Editor's note: What follows below is a brief excerpt from Hedgeye Retail Analyst Brian McGough's morning research.

CRI - Carter's Leaves Much to Be Desired

So, Carter's (CRI) beat the quarter by a penny. That's obviously good enough in this tape. But the quality of earnings left much to be desired. Guidance was weak, but that's typical for CRI. They're a 'guide and beat' kind of company. But the SIGMA chart below really tells all here. The past five quarters have been a downward spiral. Margins are slowly eroding, while sales weaken and inventories build. Not good. While there are factors to explain some of this away, including international expansion, the fact is that when the line in the chart below goes down and to the left, it means that cash flow compresses.

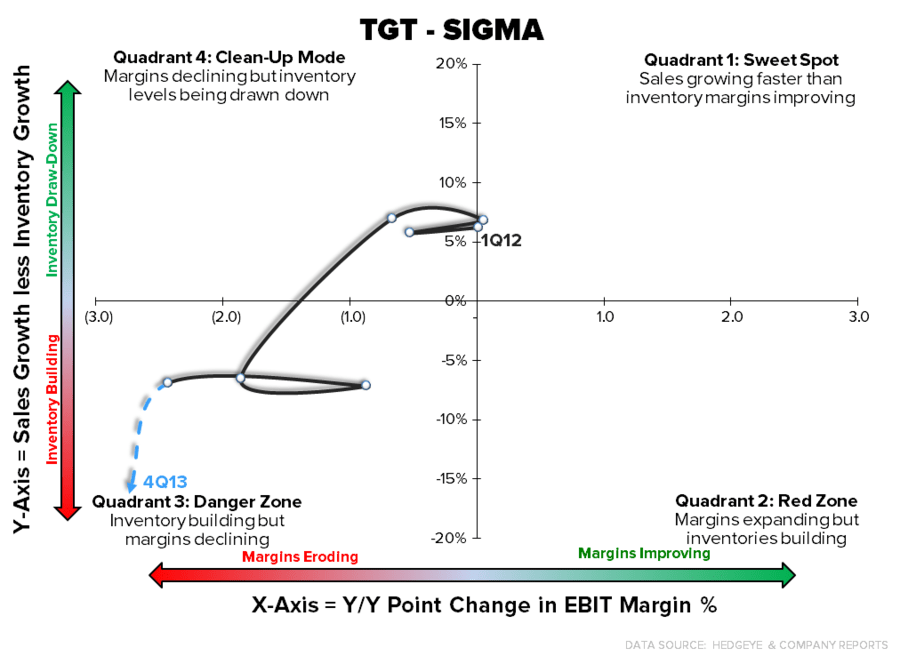

TGT - Be Weary of Target

You know what we just wrote about Carter's? Now substitute the word Target for Carters'. That pretty much sums it up.

The only real difference is that TGT's guidance in 1Q is worse than CRI's . It makes sense given that now they have to deal with their highly publicized data breach. We'll get more details on the quantification on the company's conference call at 10:30am. But it looks like Target has thrown a very beared-up scenario into their comp. But just because they set appropriate expectations, it doesn't mean that it's worth buying. Not by a long shot.