I spent some time with my daughter at the University of Richmond this weekend and decided to take her and her three roommates out to dinner Sunday night. I suggested we go to Olive Garden! After a few strange looks, I had to explain it was part of a research project and, eventually, they agreed to go.

Just as we were being seated, one of my daughter’s friends said, “This place looks like a cafe in a nursing home.” Moving past the opening comment, the salad, bread sticks and calamari were a hit, but the pasta dishes, well, not so much – even for college kids on a meal plan.

Today, we woke up to the news that Starboard could potentially call a special meeting to halt the spinoff of Red Lobster. As we wrote in our note, “Clarence’s Legacy, A Half-Baked Plan,” back when the plan was announced, Mr. Otis’ legacy will be defined by his unwillingness to make the changes necessary to create significant value for shareholders. We also expressed our concerns with management’s plan because, to us, it made little strategic sense and didn’t get at the heart of the problem.

Darden is still a company with an inefficient operating structure.

On the day Darden’s strategic plan was announced, the stock closed down 4% to $51. This didn’t exactly strike us as a vote of confidence in management’s plan to create value. Two days later, Starboard Value announced a 5.5% position in the company and the stock rallied 6%. For the most part, the stock has traded sideways since then, until rallying 3% on the news that Starboard retained former Olive Garden president Brad Blum to serve as an advisor in its battle against Darden.

The takeaway from stock action and, in our opinion, sentiment since 12/20/13 is the stock rallies when there is movement toward replacing management and sells off when management publicly digs their heels in.

We’ve heard management talk about a plan to fix Olive Garden for five years now. After last night’s experience, I can personally confirm (including three witnesses) that the chain continues to over promise and under deliver. The current team has had ample time to fix the brand and has failed miserably.

It is time for significant change at Darden.

To review, we’ve included our updated thoughts on why management’s plan to spinoff Red Lobster makes very little strategic sense.

INCONSISTENCIES IN OTIS’ STRATEGIC RATIONALE

“Transaction transforms the portfolio into two independent companies that can each focus on separate and distinct opportunities to drive long-term shareholder value.”

HEDGEYE – Our proposed plan transforms the portfolio brands into four independent companies that have leading market share in their respective categories. These NewCo's would be comprised of New Italian, New Seafood, New Steak and New Growth (Yard House, Seasons 52, Eddie V’s, and Bahama Breeze). Each company will be driven by an intensive focus on a single operating priority and shareholder value creation.

According to Otis, the Old Darden had eight brands with “divergent operating priorities” and the New Darden will have seven. Despite admitting the company has divergent operating priorities, management wants us to believe spinning of the Red Lobster brand will solve this issue. They couldn’t manage eight brands; we don’t see why they’d be able to manage seven.

“Separation will allow New Darden and New Red Lobster to better serve their increasingly divergent guest targets.”

HEDGEYE – What about the divergent guest targets among Olive Garden, Yard House, Capital Grille and so forth? A changing consumer dynamic creates the need for intensive focus on key guest targets; the New Darden is anything but focused. Our plan creates four operating companies focused on: Italian, Seafood, Steak and Growth. This would properly allow for intensive focus on guest targets and specific brand priorities in each respective category.

“Separate organizations enable New Darden and New Red Lobster to better focus on their divergent value creation levers.”

HEDGEYE – This is nothing more than a bunch of filler. It’s unnerving to think management believes they can spin this idea as a strategic plan. Leading full-service restaurant companies are vastly outperforming Darden because they are more nimble and have more focused operating models.

“Announced compensation changes for New Darden and planned program for New Red Lobster will result in appropriate incentives for management teams passionate about their respective businesses.”

HEDGEYE – You don’t need to split the company to do that. If the Old Darden wanted compensation closely tied to each respective business, this could’ve easily been enforced. Management teams shouldn’t be in place if they aren’t passionate about their business.

“Separation repositions the business to better serve differing shareholder investment requirements (growth and income vs. income/yield) and maximizes total shareholder value.”

HEDGEYE – The guidance for the New Darden looks the same as the guidance for the Old Darden. We don’t see how this strategic plan better serves the different investment requirements of its brands.

All told, the plan presented in December seems reactionary and hastily put together. It fails to address declining traffic, margins and relevance as well as potential solutions to these issues.

After a series of conversations with industry insiders and some independent thinking, we’ve concluded that Darden’s strategic initiatives could actually end up destroying shareholder value.

THE POTENTIAL FOR VALUE DESTRUCTION

Red Lobster may become less profitable and, as a result, less valuable.

By spinning off the Red Lobster brand, management is essentially kicking a brand that is already down. What message does this send to Red Lobster’s rank and file employees? This decision could create a lot of angst among the employee base and could perpetuate underperformance. In fact, under this plan, the probability that the brand sees an accelerated decline in profitability increases significantly.

The plan does not address the issue of managing multiple brands.

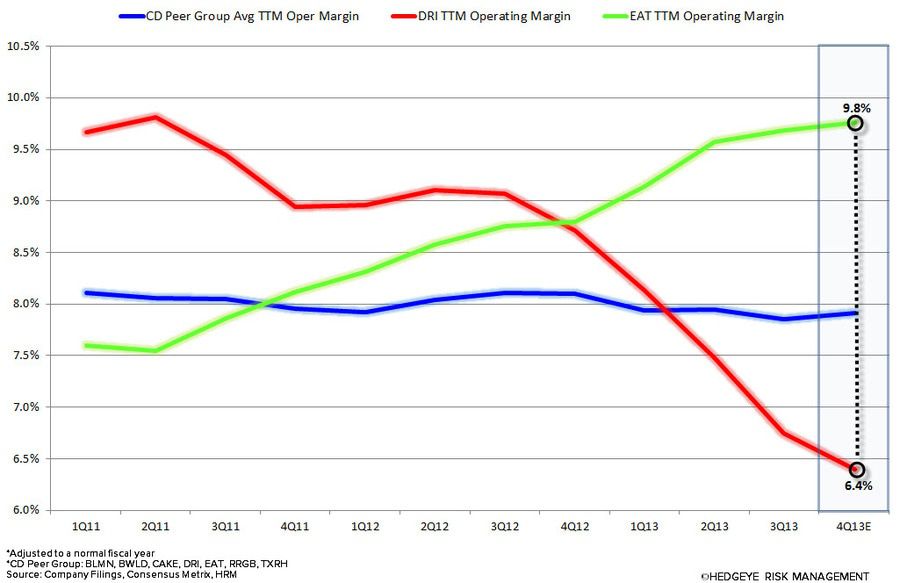

This strategic plan fails to address Darden’s largest issue: the portfolio is too large and too complex to perform. We believe its current multi-concept structure has created significant inefficiencies in the operating structure of the company.

Management’s proposed initiative simply removes one underperforming brand from a large portfolio. Our plan to fix Darden organizes the portfolio in a way that would be beneficial to each NewCo.

Clarence is building a moat around his castle.

After years of underperformance, we’d expect someone to be held accountable. So Clarence has been deflecting blame and firing the people around him. He needs to be held accountable. He is the Chairman and CEO of a company that has struggled mightily over the past several years. When will he accept responsibility for his decisions?

They are not cutting unit growth or costs as aggressively as they should.

Darden plans to halt unit growth at Olive Garden for a few years, slow unit growth at LongHorn and slightly slow unit growth at SRG in FY14. This reduction in unit growth is expected to shave $100 million off of capital expenditures annually. We don’t believe management wants to slow unit growth. Rather, we believe they are being forced to in order to maintain the current dividend. Darden should halt growth all together and address their issues before they exacerbate them.

Further, through support cost management, the team expects annual savings of $60 million beginning in FY15. This is up from the $50 million the company had previously announced. For a company riddled with excessive spending, we find it discouraging that management was only able to find an additional $10 million in annual cost savings. Management must cut costs more aggressively if they intend to unlock significant shareholder value.

There is no real plan to fix Olive Garden.

The company hasn’t released any compelling details around fixing the Olive Garden brand. Considering the brand will make up approximately 60% of the New Darden, this should be their top priority. We’ve heard infrequently about the “Brand Renaissance” plan, but management has been rather quiet on this front for “competitive reasons.” Considering its waning relevance, declining traffic trends and the addition of a cheeseburger to the menu, we believe the brand has lost its way.

Management has lost all credibility to hit targets.

This was evident during the most recent earnings call. One analyst, in particular, confronted management about this:

“It seems in the presentations that you gave us that the key to whether this could create value or not is on those operating income growth numbers, low to mid-teens at the New Darden and mid to high-single digits at the New Red Lobster. Why are those credible given the track record?”

We knew FY14 guidance was too aggressive and saw a massive miss coming in the first quarter. What we didn’t see coming was management’s reluctance to guide down FY14 numbers after this miss. After another disappointing performance in the second quarter, management was forced to guide down full year estimates. As a result of these massive misses, they are losing credibility from others on the street. If they don’t hit the targets laid out in most recent earnings call, they will fail to create any shareholder value despite these strategic initiatives.

Recent Notes

02/20/14 DRI: CRITICAL SHOT FIRED

01/29/14 DRI: THE PRESSURE COOKER IS BUILDING

01/22/14 DRI: NEWTON’S FIRST LAW

12/20/13 CLARENCE’S LEGACY, A HALF-BAKED PLAN

12/19/13 DRI: NOT ENOUGH

12/17/13 BEST IDEA UPDATE: LONG DRI

12/11/13 RESTAURANT IMPOSSIBLE: FIXING OLIVE GARDEN

10/30/13 DRI: PENDING FY2Q14 DISASTER?

Call with questions.

Howard Penney

Managing Director