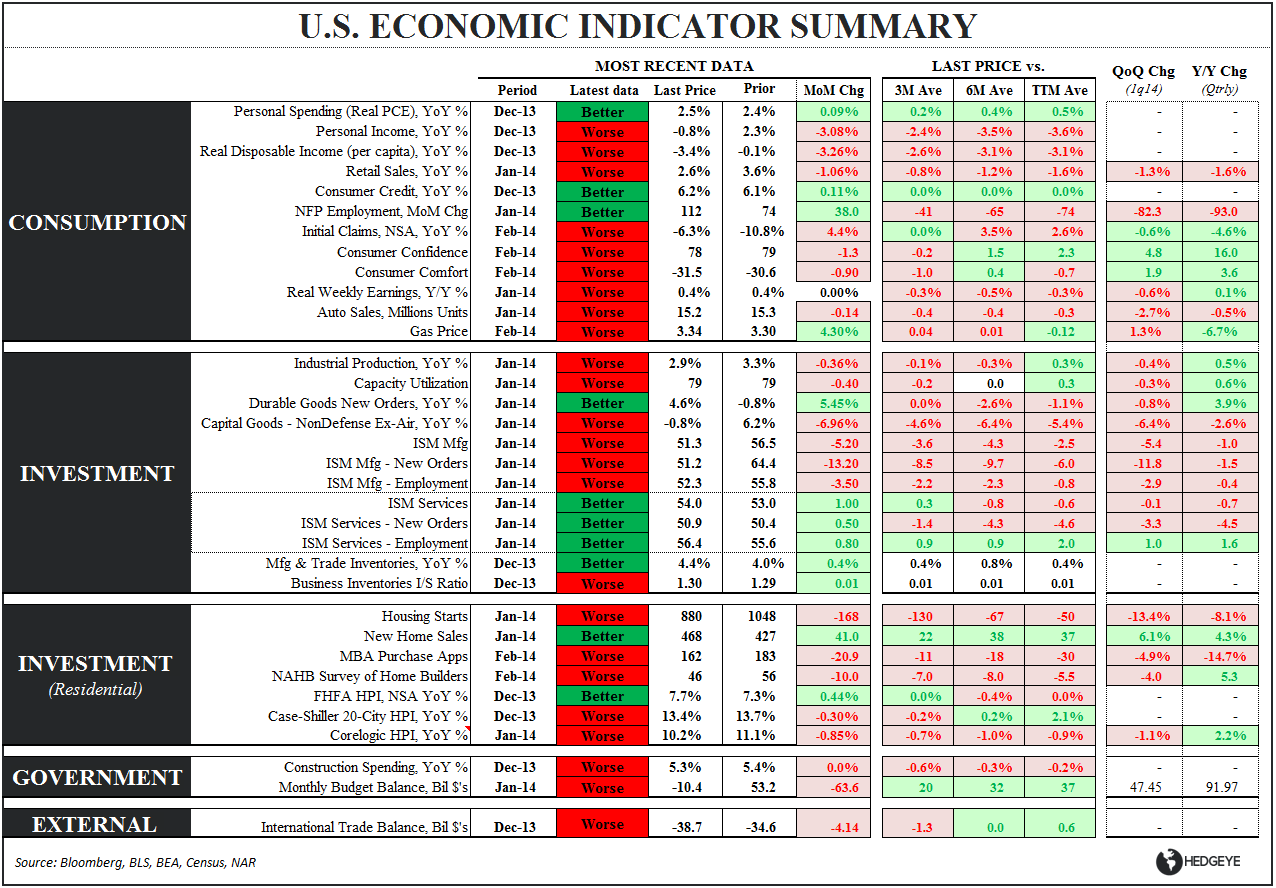

Summary: The softness in New Durable & Capital Goods Orders extends itself in January. The labor market continues to improve but at a slowing rate. Bloomberg’s high frequency read on Consumer Confidence printed its best reading in 6 wks but the current trend remains equivocal.

Meanwhile, the preponderance of domestic, fundamental macro data continues to suggest slowing growth – a trend the market continues to discount as utilities, bonds, and gold/commodities continue to outperform pro-growth leverage.

DURABLE GOODS: Unsurprising softness following January ISM and Retail Sales

Headline New Orders: Durable Goods declined for two consecutive months for the first time since October 2011 as January New Orders declined -1.0% MoM, unable to comp Decembers -5.3% MoM decline. The 23% MoM increase in Defense Orders in January helped buttress the headline reading against broader private sector softness

New Durable Goods Orders Ex-Defense & non-defense Aircraft: Orders ex-Defense and Aircraft - perhaps the best of the sub-aggregates in gauging household consumerism - remained negative on a MoM basis and decelerated on a YoY basis.

Capital Goods Orders: The great 2014 capex resurgence narrative remains in a holding pattern as Core Capex Orders growth retraced Decembers MoM decline but posted its first YoY decline in 10 months.

INITIAL CLAIMS: SLOWING IMPROVEMENT

After last week’s counter-trend move to 4-weeks of steadily deteriorating improvement in the initial claims data, this morning’s data again reflects a deceleration in the rate of improvement in the domestic labor market.

The year-over-year rate of improvement in rolling NSA initial jobless claims decelerated to -4.4% from -5.4% WoW as the YoY rate of change worsened to +0.13% YoY vs. -8.4% the week prior.

On a seasonally-adjusted basis, initial jobless claims rose 14k to 348k from 334k WoW, as the prior week's number was unrevised lower by 2K. Meanwhile, the 4-week rolling average of seasonally-adjusted claims was flat WoW at 338K.

To be clear, the trend in the labor market is still one of improvement but, in contrast to last year which was largely characterized by accelerating improvement, the prevailing trend YTD has been one of deceleration.

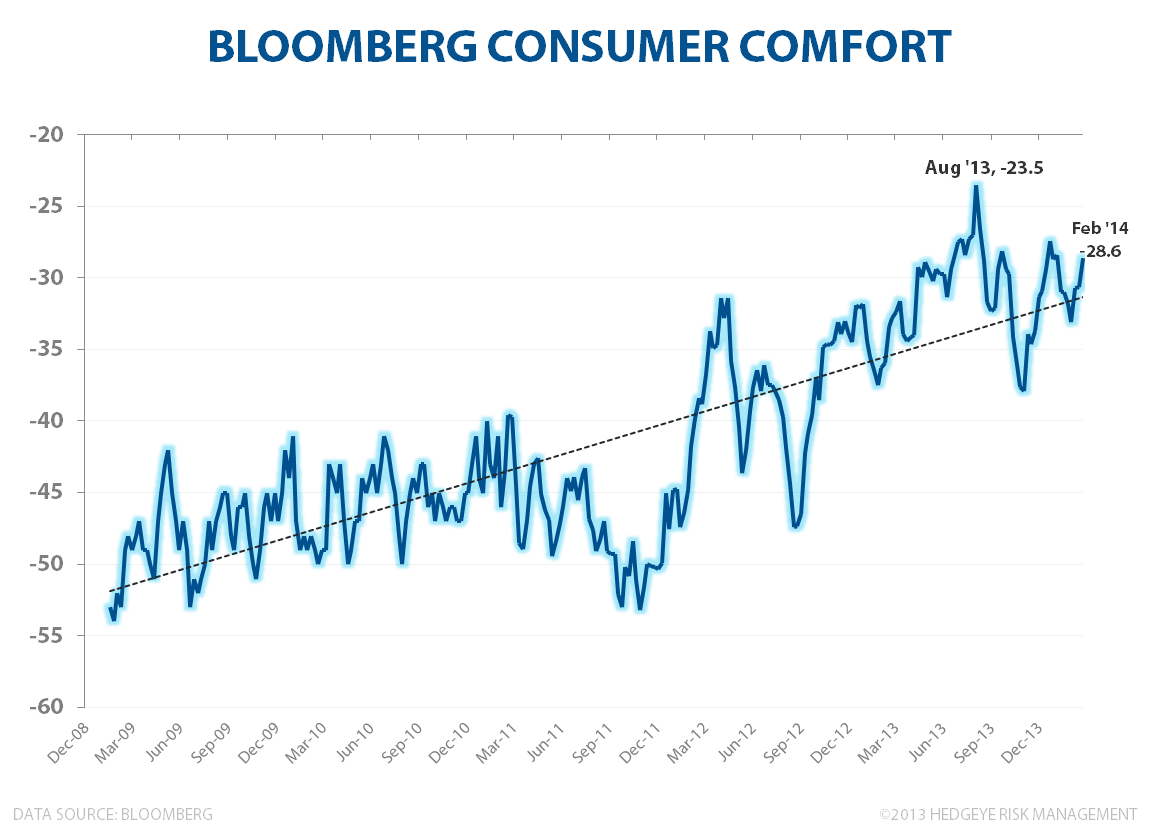

CONFIDENCE: Bloomberg’s weekly survey of Consumer Comfort printed its best reading in 6 weeks but, across the primary confidence surveys, the data remains mixed and the current trend largely equivocal with the University of Michigan and Conference Board surveys flat and modestly lower sequentially in February, respectively.

Christian B. Drake

@HedgeyeUSA