We've maintained that 2009 will be an extremely difficult year in the Las Vegas locals market. While the actual gaming revenues through the first 5 months of the year haven't been that bad, we're not out of the woods. More importantly, a bottoming housing market and population growth should provide positive growth in gaming revenues in 2010. The following chart shows the Locals gaming revenue trends. Note that revenues have been getting "less bad" since December and have been stable since January.

We put forth our Las Vegas Locals macro model in our 2/05/09 post. The conclusion then was that the macro variables of housing prices, unemployment, interest rates, and population growth explain virtually all of the growth in gaming revenues. If this relationship holds up, the LV locals market could be one of the best performing markets next year. Given the inputs of flat housing prices, unemployment rising to 11.5% from 11% in 2009, and 1% population growth, our model projects gaming revenue growth of 5%.

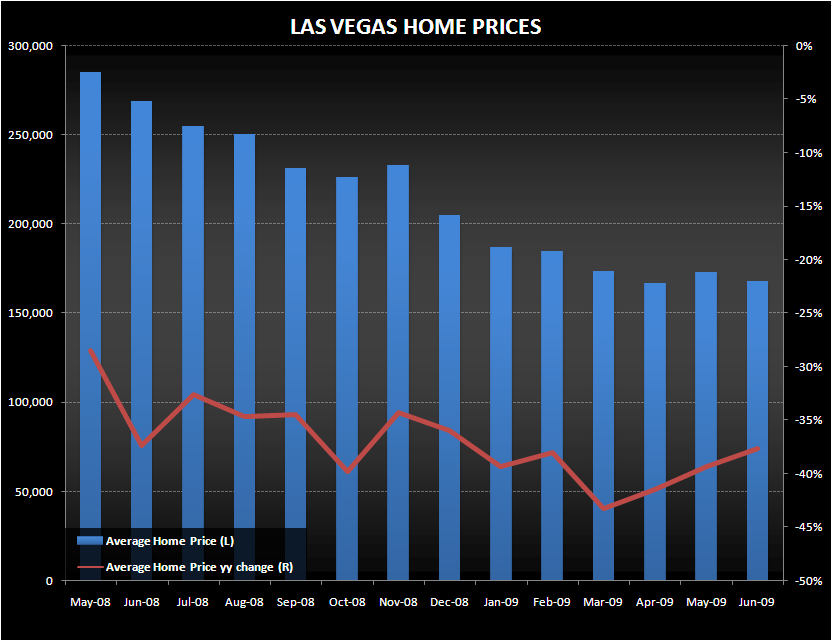

The recent housing data have shown a bottoming in prices, at least sequentially, while the year-over-year decline has improved. The average home price has been stable since March at around $170k. Velocity has actually improved which gives us some confidence that the recent stability is sustainable. Home sales have increased sequentially for 5 straight months. Year-over-year home sales are up huge as can be seen in the following chart.

With 30% exposure to the LV locals market, Boyd Gaming has been hit hard by the economic calamity but will also be the prime publicly traded beneficiary of the recovery we see next year. Considering the 25%+ free cash flow yield on the stock, investors are certainly not pricing in a recovery.