Conclusion: The puts and takes battle each other fiercely this quarter. Good improvement on the margin on the P&L, but cash flow went the other way. Net/net, let's face it...JCP never gets a win. This is as close to a win as its gotten in a while. That said, probably not enough for us to get back on board, as we think that the earnings power is there, but the right management team is not. For now, we're still 'JCP Agnostic'.

DETAILS

With the run that JCP had immediately preceding the earnings release, JCP needed to ‘bring it’ with this print. While the numbers on a stand-along basis were atrocious – it’s tough to argue otherwise, our sense is that there will be two camps emerging from this earnings report; 1) one that looks at the income statement, who will be upbeat about the positive changes on the margin (changes on the margin is what matters), and 2) one that is focused on cash flow and the balance sheet, which looked pretty depressing. The peer analysis below speaks volumes. You might argue that the P&L and Cash Flow might wash each other out. But the reality is that we’re talking about JC Penney here. It NEVER wins. The fact that it showed signs of life on the P&L is a positive that can’t be overlooked. As bad as the results were overall, they got better on the margin. That doesn’t happen a whole lot with JCP.

So does this mean that we jump back on board as one of the lone bulls on the name? We thought about it – very briefly. But the answer is no. Every bit of research we’ve done over the past year – including multiple consumer surveys – tells us that there’s $1.50 in earnings power buried away in there. And let’s be clear…we’re not talking about some phantom earnings power that will never be realized. We definitely think that $1.50 is attainable. But we remain hung up on our view that the current management team simply cannot make those numbers a reality. We acknowledge that Ullman can continue to steer the ship for another year, and productivity, earnings, and cash will all likely be in a better place. After all, this quarter alone showed a nice delta on some key line items. Let’s give credit where it’s due. But we don’t think Ullman is the guy to get JCP to a point where it actually makes money, which is pretty critical to us building up to a defendable value for this company.

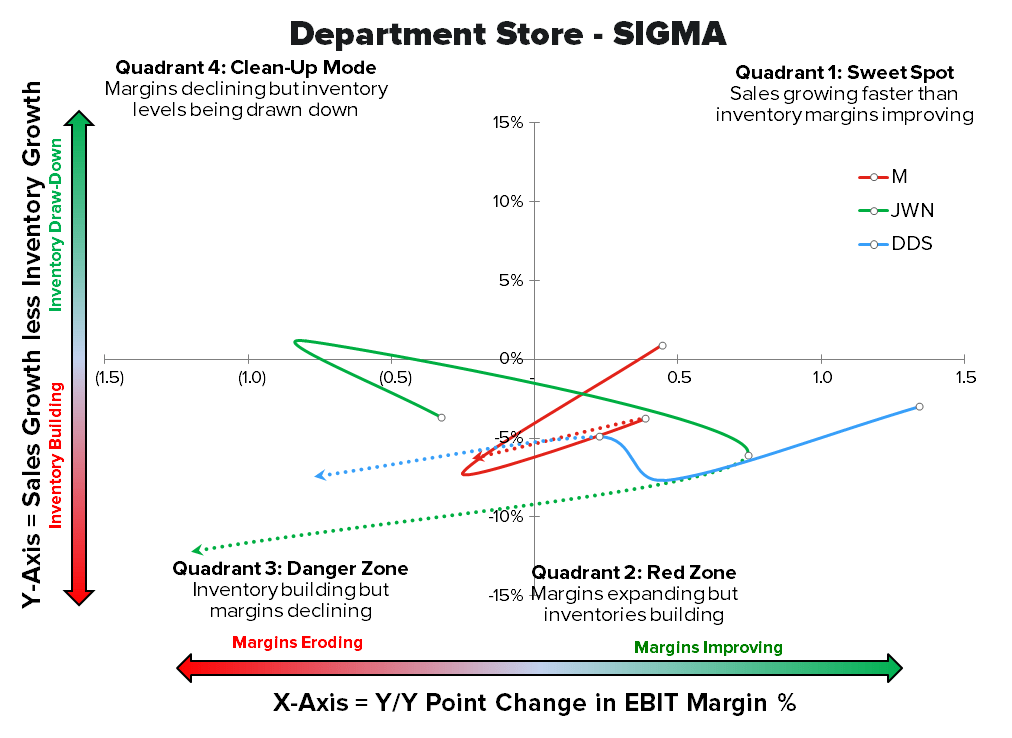

Everyone will agree that this quarter was challenging for everyone. In order to get a complete picture of the financial landscape, let’s compare JCP to the other department stores that have reported numbers…Macy’s, Dillard’s, and Nordstrom. There are some pretty major comparative differences. Such as…

1) First off, let’s start with the biggest commonality – which is same store sales. Every single one of them comped within 60bp of 2.0%. That’s as tight a grouping as we recall seeing in a long time. Of course, Kohl’s will probably destroy that trend when it reports Thursday.

2) JCP definitely won with Gross Margin improvement of 461 bp, but it’s still sitting at a GM rate of only 28%, which is well below all of its competitors – even a dog like DDS.

3) JCP also wins the comparison on the SG&A line – for two reasons. The first is the 458 bp improvement in the SG&A rate, but the more important one is the fact that it’s SG&A rate is still the highest out of the group by far. We don’t think that means JCP has costs to cut, but simply that it’s productivity can improve and naturally leverage costs.

4) All good things must come to an end. Let’s move over to the cash flow statement. Cash from operations down 41%? Seriously?

5) Free cash flow margins are half that of Macy’s, and with a 271 bp decline vs last year JCP is the only company in the group to post an erosion in free cash margins.

6) Cash conversion cycle is perhaps the scariest due to a 27 day increase in days inventory on hand. You might think that the company made that up in part by extending payables, right? Nope, those eroded as well. All in, we’re talking a 31 day erosion in the cash conversion cycle. Yes, there was noise in the timing of inventory receipts. But cash is cash. Every other retailer improved it vs last year.