TODAY’S S&P 500 SET-UP – February 27, 2014

As we look at today's setup for the S&P 500, the range is 27 points or 1.09% downside to 1825 and 0.37% upside to 1852.

SECTOR PERFORMANCE

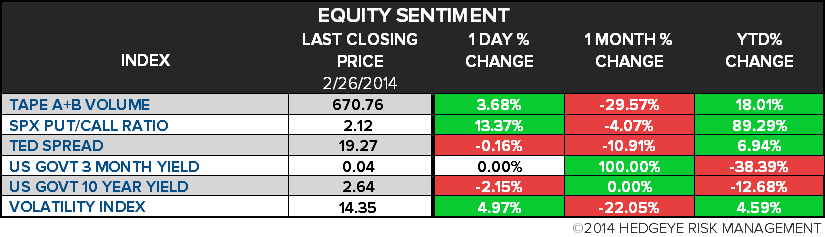

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.33 from 2.34

- VIX closed at 14.35 1 day percent change of 4.97%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Durable Goods, Jan., est -1.6% (pr -4.3%, rev -4.2%)

- 8:30am: Init Jobless Claims, Feb. 22, est. 335k (prior 336k)

- 9:45am: Bloomberg Consumer Comfort, Feb. 23 (prior -30.6)

- 10am: Fed’s Yellen testifies to Senate Banking Committee

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 10:30am: Fed’s Fisher speaks in Frankfurt

- 11am: Kansas City Fed Mfg Activity, Feb., est. 2 (prior 5)

- 1:30pm: ECB’s Draghi speaks in Frankfurt

- 3:15pm: Fed’s Lockhart and George speak in Atlanta

GOVERNMENT:

- 9:30am: House Oversight panel holds hearing on IRS examinations of political speech by tax-exempt groups

- 10am: Senate Banking Cmte hears from Fed Chair Yellen on semiannual monetary report to Congress

- 10am: House Transportation and Infrastructure panel meets on “Improving the Nation’s Highway Freight Network”

WHAT TO WATCH:

- Janet Yellen to testify before Senate Banking Committee

- Sony job cuts to include a third of electronics unit workers

- Baidu 1Q revenue forecast tops estimate as 4Q beats

- Williams Partners to buy Williams Canada assets for $1.2b

- JPMorgan sees March bid for Global Special Opportunities: WSJ

- J.C. Penney gains as sales forecast signals turnaround momentum

- KKR said to seek Abril Educacao deal avoiding $1b buyout

- Imerys tops Minerals Technologies bid for clay-supplier Amcol

- Bitcoin Foundation aided New York prosecutor’s Mt. Gox probe

- U.S. cos. seen making exchange plans to trade Bitcoin: WSJ

- Google fights e-mail privacy group lawsuit calling it too big

- Musk’s $5b Tesla gigafactory may unleash incentive fray

- Gunmen take Ukraine’s Crimea parliament, raise Russian flag

- German unemployment falls for 3rd month as growth picks up

- Eurozone Feb. economic confidence rises to 101.2; est. 100.7

- RBS posts biggest loss since 2008 as McEwan details overhaul

- WPP falls most in 4 yrs as exchange rates hurt margins

- Financing for Jos. A. Bank’s Bauer deal delayed by Goldman: WSJ

AM EARNS:

- American Realty Capital (ARCP) 6am, $0.27

- Best Buy (BBY) 7am, $1.01 - Preview

- Chico’s (CHS) 7:15am, $0.16

- Cobalt International Energy (CIE) 7am, $(0.16)

- Federal Home Loan Mortgage (FMCC) 8am, $0.73

- Fortress Investment Group (FIG) 7am, $0.19

- GrafTech Intl (GTI) 7:10am, $0.03

- Hilton (HLT) Bef-Mkt, $0.16

- Kohl’s (KSS) 7am, $1.54 - Preview

- Lamar Advertising (LAMR) 6am, $0.16

- Linn Energy (LINE) 6:50am, $0.26

- LinnCo (LNCO) 6:50am, $0.50

- LKQ (LKQ) 7am, $0.28

- Mylan (MYL) 6:30am, $0.75 - Preview

- Nationstar Mortgage (NSM) 6am, $(0.19)

- NorthStar Realty Finance (NRF) 7:30am, $0.29

- Ocwen Financial (OCN) 7:30am, $1

- Pall (PLL) 7am, $0.80

- Rowan Cos (RDC) 8am, $0.41

- Sarepta Therapeutics (SRPT) 7am, $(0.70)

- Sears Holdings (SHLD) 6am, $(1.82)

- Sempra Energy (SRE) 9am, $0.97

- Toronto-Dominion (TD CN) 6:30am, C$1.04 - Preview

- Valeant Pharaceuticals (VRX) 6am, $2.06 - Preview

- Wendy’s (WEN) 7:30am, $0.10

- Western Refining (WNR) 6am, $0.56

- Windstream (WIN) 6:15am, $0.09

- WPX Energy (WPX) 7am, $(0.35)

- Zale (ZLC) 7:30am, $1.04

PM EARNS:

- ACADIA Pharmaceuticals (ACAD) 4:01pm, $(0.13)

- Arena Pharmaceuticals (ARNA) 4:03pm, $0.15 - Preview

- Deckers Outdoor (DECK) 4pm, $3.79

- Gap (GPS) 4pm, $0.65

- KBR (KBR) 4:08pm, $0.91

- Kodiak Oil & Gas (KOG) 4:01pm, $0.18

- Medivation (MDVN) 4:10pm, $(0.09)

- Mentor Graphics (MENT) 4:05pm, $0.91

- Monster Beverage (MNST) 4:05pm, $0.46

- New Gold (NGD CN) 4:04pm, $0.03

- OmniVision Technologies (OVTI) 4:18pm, $0.35

- Ross Stores (ROST) 4pm, $1.01 - Preview

- Salesforce.com (CRM) 4:05pm, $0.06

- Salix Pharmaceuticals (SLXP) 4:01pm, $0.93

- SandRidge Energy (SD) 4:05pm, $0.00

- Sotheby’s (BID) 4pm, $1.41

- Splunk (SPLK) 4:02pm, $0.05

- Sprouts Farmers Market (SFM) 4:05pm, $0.06

- Universal Health Services (UHS) 5:01pm, $1.08

- Youku Tudou (YOKU) 4:30pm, $0.02

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Copper Trades Near December Low With Production Set to Expand

- Japan No Country for Old Farmers as 7-Eleven Takes Up the Plow

- EU Fines No Bar to Milk Output Gain as Price Surges: Commodities

- Brent Crude Declines to One-Week Low; Premium to WTI Narrows

- Gold Rally Restores Luster to ETFs After Slide: Chart of the Day

- Wheat Extends Loss as Demand Seen Easing Amid Argentina Exports

- Arabica Coffee Drops Following Surge on Brazil Crop-Forecast Cut

- China Copper Premium Slumps to Eight-Month Low as Yuan Weakens

- Palm Oil Climbing for Merchant’s Coleman on Dry Weather Risk

- Cattle Poised to Extend Rally With Hogs as U.S. Meat Supply Ebbs

- Oil Giants Sell Pipelines as Shale Strength Drives Deals: Energy

- Shale Boom Brings Rethinking of U.S. Crude Export Ban: QuickTake

- Europe Refiner Bull & Bear Pits New Markets vs. Tax: BI Outlook

- Gold Erases Drop in London, Is Little Changed at $1,332.07/Oz

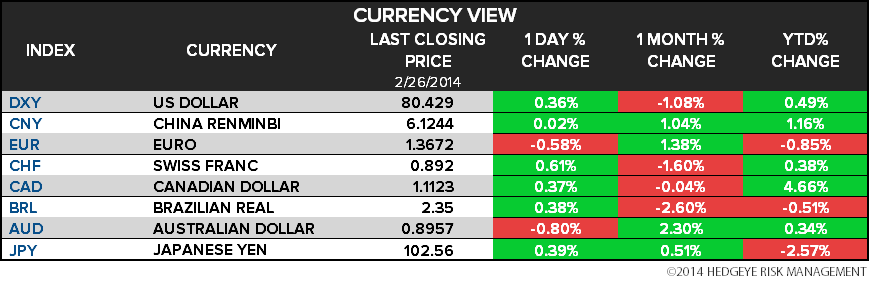

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

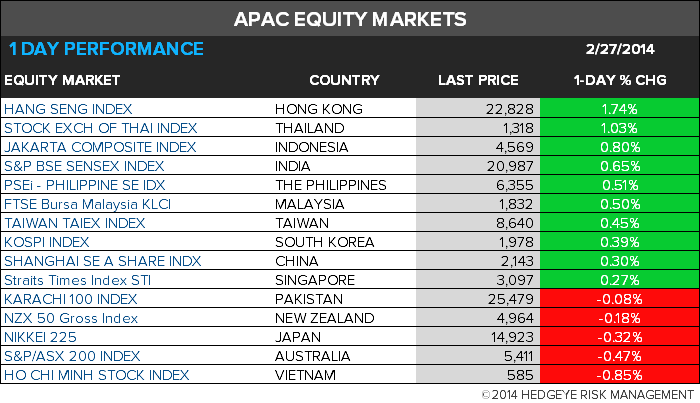

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team