Kinder Morgan Energy Partners (KMP) - one of our Best Ideas on the short side (since September 2013) - released its 2013 10-K on 2/18. As part of our process, we closely review the SEC filings of our Best Ideas. In our experience, companies press release what they want to disclose and file what theyhave to disclose. We discuss six key topics from KMP's 2013 10-K in this note:

1. KinderHawk may lose ~$120MM in annual EBDA over the next two years

2. E&P results were weak in 2013

3. KMP's Goldsmith PV-10 begs further questions

4. New maintenance CapEx definition and added disclosure

5. On KMP’s rate cases and potential refunds

6. Miscellaneous quotes, comments, and questions from the 10-K

---

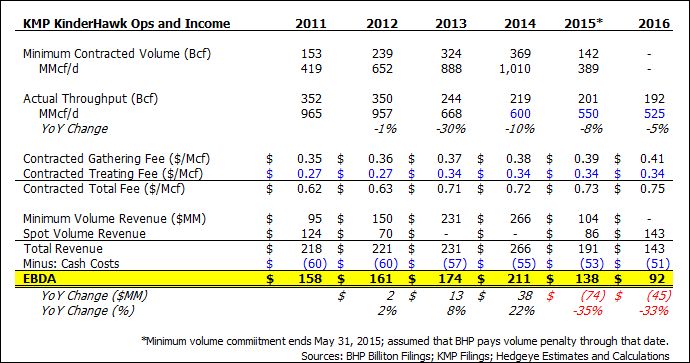

1. KinderHawk may lose ~$120MM in annual EBDA over next two years......The table on page 13 of KMP's 2013 10-K has new disclosure related to throughput of KMP's Natural Gas segment pipeline assets. Some interesting trends there, but the two that jumped out at us were Texas/Tejas throughput down 14% and KinderHawk throughput down 30% in 2013. This is particularly interesting given that Texas/Tejas EBDA was up 5% (+$16MM) and KinderHawk up 8% (+$13MM) in 2013 (2013 10-K, pg. 59). Significant volumedeclines coupled with increased profitability is likely a function of automatic volume/price step-ups in contracts and/or cost cuts - and likely means that EBDA will drop hard when contracts start to roll off. We believe that this will happen in a big way at KinderHawk, KMP's Haynesville Shale gathering asset, with BHP Billiton as the anchor producer.

BHP Billiton's minimum volume commitment to KinderHawk expires at the end of May 2015 (2013 10-K, pg. 15), at which time EBDA will likely fall hard. In 2013 KinderHawk throughput was only 668 MMcf/d, 34% below the 2014 minimum volume commitment of 1,010 MMcf/d. BHP Billiton is directing the majority of its US oil and gas CapEx to its Eagle Ford and Permian assets, so we expect that its Haynesville production will continue to decline.

BHP Billiton discloses enough information regarding the KinderHawk agreement for us to confidently forecast KinderHawks's future EBDA (from BHP's 2/18/14 6-K):

Assuming that KinderHawk throughput continues to decline ~5-10% per year through 2016 (versus down 30% in 2013!), and that the gathering + treating rate ($/Mcf) stays flat (this is likely optimistic given the excess capacity), we estimate that KinderHawk's EBDA will decline $74MM YoY in 2015 and another $45MM YoY in 2016. Said another way, this asset will generate $211MM of EBDA in 2014 and $92MM of EBDA in 2016, a $119MM hit to DCF.

Organic cash flow declines like this are particularly negative for KMP because it has razor-thin distribution coverage, and its maintenance CapEx definition has nothing to do with keeping cash flows that, such that it will take ~$1B of externally-financed "expansion" CapEx (which is 27% of the 2014 budget) just to replace these cash flows. In other words, more dilution at KMP.

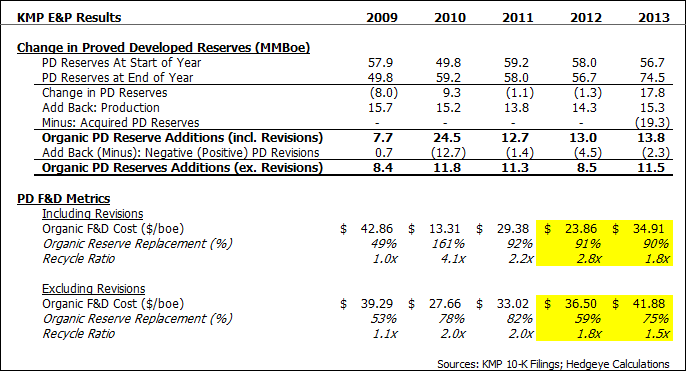

2. E&P Results Were Weak in 2013......KMP management says that its E&P segment had a strong year in 2013, while the data in the back of the 10-K tells a different story. The marginal production "beat" is not impressive considering that E&P capital costs incurred came in at $767MM (including the $285MM Goldsmith acquisition), more than double the 2013 guidance of $367MM.

Further, open EBITDA (i.e. EBITDA before the impact of commodity derivatives) increased only $10MM YoY in 2013 despite open revenues up $144MM. Production costs (excluding expensed CO2) jumped to $22.48/boe, up 41% from $15.93/boe in 2012. As a result, KMP's E&P open EBITDA margin fell to 69% ($63.26/boe) in 2013 from 76% ($66.93/boe) in 2012.

On the capital side, the key metric is the Organic Proved Developed Finding and Development (F&D) Cost. This is where the rubber meets the road - turning capital into production (not PUD reserves). In 2013, KMP had organic costs incurred of $482MM and added 13.8MMboe of PD reserves including revisions, for an F&D cost of $34.91/boe; this was +46% from $23.86/boe in 2012. KMP replaced only 90% of production with organic PD reserve additions in 2013, versus 91% in 2012, suggesting that its organic CapEx budget is not enough to maintain PD reserves. KMP's recycle ratio (EBITDA/boe over F&D/boe) was 1.8x in 2013, down from 2.8x in 2012. Excluding PD revisions, KMP's 2013 F&D cost was $41.88/boe, +15% from $36.50/boe in 2012. Reserve replacement was 75%, up from 59% in 2012; and KMP's recycle ratio was 1.5x, down from 1.8x in 2012. All-in-all, KMP's E&P capital efficiency deteriorated significantly in 2013.

---

KMP produced 13.8MM boe in 2013. In our view, proper maintenance CapEx is the cost of keeping production flat, or replacing produced reserves. With a PD F&D Cost (ex. revisions) of $41.88/boe, it would cost KMP~$578MM per year to keep production flat with the 2013 level. This is in-line with KMP's YE13 Future Development Cost per PUD reserve of $40.89/boe, which was up from $31.12/boe at YE12.

---

While KMP's production increased 7% YoY to 41,922 boe/d, organic growth was only 3%. Further, production remains below what it was in 2009, 43,103 boe/d. Over the last 5 years KMP has spent $2.1B of capital for no production growth, with near $0 assigned to maintenance CapEx. Given the 50/50 IDR split, that's a +$1B wealth transfer from the LPs to the GP, just since 2009.

---

KMP's all-in costs (cash costs + F&D) are now ~$65-$70/boe, making it one of the highest cost oil producers in North America. With the WTI curve steeply backwardated, expect margins and returns to come under more pressure unless KMP can get its expenses and capital costs lower.

---

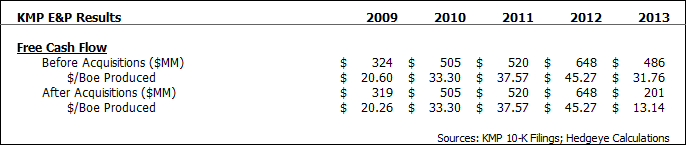

KMP's E&P Free Cash Flow (open EBITDA - CapEx) came in at the lowest level since 2009, $486MM before acquisitions and $201MM after acquisitions. This compares to $648MM of E&P Free Cash Flow in 2012.

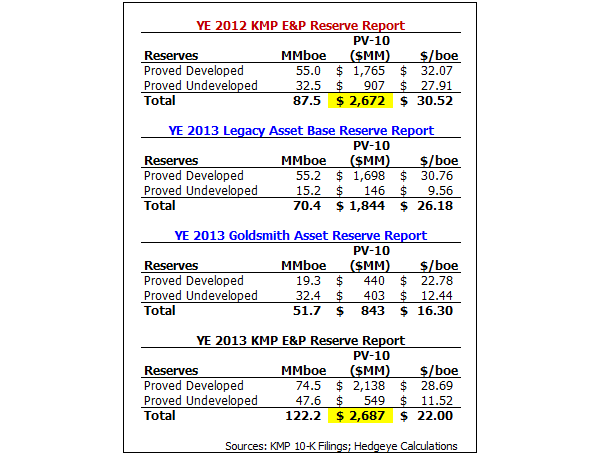

3. KMP's Goldsmith PV-10 begs further questions......KMP disclosed that the 12/31/13 PV-10 of the Goldsmith Unit was $843MM; this is 3x what KMP paid for it in June 2013, $285MM. This is highly questionable, in our view, and suggests to us that there is considerable risk to KMP hitting the Goldsmith production forecast in its PV-10 and long-term budget. The seller, Legado Resources, worked this asset since 2008 and had ROZ plans as KMP does, as this article demonstrates; Legado was not an uninformed seller. It appears to us that Legado would have valued the PUD reserves that KMP is assigning the Goldsmith Unit (32.4MMboe) near $0, while the KMP PV-10 of the PUDs is $403MM. The reserve report warns us about these PUD reserves (our emphasis):

"It should be noted that proved undeveloped reserves for a CO2 flood in the Goldsmith Landreth Unit (Goldsmith Field) account for 63 percent of the reserves included herein. These reserves were based on volumetric oil-in-place volumes for both the Main Pay and Residual Oil Zone intervals for this project estimated and provided by Kinder Morgan and reviewed by Ryder Scott. Nearby pilots or similar established improved recovery CO2 projects in the Permian Basin area in which the Goldsmith Field is located, were used to determine the appropriate recovery of the oil-in-place volumes" (Ryder Scott, Exhibit 99.2, KMP 2013 10-K).

Curiously, KMP's PV-10 was flat YoY at $2.7B despite the Goldsmith acquisition. The PV-10 of the legacy asset base declined by ~$800MM YoY, largely due to negative PUD revisions at the Katz field and an increase in overall future development costs, while the Goldsmith acquisition added ~$800MM of PV-10. A few questions on our mind: Did KMP acquire and then write-up the Goldsmith Unit PV-10 to ~$800MM in order to compensate for the underperformance of legacy assets? How much credence should we put in KMP's Goldsmith Unit production forecast given the recent issues at Katz that led to negative PUD reserve revisions this year, as well as the wide bid-ask between the acquisition price and KMP’s PV-10? And lastly, why shouldn’t the $285MM spent on the Goldsmith acquisition be considered sustaining CapEx?

Lastly, we note that Goldsmith production as of 12/31/13 was 1,230 bbl/d, down from the 2H13 average of 1,300 bbl/d (2013 10-K, pgs. 8 and 20).

4. New Sustaining CapEx definition and added disclosure......In the 2013 10-K, KMP made a subtle change in its definition of sustaining CapEx and added more disclosure, in what looks to us like an attempt to more closely match the language used in SEC filings to the language in KMP’s partnership agreement.

From the 3Q13 10-Q (pg. 68) and 2012 10-K (pg. 73): "We define sustaining capital expenditures as capital expenditures which do not increase the capacity of an asset."

From the 2013 10-K (pg. 74, our emphasis):

“We account for our capital expenditures in accordance with GAAP. Capital expenditures under our partnership agreement include those that are maintenance/sustaining capital expenditures and those that are capital additions and improvements (which we refer to as expansion or discretionary capital expenditures). These distinctions are used when determining cash from operations pursuant to the partnership agreement (which is distinct from GAAP cash flows from operating activities). Capital additions and improvements are those expenditures which increase throughput or capacity from that which existed immediately prior to the addition or improvement, and are not deducted in calculating cash from operations. Maintenance capital expenditures are those which maintain throughput or capacity. Thus under our partnership agreement, the distinction between maintenance capital expenditures and capital additions and improvements is a physical determination rather than an economic one.

Generally, the determination of whether a capital expenditure is classified as maintenance or as capital additions and improvements is made on a project level. The classification of capital expenditures as capital additions and improvements or as maintenance capital expenditures under our partnership agreement is left to the good faith determination of the general partner, which is deemed conclusive.”

A few points on this….

- KMP added “throughput or” to the maintenance CapEx definition. This is great.... So which is it, throughput or capacity? Because they can be very different. Think of a gathering system – if it’s “throughput,” then new well connections needed to hold volumes flat would be included in maintenance CapEx; if it’s “capacity,” then new well connections would not be included in maintenance CapEx. There's a lot of discretion here.

- “The distinction…is a physical determination rather than an economic one” = maintenance CapEx has no relation to income, cash flows, etc.

- “…the determination…is made on a project level” = KMP will not reserve for CapEx for one project that may be needed to replace organic cash flow declines on another (think KinderHawk).

- “…the determination…is made on a project level” = What constitutes “a project”? Is a single oil well “a project”? Again, there's a lot of discretion here.

- “…which is deemed conclusive” = What the GP says, goes.

5. On KMP's rate cases and potential refunds......At the FERC, both SFPP and EPNG are subject to rate cases (2013 10-K, pgs. 159-60). In the SFPP case, the shippers are requesting $100MM in refunds and a ~$20MM reduction in annual rates. EPNG is also subject to a FERC rate case; the potential refunds and rate reductions were not disclosed, though KMP noted that a refund will likely be less than $50MM in the 3Q13 10-Q (pg. 32).

SFPP is subject to a separate rate case at the CPUC (2013 10-K, page 160). The shippers are requesting refunds of $400MM and annual rate reductions of $30MM. KMP expects a decision in 2Q14.

It is comical that KMP discloses, "we do not expect any reparations that we would pay in [these] matter[s] to impact the per unit cash distributions we expect to pay to our limited partners for 2014" (2013 10-K, pg. 160). As if this matters – the distribution payment is purely discretionary. But these rate cases could result in at least a $50MM reduction in annual DCF, as well as a $500MM refund payment that will be financed 100% by KMP unitholders.

---

KMP's net regulatory asset/liability moved from a $201MM asset as of 12/31/12 to a $64MM liability as of 12/31/13, largely due to this:

"During the second quarter of 2013, we began applying regulatory accounting to the Trans Mountain pipeline systems due to a newly negotiated long-term tolling agreement approved by the system’s regulator that went into effect in April 2013. The primary impact of applying regulatory accounting was the reclassification of approximately $362 million of current and long-term deferred credits to regulatory liabilities. We expect this regulatory liability to be refunded to rate-payers over approximately the next four years" (2013 10-K, page 120).

It's not clear to us how KMP will account for these revenues and expenses as they run through the non-GAAP financials. Will the $362MM of refunds to be paid over the next 4 years be "Certain Items"?

6. Other key quotes, comments, and questions from the 10-K……

- How much of the $504MM Northeast Upgrade expansion project was really maintenance CapEx? The project’s scope included, “system upgrades at four existing compressor stations and one meter upgrade in New Jersey” (pg. 7).

- Texas Intrastate relies on new well connections to keep throughput flat, though that CapEx is likely not considered maintenance: “While our intrastate group does not produce gas, it does maintain an active well connection program in order to offset natural declines in production along its system and to secure supplies for additional demand in its market area” (pg. 14).

- Midcontent Express’s long-term contracts begin to expire in August 2014: “Capacity on the Midcontinent Express system is 99% contracted under long-term firm service agreements that expire between August 2014 and 2020” (pg. 19).

- Qualifying language regarding the St. John’s CO2 project suggests caution: “As of the date of this report, we are continuing to perform predevelopment activity and test wells; however…” (pg. 21).

- The completion date of Trans Mountain has shifted back slightly, from “late 2017” to the “end of 2017” (pg. 26).

- We note the lack of organic volume growth in the entire Natural Gas Segment (pg. 58), CO2 and oil production (pg. 61), and bulk transload tonnage (pg. 66).

- G&A “Certain Items” totaled $75MM in 2013, with the majority of the expense related to acquisition costs (pg. 70-71); KMP is in business of making acquisitions – these should not be Certain Items, in our view.

- Management’s quantitative financial performance objectives – which, in part, determine their bonuses – are based only on what KMI, KMP, and EPB pay out in dividends / distributions (pg. 88-89). This is ridiculous, as distribution payments are discretionary – management can set the distribution at whatever price it wants.

- Despite the fact that management wants us to believe that DD&A is irrelevant, “When assets are put into service, we make estimates with respect to useful lives (and salvage values where appropriate) that we believe are reasonable. However, subsequent events could cause us to change our estimates, thus impacting the future calculation of depreciation and amortization expense. Historically, adjustments to useful lives have not had a material impact on our aggregate depreciation levels from year to year”(pg. 116).

- The APT/SCT Jones Act Tanker acquisition became effective on 1/17/14 (pg. 124), yet KMP/KMI still left out its impact on the 2014 budget that is put out at the 1/29/14 Analyst Day.

- The average ATM financing price in 2013 was $83.22/unit (pg. 138).

- KMP’s legal reserve increased $207MM YoY to $611MM as of 12/31/13 (pg. 162).

- KMP discloses the Slotoroff suit, and of course, “Defendants believe that this suit is without merit and intend to defend it vigorously” (pgs. 162-63).

Kevin Kaiser

Managing Director