This note was originally published at 8am on February 12, 2014 for Hedgeye subscribers.

“We don’t see things as they are, we see them as we are.”

-Anais Nin

We are short the consumption growth components of the US stock market. And that means we were wrong yesterday. It’s ok to say it that way – we see the real-time score for what it is, not what we want it to be.

Ellen Langer uses the aforementioned quote in a #behavioral psych book I just finished called Counterclockwise. Her concept of “mindfulness” fits how I see things in macro (on the margin). “Noticing differences is the essence of mindfulness. Don’t imagine, however, that all this needs to be exhausting… mindfulness is actually energizing, not enervating.” (pg 52)

Being wrong for a few days is a little different than being wrong for a few months (or years). When I was younger and wrong, I’d get mad. Now that I am less young, being wrong energizes me – especially when I notice something that isn’t consensus.

Back to the Global Macro Grind…

To be clear, I’m not the only one who has noticed that Janet Yellen is re-opening Pandora’s real-world inflation box with another Federal Reserve ideological “innovation” (the #untapering). Mr. Macro Market has been front-running her for 6 weeks:

- Dollar Down

- Rates Down

- Inflation Expectations Up

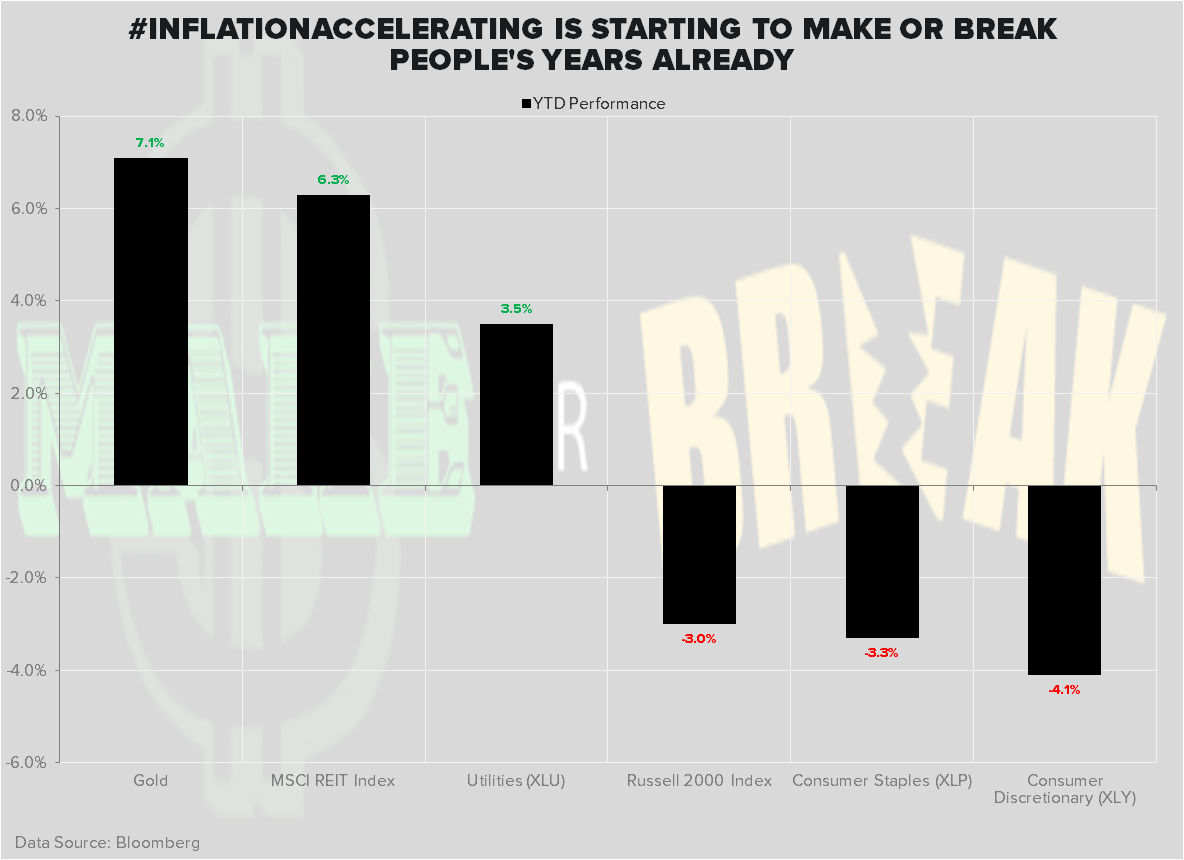

That, of course, is fantastic for slow-growth-yield-chasing asset prices like:

- Gold +7.1% YTD

- MSCI REIT Index +6.3% YTD

- Utilities (XLU) +3.5% YTD

Not to be confused with US #GrowthAccelerating asset prices like:

- Consumer Discretionary (XLY) -4.1% YTD

- Consumer Staples (XLP) -3.3% YTD

- Russell2000 -3.0% YTD

Alongside Boehner waiving the debt limit last night (without conditions!), what we have here is another Big Government policy investing-style shift towards #InflationAccelerating. This isn’t new. It’s what happened to the Dollar in both Q1 of 2008 and 2011. Inflation is a tax.

The inflationary concept that zero isn’t zero is what the Fed calls “policy innovation.” Happy #Darwin Day! #1806

In Q1 of 2008, Bernanke whispered to his boys that he was going to do the “shock and awe” thing and cut to zero; so, while demand was slowing, Oil prices ripped humanity a new one by the summer time ($150/barrel), perpetuating US #GrowthSlowing.

In Q1 of 2011, Bernanke continued to send sweet nothings down his communication pipes that zero really wasn’t zero – it was zero minus whatever # of QE’s he damn well wanted. The CRB Commodities Index, Gold, etc. ripped to all-time highs, US consumption growth slowed, and Utilities (XLU) closed the year +14.8%.

In Q1 of now, zero still really isn’t zero because you have to:

- Subtract 2 tapers from the 0 minus 3-4 QE’s

- Then add expectations of un-tapering to the 2 tapers…

- And add a minus taper to a real-rates # … and you get a dovish Dollar

Or something like that.

The Fed, of course, doesn’t see it this way. But no matter how they want to see their theoretical world, market expectations and prices see them the way the real-world is.

While I am sure this will all end well, can the US stock market continue higher? Obviously the answer to that is yes. But what parts of the market will lead? Will they be food/energy inflations, real-estate inflations, and/or some of those beauty MLPs?

I don’t know anything about nothing, but I am certain that everything that you eat, put in your car, and pay for from a housing perspective has nothing to do with inflation or your cost of living.

In other news, as both the British Pound and Euro gain strength versus Yellen’s Burning Buck, both the UK and German governments are taking up their GDP growth estimates for 2014 (British Pound remains our favorite currency vs USD).

How that #StrongCurrency correlation to growth thing works is cool. It’s too bad that un-elected and unaccountable US central planners aren’t paid to see the history of currency appreciation, real-purchasing power, and consumption growth for what it is.

Our immediate-term Macro Risk Ranges are now (all 12 macro ranges are in our Daily Trading Range product):

SPX 1730-1828

VIX 13.21-17.61

Pound 1.63-1.65

Brent 107.84-110.03

Nat Gas 4.57-5.34

Gold 1260-1291

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer