TODAY’S S&P 500 SET-UP – February 19, 2014

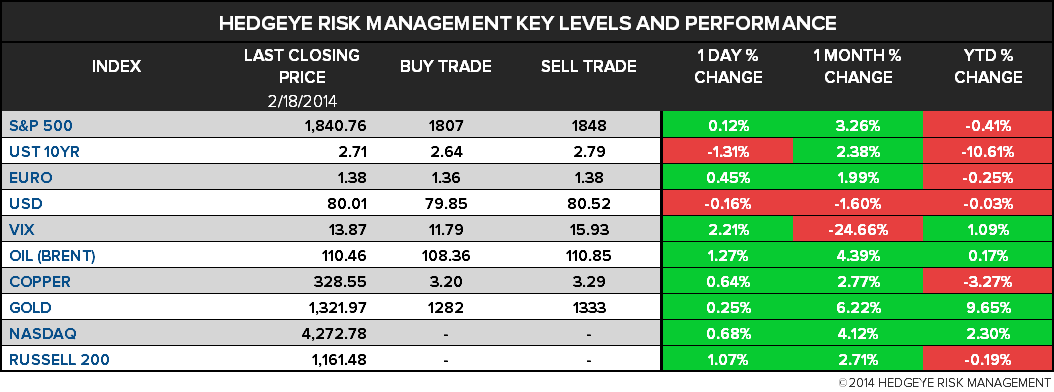

As we look at today's setup for the S&P 500, the range is 41 points or 1.83% downside to 1807 and 0.39% upside to 1848.

SECTOR PERFORMANCE

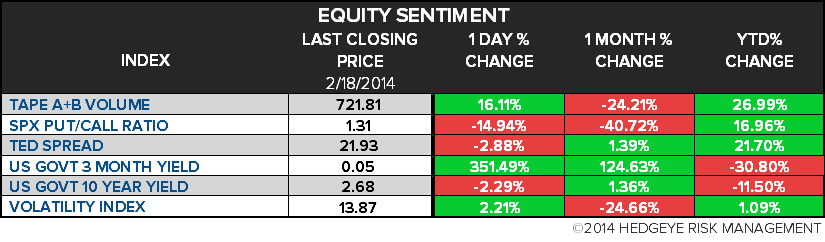

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.39 from 2.41

- VIX closed at 13.87 1 day percent change of 2.21%

MACRO DATA POINTS (Bloomberg Estimates):

• 7am: MBA Mortgage Applications, Feb. 14, est. -2.0%

• 7:45/8:55am: ICSC/Redbook weekly retail sales

• 8:30am: Bureau of Labor Statistics issues redesigned PPI

• 8:30am: Housing Starts, Jan., est. 950k (prior 999k)

• 11am: Fed to purchase $1b-$1.25b in 2036-2044 sector

• 11:30am: U.S. to sell $32b 4W bills

• 12:15pm: Fed’s Lockhart speaks on economy in Macon, Ga.

• 1pm: Fed’s Bullard speaks in Washington

• 2pm: Fed releases minutes from Jan. 28-29 FOMC Meeting

• 4:30pm: API weekly oil inventories

• 7pm: Fed’s Williams speaks on economy in New York

GOVERNMENT:

- President Barack Obama holds press conf. with Canadian Prime Minister Stephen Harper, Mexican President Enrique Pena Nieto

WHAT TO WATCH:

- China cuts Treasury holdings by most since 2011 amid Fed taper

- Canadian Natural buys some assets of Devon Canada for C$3.13b

- BlackBerry CEO chides T-Mobile for promoting switch to iPhones

- Blackstone buys stake in Senator as Hill targets hedge funds

- Ranbaxy, Teva agree to settle New York antitrust drug Claims

- Las Vegas Sands says hackers breached co.’s internal drives

- EBay CEO Donahoe says PayPal is stronger as a unit

- Fed foreign-bank capital rules positive for insurers: Seiberg

- Credit Suisse waits for $11b answer in N.Y. fraud suit

- Verizon Communications to issue 1.27b shrs to Vodafone holders

- Buffett’s Coca-Cola complacency warning foretells troubled year

- Mexico to push ahead on broadcast-TV rules after legal decision

- Tribune sees $325m benefit in public publishing co.: L.A. Times

- Netflix says Jan. speed dropped 14% on Verizon’s FIOS: WSJ

- Investment Technology Group may buy Nyfix From ICE: WSJ

AM EARNS:

- Cimarex Energy (XEC) 6am, $1.41

- Devon Energy (DVN) 7am, $1.08 - Preview

- Eaton Vance (EV) 8:35am, $0.59

- Garmin (GRMN) 7am, $0.62

- Health Care REIT (HCN) 7:30am, $0.16

- Hecla Mining (HL) 8am, $0.00

- Host Hotels & Resorts (HST) 6am, $0.31

- Lumber Liquidators (LL) 7am, $0.72

- Medicines Co (MDCO) 7am, $0.12

- MGM Resorts Intl (MGM) 8am, $(0.01)

- Navios Maritime (NM) 7:45am, $(0.09)

- Omnicare (OCR) 7am, $0.90

- Sherritt Intl (S CN) 7:42am, C$0.01 - Preview

- Six Flags Entertainment (SIX) 8am, $(0.22)

- SunEdison (SUNE) 6am, $0.17

- Wabtec (WAB) 8:10am, $0.79

PM EARNS:

- Allegion (ALLE) 5pm, $0.59

- Arris Group (ARRS) 4pm, $0.46

- Avis Budget Group (CAR) 4:15pm, $0.12

- Coeur Mining (CDE) 5pm, $(0.18)

- Concho Resources (CXO) 4:30pm, $0.95

- Energy Transfer Equity (ETE) 5:10pm, $0.32

- Energy Transfer Partners (ETP) 5:05pm, $0.58

- Equinix (EQIX) 4:01pm, $0.79

- Finning Intl (FTT CN) 4:30pm, C$0.54

- Goodrich Petroleum (GDP) 4:44pm, $(0.47)

- HealthSouth (HLS) 4:15pm, $0.42

- Helix Energy Solutions (HLX) 5:30pm, $0.32

- HomeAway (AWAY) 4pm, $0.13

- HudBay Minerals (HBM CN) 5:09pm, C$0.02 - Preview

- Iamgold (IMG CN) 5:04pm, $0.04

- Jack in the Box (JACK) 4:01pm, $0.66

- LifeLock (LOCK) 4:05pm, $0.21

- Marriott (MAR) 4:30pm, $0.49

- Millennial Media (MM) 4:05pm, $(0.01)

- Penn Virginia (PVA) 4:03pm, $(0.03)

- Questar (STR) 4:10pm, $0.37

- Safeway (SWY) 4:05pm, $0.48 - Preview

- Sunoco Logistics Partners (SXL) 4:02pm, $0.65

- Synopsys (SNPS) 4:05pm, $0.52

- Tesla Motors (TSLA) 4:01pm, $0.26 - Preview

- Trinity Industries (TRN) 4:01pm, $1.42

- Williams (WMB) 4:05pm, $0.21

- Williams Partners (WPZ) 4:05pm, $0.40

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Mercuria Said in Discussions With China’s SDIC to Sell Stake

- WTI Oil Rises for Second Day as U.S. Chill Erodes Fuel Supplies

- Sugar Crop Tumbling to Four-Year Low in India May Cut World Glut

- Nickel Reaches Three-Week High on Buying to Close Bearish Bets

- Gold Holds Below 3-Month High as Buying Slows Before Fed Minutes

- Soybeans Near Two-Month High on U.S. Exports, Brazil Drought

- Sugar, Coffee Decline After Rally on Brazil Dryness; Cocoa Falls

- Rebar in Shanghai Advances on Spring Restocking Speculation

- Commodities Revenue at Top 10 Banks Declined 18% Last Year

- Rice Rout Seen Extending as Thai Sales Quicken: Southeast Asia

- Arabica Coffee Climbs 2.8% in New York, Erasing Earlier Decline

- EU Gas to Extend Bear Market on Mildest Month Since ’08: Energy

- Australia Freight, Currency Advantage Delivers China’s Iron Ore

- Natural Gas Rises to Four-Year High as Inventories Seen Falling

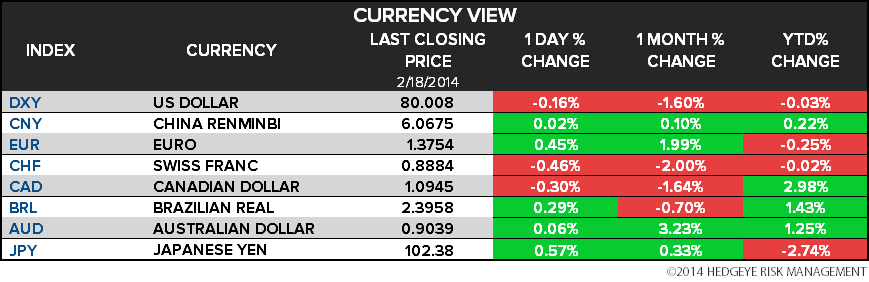

CURRENCIES

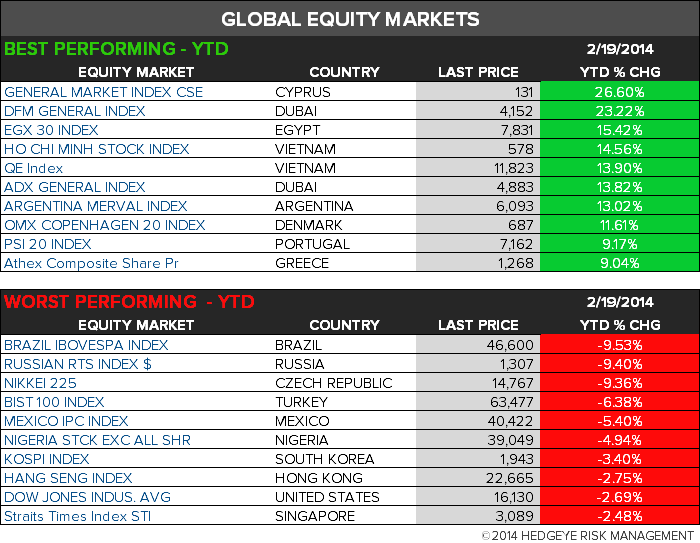

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team