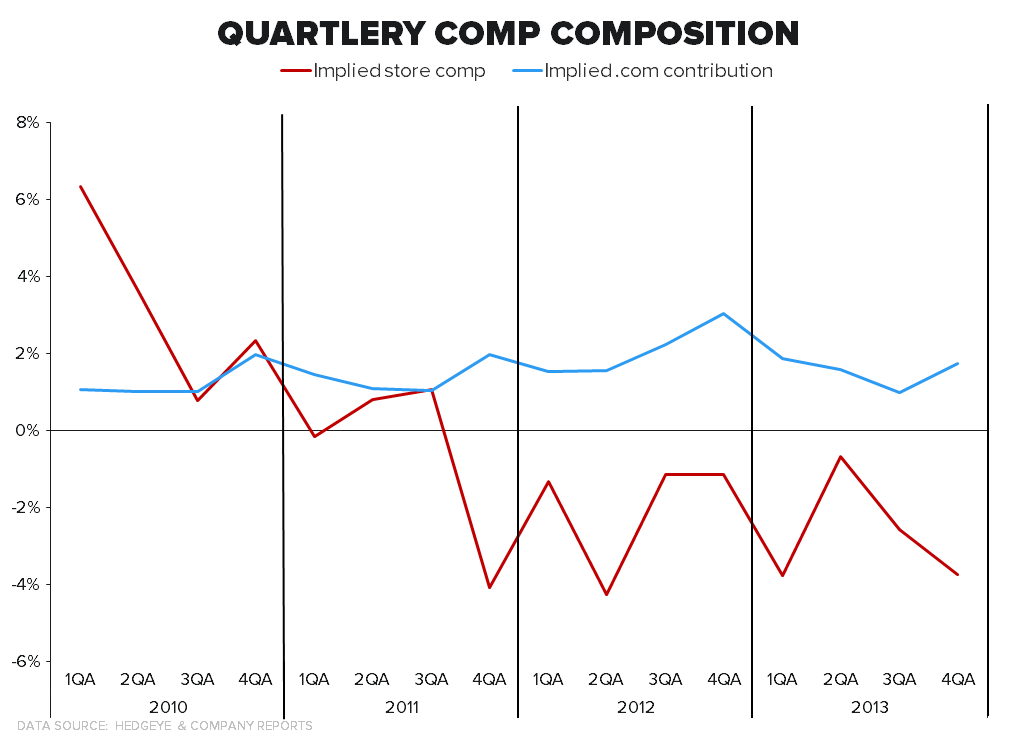

While not outwardly clear given dot.com and store comps are blended into one number, it’s pretty troubling that brick and mortar comps have been negative for nine straight quarters. Growth in the dot.com channel has protected the company's reported comp over that time period to some degree, as outlined in the chart below.

KSS definitely recognized the importance of dot.com and have grown that side of the business at a 37% CAGR over the last 5 years into a $1.7bn business. Unfortunately, the growth rate of KSS’ dot.com is clearly slowing – both on a one and two-year basis. We still dot.com growth of 15% in '14 - but it won't continue to grow fast enough off of a much bigger base to offset weakness in KSS' 1100+ doors.

Alec Richards

HedgeyeRetail