Summary: We’ve been vocal in our expectation for a deceleration in the slope of domestic growth over the last couple months and while this morning’s downward revision to 4Q13 wasn’t particularly surprising, it does offer some positive confirmation to that view.

With the dollar breaking down, #InflationAccelerating, earnings growth still sub-trend, wealth effect (equities/housing) momentum decelerating and little incremental upside for consumption growth via a reduction in savings, we continue to think the growth decelerating trend extends through 1H14.

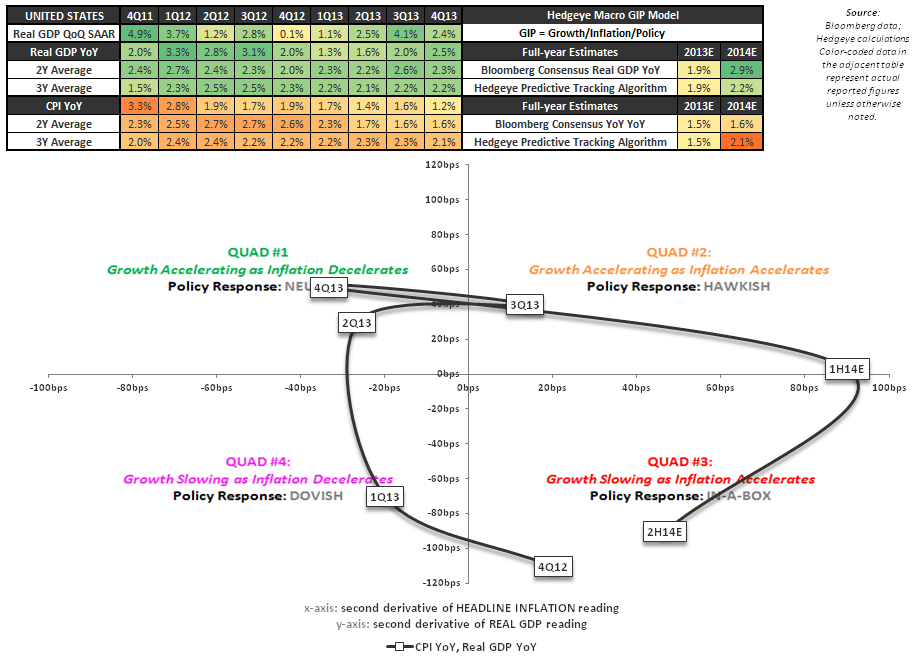

GIP MODEL REFRESH: The net impact to our GIP (Growth/Inflation/Policy) model from this morning’s data is another incremental shift in trajectory towards quadrant #3 – Slowing Growth and Rising Inflation.

To the extent that the market continues to discount slowing growth and subsequent, incremental easing in policy – which ironically/unfortunately only perpetuates the move into Quad #3 – we think slow growth exposure (gold/bonds/commodities/utilities) continues to outperform pro-growth leverage.

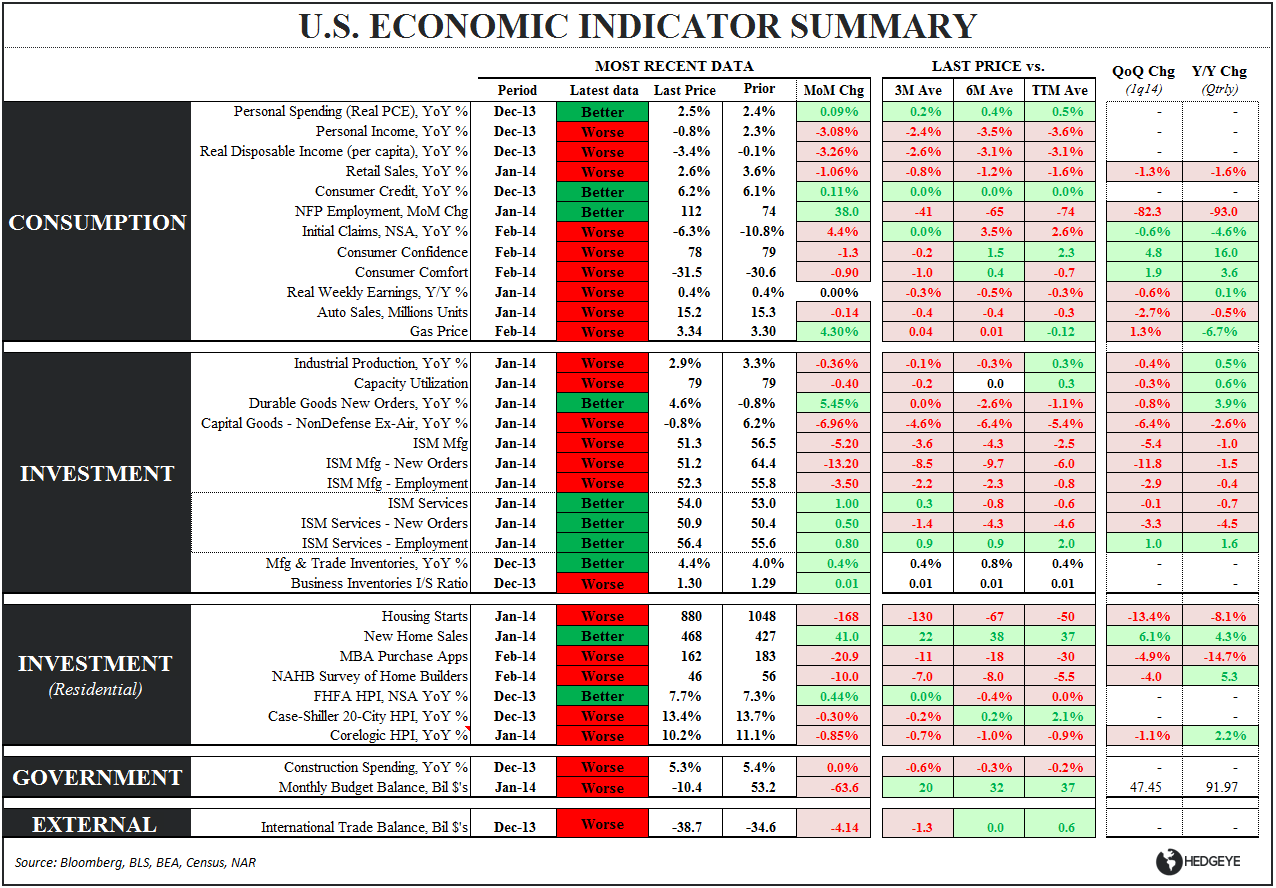

GDP DATA SUMMARY: Below we highlight the notables in this mornings, 1st revision to the 4Q13 GDP estimate.

Real GDP: revised lower by 80bps to 2.4% from 3.2%. Decelerating 170bps QoQ to 2.4%.

Nominal GDP: decelerating 200bps QoQ from +6% in 3Q13 to +4% in 4Q14.

Inflation: Inflation estimates marked higher with the GDP Price index and Core PCE measures revised up 30bps and 20bps, respectively.

C+I+G+E Revision: Investment revised up small, everything else revised lower.

C: Consumption saw the largest downward revision from a contribution perspective at -.53% with QoQ growth revised from +3.3% to +2.6%. Durable/NonDurables/Services were all revised lower but Durables (as the latest PCE data has reflected) saw the largest decline.

Whether the emergent deceleration in durables, and luxury and higher-end durables particularly, represents a pull-back in spending across the top income quintiles as equity and home value gains slow remains to be seen. We’ll get the updated PCE detail data on Monday.

I: Investment: Private Nonresidential Investment, which was revised higher by +0.4 from a contribution perspective and +3.5% from a growth perspective, was one of the lone bright spots in the report.

Inventories were revised lower and with inventory-to-sales ratios continuing to creep higher through year end, its unlikely inventories provide another outsized boost to reported growth in the coming quarters.

G + NE: Government was revised down modestly while the revision to the trade balance was the second biggest contributor to the headline decline with export growth revised -2.0% against a +.60% revision for imports.

Real Final Sales growth (GDP less Inventory Change): decelerating 20bps QoQ to 2.3%…revised lower by 50bps

Gross Domestic Purchases (GDP less exports, including imports): Very Weak sequentially - Decelerating 250bps QoQ to +1.4%..revised lower by 40bps

Real Final Sales to Domestic Purchasers (GDP less exports less inventory change): (Perhaps) The cleanest read on aggregate domestic demand was also weak, decelerating 100bps to +1.2%, revised lower by 20bps.

Christian B. Drake

@HedgeyeUSA