We remain bullish on European equities over U.S. equities on the margin.

In the charts below, we add our updated commentary.

Quantitative – European equities are flashing bullish TRADE and TREND signals, per the STOXX 50 and Euro STOXX 600. Our preferred equity markets remain Germany (EWG) and the UK (EWU).

YTD the equity markets have broadly rallied off a bottom in early February: Denmark (+13.5%), Portugal (+10.7%) and Ireland (+10.4%) are topping ytd returns while Russia remains the clear laggard (RTSI -8.6% and etf RSX -11.1%), reflecting the political uncertainty in Ukraine and challenged fundamentals.

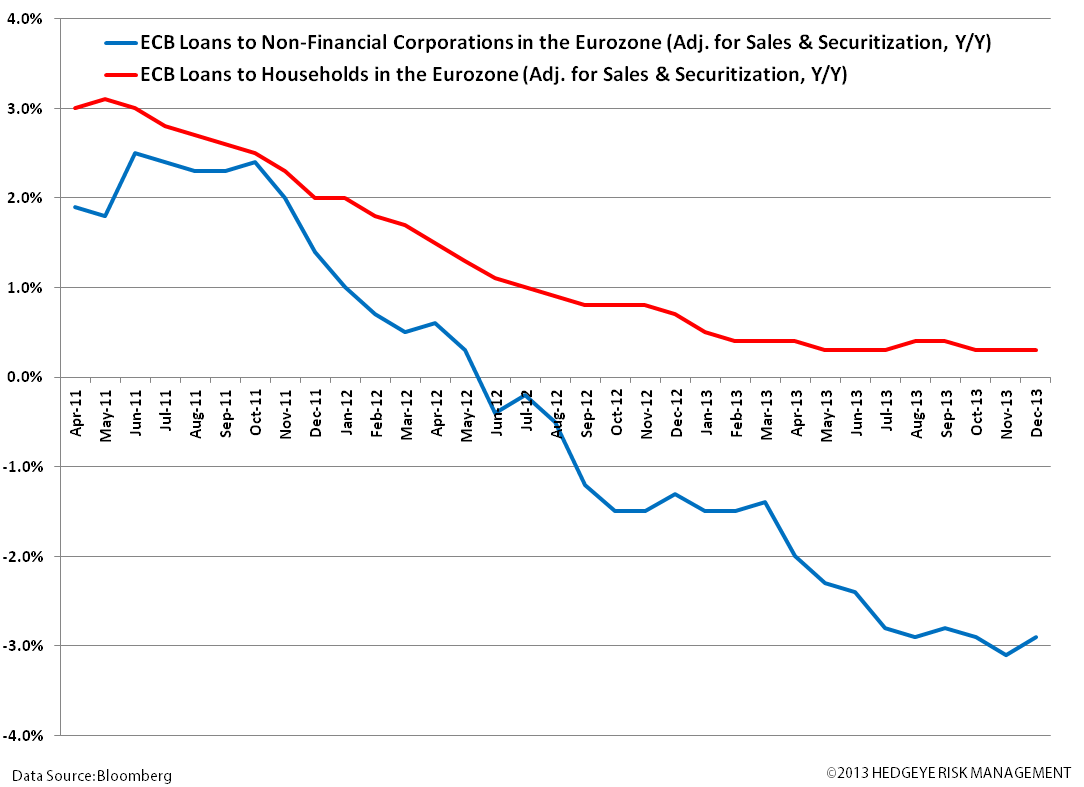

Policy – We expect ECB President Mario Draghi and the Eurocrats to continue to grease the skids, which should propel equities higher. This includes not letting any member state “fail” (sovereign default or exit), managing the banking system, keeping rates “accommodative” or lower, pushing for schemes to unlock lending to the real economy (especially SMEs), and remaining concessionary on fiscal austerity targets.

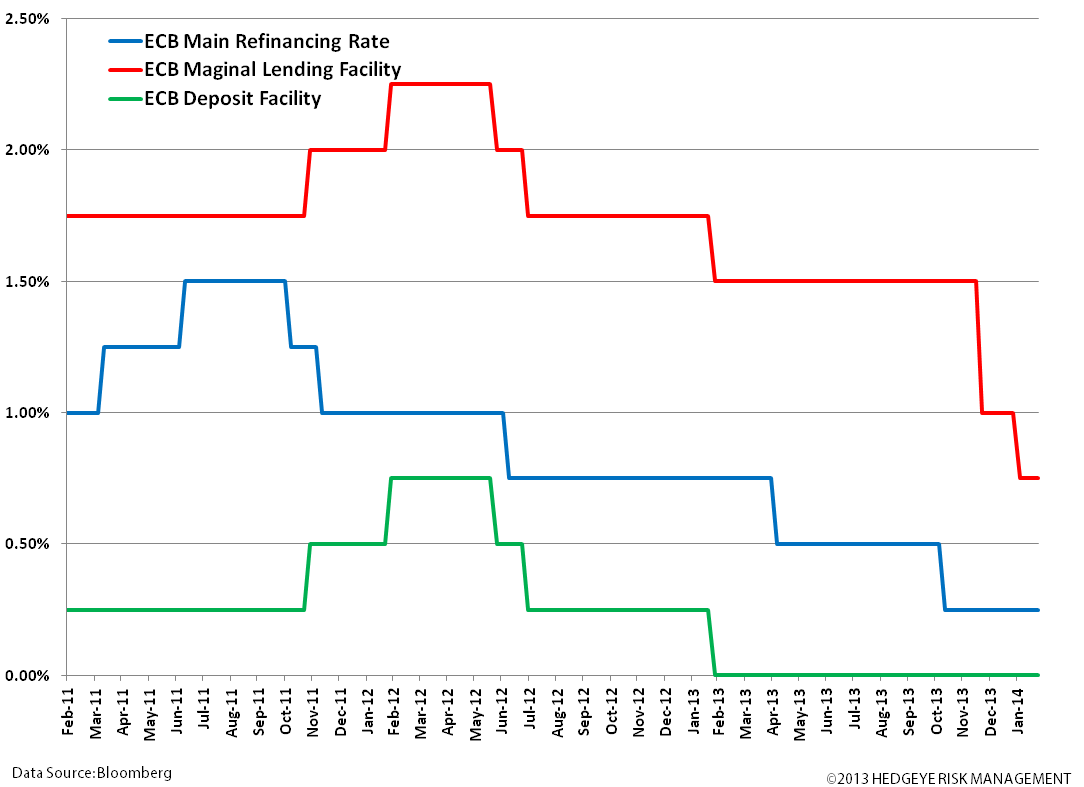

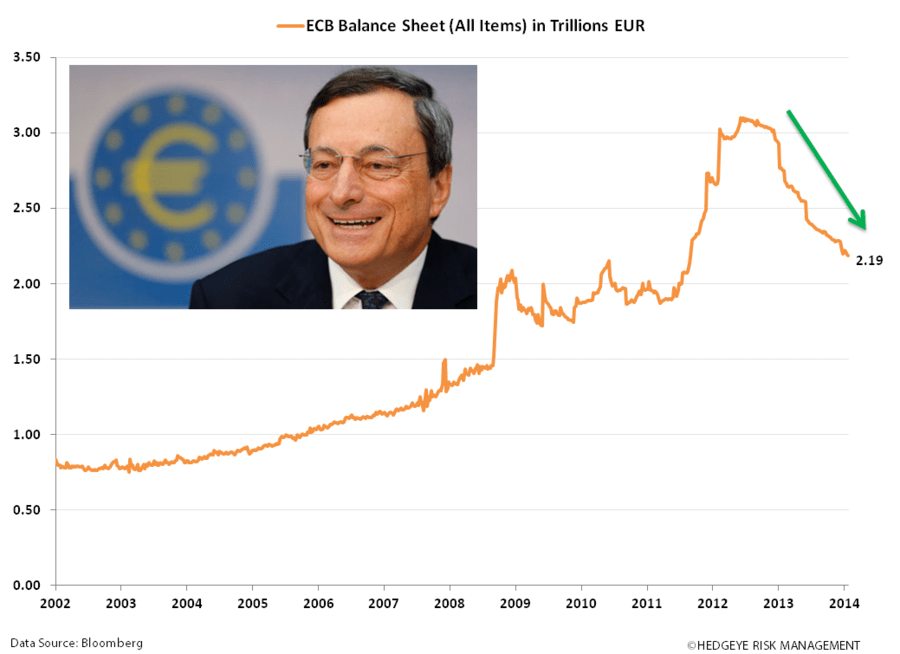

Note: over the weekend Draghi said that the March 6th policy meeting will be critical in determining whether the ECB will provide additional stimulus. He said that by then it will have a full set of information needed to decide whether to act or not. Whether this means an interest rate cut to zero (currently the main refinancing rate stands at 0.25%) and/or some new loan package (to spur a stalled channel -- with room on the balance sheet given LTRO paybacks), or something else altogether, we believe the go-forward policy will continue to support the equity market and put a floor in the EUR/USD. Any indication that the Fed’s Yellen is taking her foot off the taper program (which we think is likely) should also boost the cross (see levels below).

Outlook – Eurozone Q4 2013 Preliminary GDP surprised to the upside at +0.5% y/y vs consensus +0.4% and prior -0.3%. The ECB is still forecasting Eurozone 2014 GDP at a modest +1%. We expect inflation to be grounded under +2% for at least the next couple of years. Minimizing the consumption tax should continue to boost consumer and business confidence. Eurozone CPI in January stood at +0.8% versus an initial reading of +0.7%. We expect #GrowthAccelerating off low levels throughout Europe and investors to pile into the trade given such forces as EM headwinds and dovish policy out of the Fed.

Political – While Italy’s political scene and structure remains anything but stable, we see the transition to Italy's new Prime Minister, Matteo Renzi, over the weekend as at least a stabilizing force over the near term. The ousting of Ukrainian President over the weekend should also minimize some of the geopolitical forces influencing the market over recent weeks.

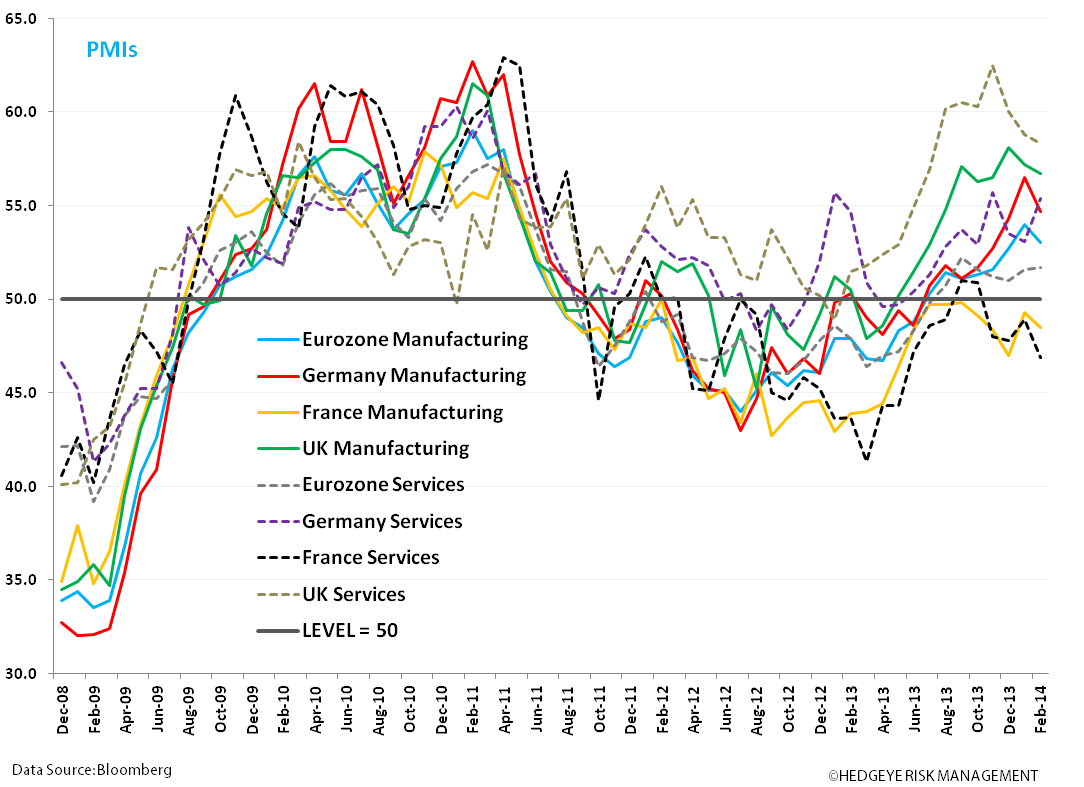

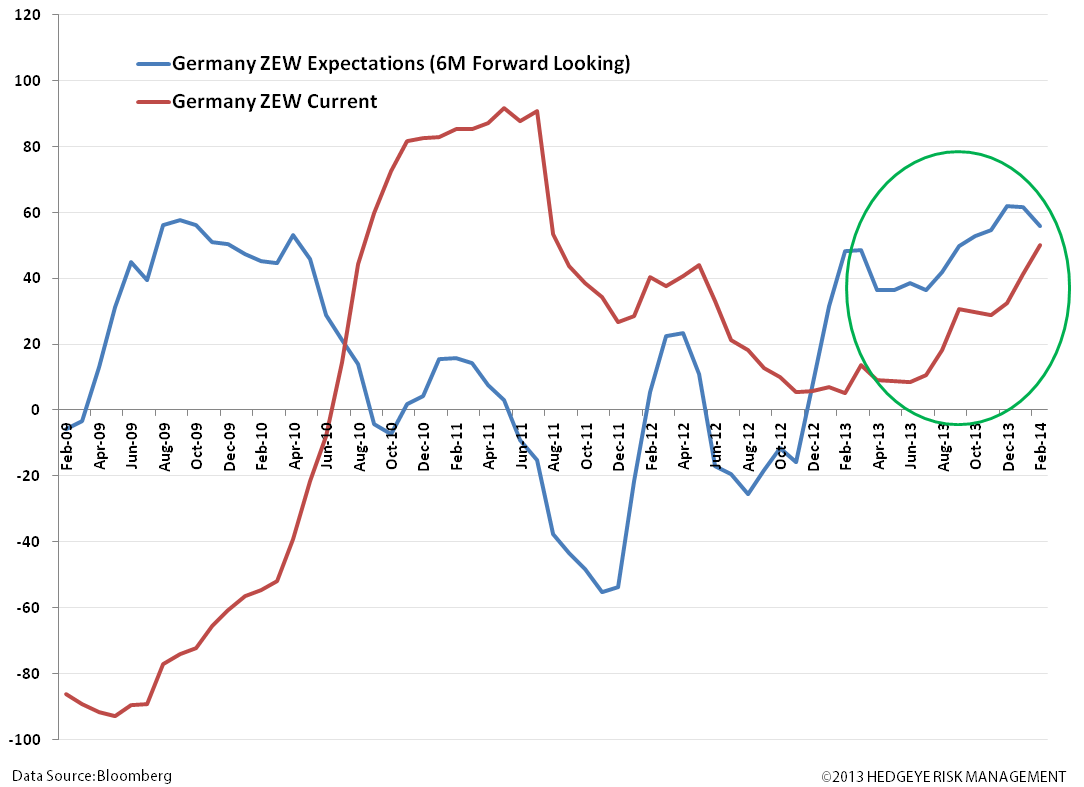

Fundamentals & Sentiment Surveys – There’s been mixed data points over recent weeks. Preliminary PMIs for February for the major economies showed a slight dip for Manufacturing, while Services broadly grew (France the exception). Survey work from IFO on German Business expectations showed broad improved in February, while the ZEW survey for forward-looking economic expectations dipped for both Germany and the Eurozone aggregate. Our trend bullish outlook, however, remains intact.

- The WSJ recently confirmed our outlook, reporting increased appetite from U.S. fund managers for European equity funds since the start of the year due to an improving economic outlook and low interest rates. It noted data from fund tracker EPFR, which indicated that $24.3B has flowed into European equity funds this year through 19-Feb, while U.S. stock funds have seen $5B in outflows.

- Also, over the weekend George Soros said in the weekly Der Spiegel magazine that he wants to invest in Europe's financial sector. Soros said he believes in the euro and could pump money into banks which urgently need capital. He said his team is also considering investing in Greece and noted improved economic conditions there.

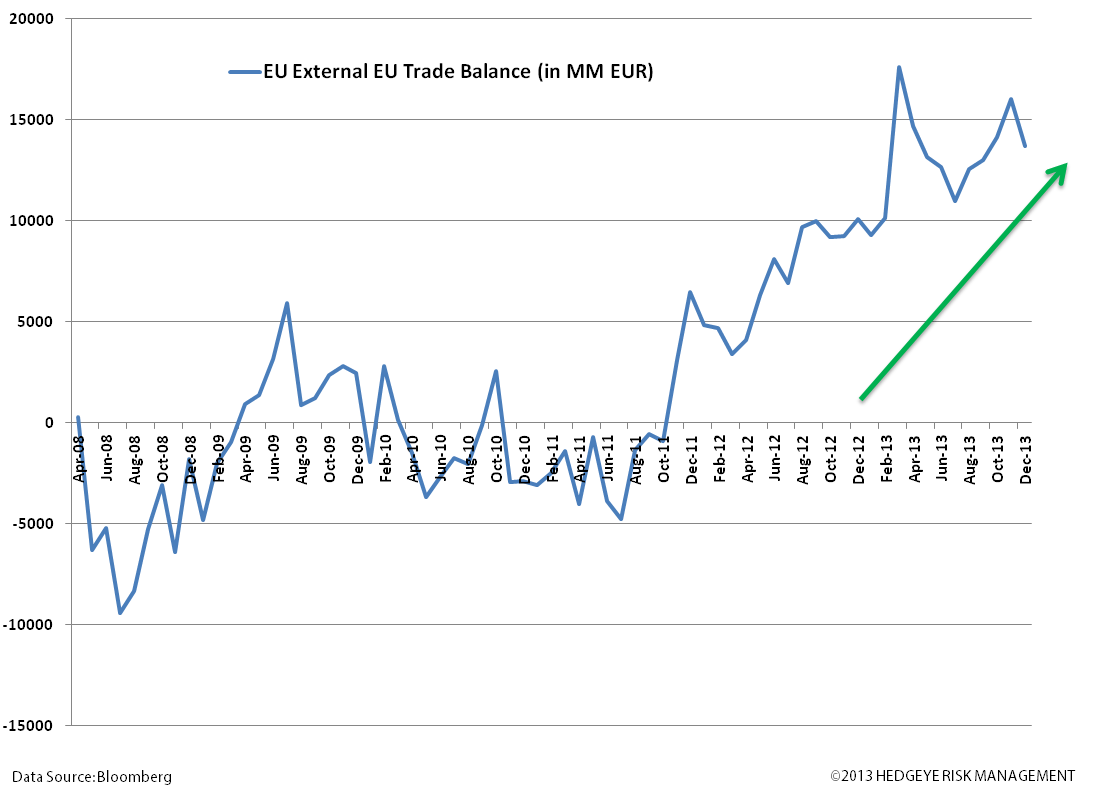

Below we show updated Trade Balance and Current Account data, both of which are supportive of an improving economic climate.

Not that we put much worth in the ratings agencies, but as a positive sign to investors, Moody's upgraded Spain's rating to Baa2 from Baa3 and assigned a positive and upgraded Spain's short-term rating to (P) Prime-2 from (P) Prime-3, citing the rebalancing of the Spanish economy towards a more sustainable growth model.

Finally, European Auto Sales remained strong in January, up +4.6%, another signal to us of strong confidence to make big-ticket purchases.

We're data dependent, but for now staying with our bullish call on European equities over U.S. equities, and our positive outlook on the EUR/USD (FXE) and GBP/USD (FXB).

Matthew Hedrick

Associate