This note was originally published at 8am on February 11, 2014 for Hedgeye subscribers.

“If I had a mind to rent pigs, I’d be mighty upset. A man that likes to rent pigs won’t be stopped.”

-Larry McMurtry, Lonesome Dove

Lately I’ve been watching the famed late 1980s mini-series, “Lonesome Dove”, on Netflix. It is based off of the Pulitzer Prize winning novel by Larry McMurtry of the same name. The novel tells the story of two former Texas Rangers, Captain Augustus “Gus” McCrae and Captain Woodrow F. Call, who run a livery called the Hat Creek Cattle Company in the desolate Texas border town of Lonesome Dove.

The bulk of the plot involves the decision by McCrae and Call to leave the relative complacency of Lonesome Dove and drive a massive herd of cattle north to the Montana Territory. On the way north, they encounter a plethora of adventures, including proverbial dust ups with the army, bandits, and Indians.

By far, the savvy plains Indians (Native Americans) are the most formidable challenge McCrae and Call face on their journey. In reality, this is no surprise since the Natives occupied the land for thousands of years before the European settlers arrived and developed many proprietary ways of surviving off the land without the benefit of modern technology.

One such proprietary method of hunting was the Buffalo Jump.

It was a simple, but very effective method of collecting a massive amount of buffalo meat. On horses or foot, the Natives would chase buffalo herds towards, and eventually over, a sharp cliff. Tribesmen waiting below would finish off the buffalo and butcher the meat. The key of course was that buffalo had no idea they were running towards, and eventually over, a cliff.

Back to the global macro grind . . .

While it is an apt analogy, we are not yet ready to say that the global economy is going over the cliff, but the fact remains that much of the data we’ve been collecting and watching is getting incrementally more negative. Yesterday in our morning meeting, Hedgeye’s Asian Analyst Darius Dale emphasized that he is getting a little more cautious on China.

They key reason for his shift is that money market rates continue to back up. This is a point that is emphasized in the Chart of the Day. Further, while the government could choose to intervene, the People’s Bank of China is instead opting to let the markets settle on their own. According to a February 8th PBOC report:

“When the valve of liquidity starts to tame and curb excessive credit expansion, money-market rates, or the cost of liquidity, will reflect that. The market needs to tolerate reasonable rate changes so that rates can be effective in allocating resources and modifying the behavior of market players.”

In the long run, this is likely a positive for the Chinese economy. In the short run, of course, higher money-market interest rate volatility is likely a headwind.

The caveat on getting aggressively negative on China is that GDP comps are relative easy for China and seasonality should also be a positive in the reported numbers this quarter and next. In part, this is likely why the Shanghai Composite is up +0.85% this morning and +3.5% this month – a move that may have some legs if the PBOC decides to cut the Reserve Rate Ratio (RRR) as is rumored this morning.

The novel Lonesome Dove is also somewhat apropos as newly minted Federal Reserve Chair Janet Yellen is scheduled for her debut in front of the House Financial Services Committee this morning, which will include Q&A. Interestingly, there will be a second panel of witnesses that will react to Dr. Yellen’s testimony and will include:

- Dr. John Taylor, Professor of Economics, Stanford University;

- Dr. Mark Calabria, Cato Institute;

- Abby McCloskey, American Enterprise Institute; and

- Dr. Donald Kohn, Brookings Institution.

So, we will see soon enough if Dr. Yellen is a Lonesome Dove or as my colleague Keith McCullough called her in this video the "Mother of All Doves." Either way, her commentary this morning is likely to have some impact on a stock and bond market that continues to be myopically focused on interest rates and Federal Reserve policy.

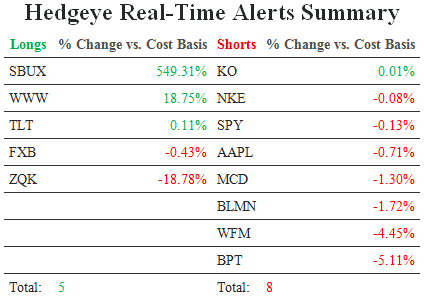

Speaking of headwinds, one of our Best Idea short positions Boardwalk Pipeline Partners (BWP) faced a few of them yesterday as the stock closed down -46%. We obviously don’t get them all right, but our Energy Sector Head Kevin Kaiser nailed this one. Interestingly, BWP didn’t miss its EBITDA estimate by all that much, but did cut its distribution by more than 80%.

A key tenet of our short call on MLPs in general is that their distributions are quite often an illusion as MLPs borrow money, issue equity and buy companies to maintain the distribution. Investment bankers then “value” MLPs based on the yield, rather than the actual intrinsic value of the assets, and sell these financial products to unsuspecting retails investors. This whole scheme works fine until the proverbial company goes over the Buffalo Jump and distributions get cut.

If you are invested in MLPs and / or looking for good shorts, I’d highlight recommend you subscribe to our Energy Sector research. Anyone on our sales desk, sales@hedgeye.com, can help get you signed up. The best risk management is to avoid blow ups like BWP and we seem more MLPs on the horizon that are headed for the cliff.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.60-2.76%

SPX 1734-1814

VIX 14.06-20.41

USD 80.33-88.08

Gold 1251-1287

Keep your head up and stock on the ice,

Daryl G. Jones

Director of Research