“We live in a house, and therefore we consume the house.”

-John Allison

Yep, I am Canadian.

I lived in a Canadian house until I was 24 years old and have the flag tattooed on my back. Consequently, I will be consumed by my confirmation bias today as Canada’s men try to beat America’s like our women did yesterday.

Don’t worry, I’m not competitive or anything. When my all-American wife (Laura in Lacrosse) wasn’t looking one day, I hung a massive Canadian flag over my son Jack’s bed. As he was sleeping, I subliminally got him in the mind!

Admittedly, I have started to teach all 3 of my children that the USA is the best in the world, at creating asset bubbles. Just like John Allison does in the aforementioned quote about real-world economics, I have to call it like it is.

Back to the Global Macro Grind …

“In economic terms, spending on housing is consumption, not investment… houses are not used to produce other goods… thus the misinvestment in housing in housing shifted resources from production to consumption.” –John Allison (pg 8)

No, “misinvestment” isn’t a word that spell-checks inasmuch as “misinformation” did for a Canadian hockey player (me) in the mid-1990s when it was introduced to me by one of the great leaders in my life (former US Olympic Hockey Coach, Tim Taylor).

“Mucker, you don’t really have any moves… so you need to start waggling the blade of your stick when you are carrying the puck up ice to give the defense some misinformation.” –Tim Taylor

Try it – it works!

Longer-term, an un-elected central planning bureau (The Fed) forcing investors to chase short-term price inflations (and “yields”) to all-time bubble highs won’t work. Anyone who didn’t sleep through the deflation of asset prices in 2008 will get that.

I had a lot of feedback on John Allison’s “fundamental themes” yesterday (mainly because I left 3 of his top 6 out). They are:

1. “Individual financial Institutions (#OldWall) made very serious mistakes that contributed to the crisis

2. “The deeper causes of our financial challenges are philosophical, not economic”

3. “If we don’t change direction soon, the United States will be in very serious financial trouble in 20-25 years”

In other words, the government (and The Federal Reserve) created policies based on academic ideologies (weak currency “boosts exports”, cheap money “boosts housing”, etc) that are A) very short term in nature and B) misaligned with making long-term investments in productive, job generating, assets.

Newsflash: Gold is the least productive major “asset class” in the world – so it loves #InflationAccelerating-slow-growth government policies to fix prices (rates and wages) and devalue the purchasing power of The People in exchange for debt.

The Canada vs. USA score won’t lie today. Neither will the misinvestment, misinformation, or misalignment of the US stock market’s YTD score vs. economic reality (after torching their currencies, Venezuela was +460% last yr and Argentina is +10% YTD).

If you peel back the -0.5% and +9.5% YTD returns of the SP500 and Gold, respectively, and look at the S&P’s Sector Returns:

- Slow-growth-yield chasing Utilities (XLU) lead the charge at +6.7% YTD

- Consumer Sectors (XLY and XLP) lead losers at -2.6% and -3.0% YTD, respectively

- Interest Rate Sensitive Financials (XLF) are underperforming the SP500 at -1.9% YTD

#InflationAccelerating A) slows consumption growth (hurts consumer stocks) and B) encourages investors to chase “yield.” That’s why the Financials (XLF) suck relative to Utilities (XLU) this year inasmuch as they did at the start of 2011.

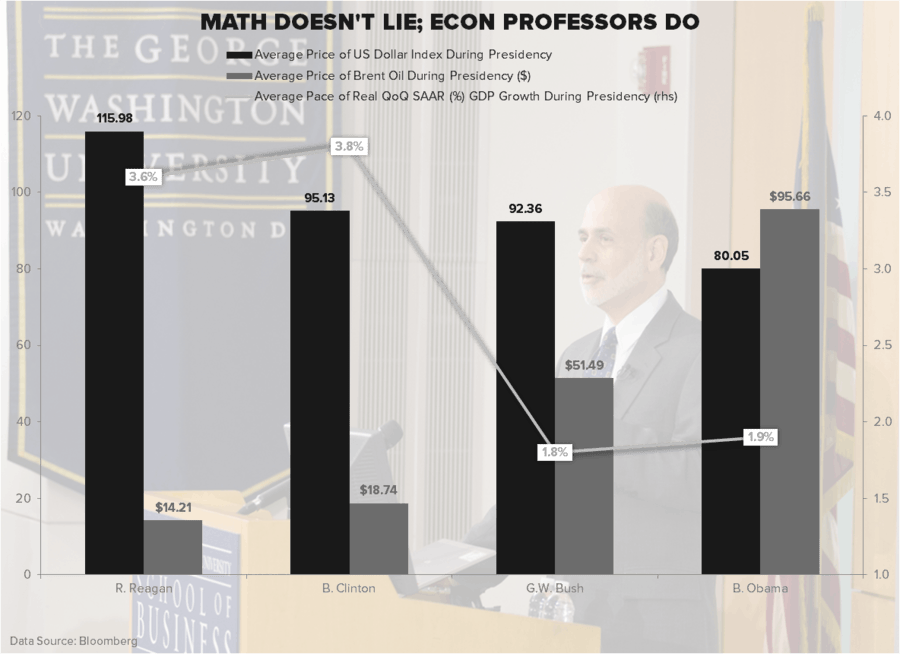

Put another way, as the Financials, Rates, and the US Dollar go, so will real-economic growth in America. The only modern periods of sustainable US economic growth (i.e. greater than 4% GDP) came in the 1 (Reagan) and 1 (Clinton) years. You saw a sneak preview of interest rates and the US Dollar breaking out to the upside in Q3 of 2013 too (US GDP ramped to +4.12%).

That wasn’t my house versus your house. That wasn’t Canada vs. the USA either. That’s how real-world economics works. The only misinformation about it in the US, Japan, Venezuela, etc. today is in how governments and their central-planning-access starved media group-thinkers sell it to you. From a free market capitalist perspective, it’s so very un-American.

Our immediate-term Macro Risk Ranges are now:

SPX 1811-1848

Nikkei 14124-14966

VIX 13.31-15.98

USD 79.91-80.55

Pound 1.65-1.67

Gold 1

Best of luck to both Team Canada and Team USA today,

KM

Keith R. McCullough

Chief Executive Officer