“Opium is like Gold – I can sell it at any time.”

-Robert Taylor

Per British historian Julia Lovell, that’s what one of James Matheson’s first partners told him about selling opium to the Chinese in 1818. Matheson was one of the first Scottish traders to hit the ground running (selling drugs) in China in the early 19th century.

If you’re a market #history student, it’s a fascinating story to try to understand. I’m getting into it via a book all Global Macro investors should have on their shelf called The Opium War – Drugs, Dreams, and the Making of China, by Julia Lovell (pg 25).

“The PRC’s state media works hard to convince readers and viewers that modern China is the story of the Chinese people’s heroic struggles against “imperialism” and its running dogs. In reality, the story of modern China could probably be told just as convincingly as a history of collusion with imperialism and its running dogs” (pg 13).

Back to the Global Macro Grind …

Teddy Roosevelt wrote poignantly about the American “struggle.” You know, the alarm clock – the grind - the tireless hours we commit to whatever it is that we are committed to. And since most of us are human, we have a tendency to believe that what we are doing is “right”; especially if it gets us paid.

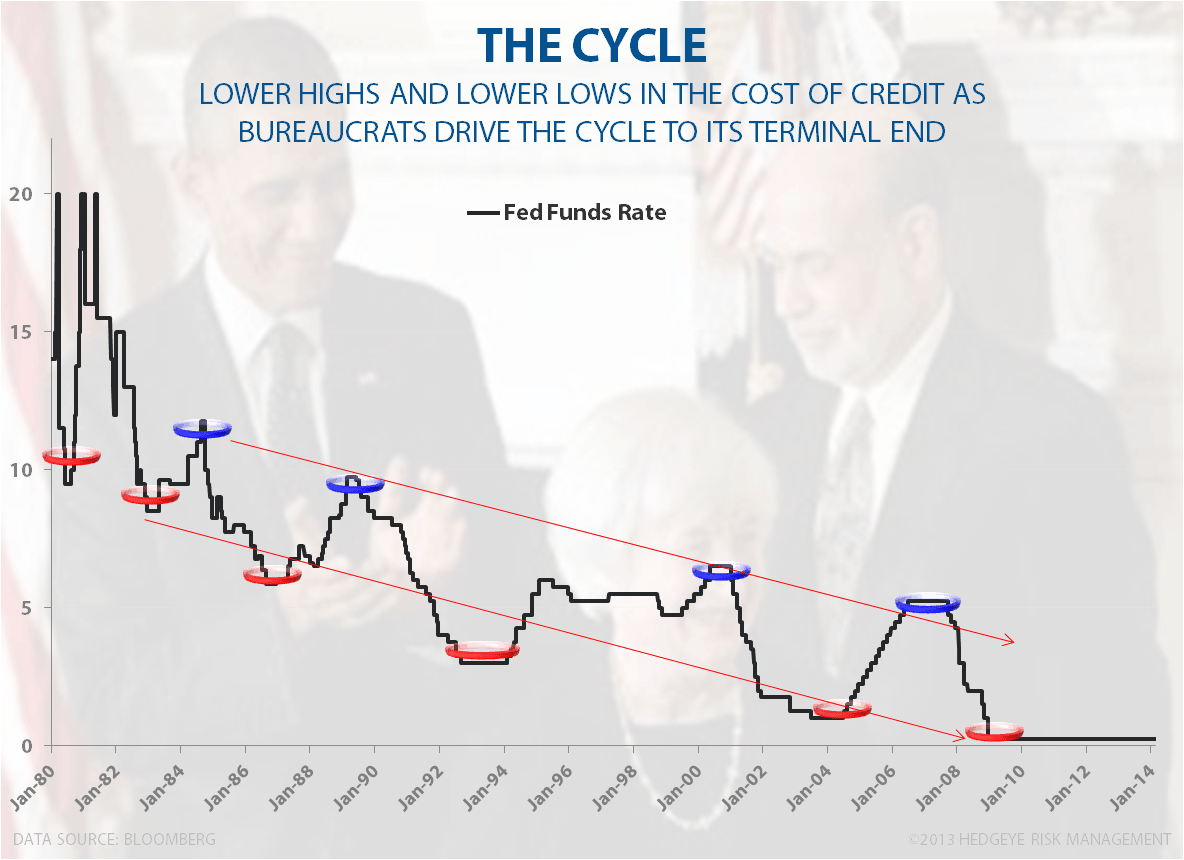

In America today, politicians are trying to pin us against one another using emotional weapons like class and gender. Leaders want the poor to think they are struggling against the rich. They want you to buy into “inequality” being someone else’s (your) fault. In reality, the 2011-2012 all-time highs in US consumer and producer price inflation is a history of US politicians perpetuating a Policy To Inflate.

Why is that?

Q: How do you have the all-time highs in prices for just about everything in your life… and both a Republican and Democrat government telling you there’s a “great recessionary risk of deflation”? A: Debt.

As John Allison simply puts it in The Financial Crisis and The Free Market Cure, “If you owe a great deal of debt (like the US Treasury) it is to your advantage to have inflation.” (pg 21)

In other news, Venezuela is considering defaulting on its debt.

That’s how this bubble story of government debt ends. And no, this isn’t a new story. Countries have been bankrupting their people via currency devaluation for centuries. There’s a 3-step default process – and it takes time:

- Politicians have to borrow from The People to meet spending promises (and get paid)

- Too much debt leads to deficits and slower growth, which fuels the need for more debt and cheaper money

- Inflation crushes real-growth; spending and liabilities run past the point of return, and the country defaults

Cool, eh?

But don’t worry, the stock markets in Argentina and Venezuela aren’t down YTD (in their burning currencies). So, in an effort to get their ratings off all-time lows, CNBC will be moving live broadcasts from NJ to Buenos Aires.

BREAKING: “stocks rally – things must be great”

Oh, and don’t forget to bring on the Top 100 Central-Planning Socialist Bureaucrats of the last 25 years for an “exclusive interview” on how they think Argentina’s Kirchners can keep it going!

Today’s morning missive was inspired by one of the best days of Institutional Investor meetings I’ve ever had in NYC. What’s fascinating about our #InflationAccelerating theme is that some buy siders really get how this ends – and some are just starting to put all of the pieces of the puzzle together.

I have a very privileged research position as I get to hear the best incremental research thoughts of some of the best investors in the world. Some are extremely well versed in the bottom-up analysis of inflation (i.e. the structural part that is born out of this government forcing companies to disinvest). It’s called constrained fixed capital formation, labor, and capacity.

No, I’m not talking about the overcapacity in things like asset managers, social media companies, and tulips. I’m talking about things like cement, fiberglass, and plumbers. Layer on the structural inflation that you’re already seeing due to capacity shortages with a cyclical rip in things like wage, rent, and commodity inflation – and voila, you find yourself approaching the aforementioned step #3.

But don’t worry, inflation that slows growth is like Gold - you can invest in it at anytime; it’s just that poor people (80% of the country) have to eat it.

Our immediate-term Macro Risk Ranges are now:

UST 10yr Yield 2.66-2.79%

SPX 1

VIX 13.06-15.55

USD 79.83-80.59

Brent 108.02-110.91

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer