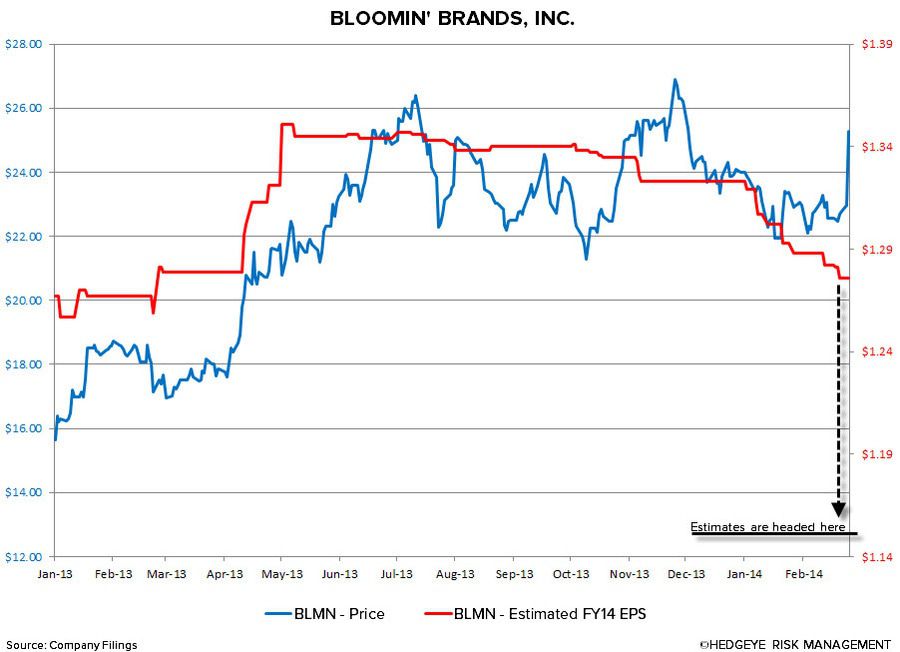

BLMN remains on the Hedgeye Best Ideas list as a SHORT.

SOLID 4Q13 RESULTS

BLMN reported 4Q13 results mostly in-line with expectations before the open. Total revenues of $1.051 billion and adjusted EPS of $0.27 slightly beat expectations by $3m and $0.01, respectively. Total revenues increased 5.2% YoY, driven by revenues from new restaurants, an increase in comparable sales and the consolidation of one-month of sales generated by Brazil operations. EPS growth was driven by marginally stronger restaurant level margins, due to higher AUVs and productivity savings, and lower corporate and compensation expenses.

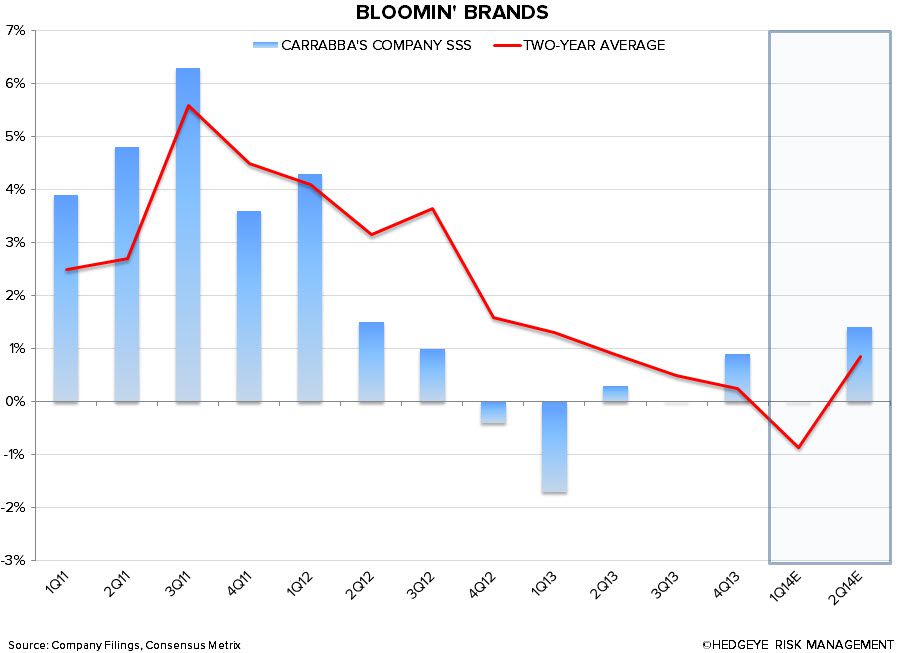

Comparable store sales at BLMN’s two biggest brands fell short of street estimates. System-wide, Outback and Carrabba’s comps missed expectations in 4Q13 by 10 bps, 50 bps and 50 bps, respectively. Outback and Carrabba’s disappointed despite growing their lunch business by a large margin in 4Q. At the end of the quarter, weekday lunch was being offered at approximately 35% of Outback locations and 40% of Carrabba’s locations. This is up significantly from the third quarter, when only 26% of Outback locations and 28% of Carrabba’s locations offered weekday lunch. With this degree of daypart expansion, these two concepts should be expected to grow traffic and outperform the industry. Outback only managed to grow traffic 0.5% and management didn’t reveal traffic trends at the Carrabba’s brand. Bonefish and Fleming’s comps beat expectations in 4Q13 by 80 bps and 70 bps, respectively.

Although 4Q13 was a difficult quarter for many casual dining operators, BLMN managed to outperform the Black Box Index by 150 bps. The 1.4% system-wide comp growth was driven by increases in price and traffic, partially offset by a lower mix due to lunch expansion. This number also benefitted 40 bps from a calendar shift in the quarter. Traffic grew by 0.3% in the quarter, consistent with what is to be expected of a company rolling out lunch across multiple brands.

Two-year sales trends remain weak across all four concepts.

GUIDING DOWN FY14

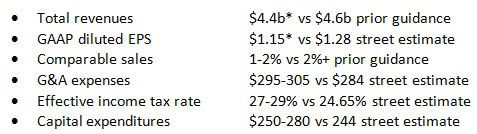

Street estimates for FY14 proved too aggressive as management reigned in guidance and expectations across the board.

FY14 Financial Outlook

*Guidance indicates the low-end of management’s range

There were clearly some positives in the quarter, but there are also several signs that the underlying trends are not as strong as management is portraying. That being said, we will revisit our short case and provide an updated outlook in the coming days.

Howard Penney

Managing Director