Conclusion: We’re one of the few bulls on WWW, and we heard absolutely nothing that shakes our confidence in this story. We continue to believe (regardless of guidance) that WWW will print outsized revenue growth at an incremental margin nearly 2x the company average as it scales its newer brands over its superior Int’l infrastructure and de-levers along the way. We’re modeling $1.78 and $2.28 in 2014 and ’15, respectively, with ultimate earnings power of $4.18 out in 2018, which is roughly 50% above the consensus. This stock used to be expensive, with earnings catalysts. Now it’s cheap with the same catalysts. Our full thesis and model highlights are outlined below.

DETAILS

WWW’s fourth quarter print was a lot more tame than the stock price would otherwise suggest. The company beat estimates by $0.02, though admittedly it was on a weak-ish growth algorithm (revenue and EBIT both flat organically, with taxes helping). Listening to the company’s prepared remarks, it was clear to us that these guys have such a firm grasp on their portfolio. They get it. That’s such a rarity in the US retail space. Unfortunately, their guidance is perennially conservative, and few people choose to see through it. As painful as this event is, we think it sets up a series of earnings beats throughout the remainder of the year.

We think that there are a few points that are critical in contextualizing WWW’s performance this quarter, and in modeling the upcoming year.

1) Guidance: We so rarely spend so much time on guidance, but with this company, it matters. It gave better definition to FY guidance -- 3-6% top line and 10-14% EPS. Acceptable in the context of where they already came out at ICR, but below where the Street is published. That in itself was probably not enough to hit the stock. But just before the Q&A when CFO Grimes discussed that the first quarter would have down revenue and EPS, the stock lost its bid almost immediately. Are there issues around this quarter? Weather, the economy, weather -- of course there are. But this seems a bit severe to us. Either a) something has changed fundamentally, b) weather is beating the heck out of this company, or c) WWW is being overly conservative with its forecast.

As hard as we try – at least with the information we have -- we can’t find anything that leads us to think that this story has changed over the past 8-weeks. Weather is probably a bit of a factor – especially since 25% of its sales come from a summer brand like Sperry. But let’s consider guidance for a minute. Over the past 5 years, WWW has, without fail, taken a substantial whack out of guidance at the beginning of each year. And EVERY year, the company has come back and earned something higher than where guidance was in the first place. That’s evidenced in the chart below. We think this is what we’re looking at today.

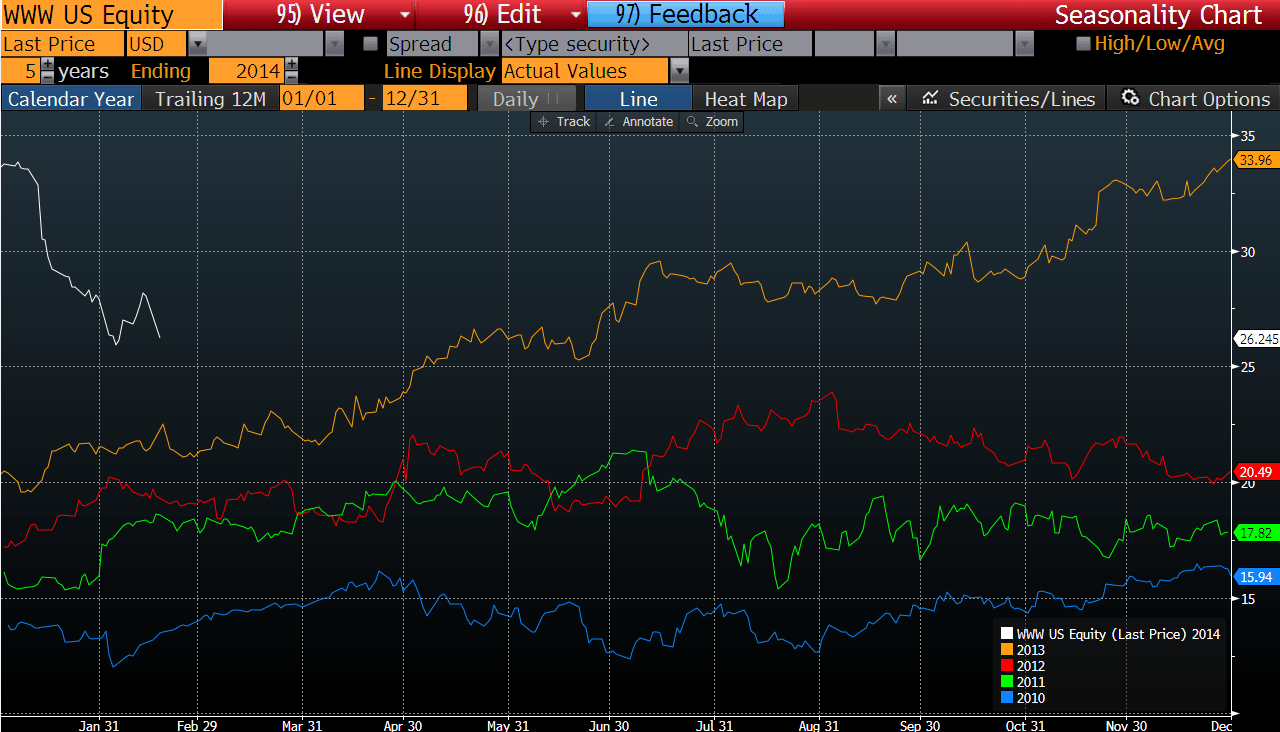

2) Seasonality: Furthermore, seasonality is counting against this story in a very big way. In every single year over the past five, you did not want to own the name at the start of the year. This one is obviously no exception. Is it because of weather, or retail trading patterns? We think NO and NO. The reality is that this is the time of year when the company gives earnings guidance. And as noted above, guidance is ALWAYS weak. As the year progresses, the Street miraculously realizes that both top line and EPS growth is far better than they initially expected (because they initially did nothing other than plug the company’s guidance into their models). The chart is a bit ugly (Bloomberg) but the patterns are very clear.

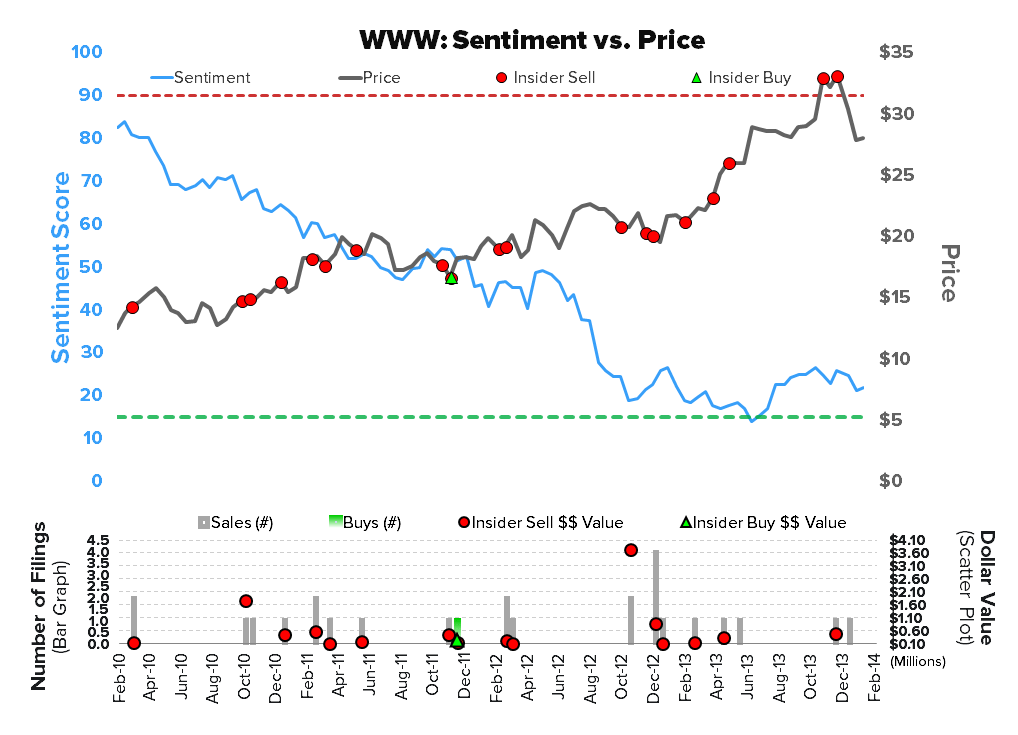

3) Sentiment. Plain and simple…sentiment stinks. When we’re faced with conservative initial guidance at the start of the year, only 1 out of 14 analysts being positive on the name, and short interest near historical highs, it’s usually not very good news over the near-term. Seriously, one of the only names that has lower sentiment scores out of the 135 retail names we track is JC Penney.

4) Why do we have higher confidence in 2014? Let’s take a step back and look at the PLG acquisition.

2012 was the year of the deal. It was big, and painful initially – no EBIT and interest from $1.2bn in debt.

2013 was the year of integration. In 1H they moved people around, repositioned the brands, and realigned management. Then in 2H the chessboard was largely set, but they had to seal the deal with an SAP implementation, which went without a hitch.

2014, in our view, is the year of revenue growth. They have four new major tools in their toolbox, and the global salesforce (the most efficient footwear operation on the planet) finally gets to sell them. They’ve been getting international distribution arrangements in place over the past year. And while they strike new ones every day, each of them is cumulative (i.e. signing three per month means that by now there are over 40). Aside from each of those arrangements getting more productive, there’s still another 150 that could be added by our estimates.

5) Double standard? OK, here’s a nitpick. But how come in the summer when Sperry is crushing it and Merrell is sucking wind, all everyone talks about is that ‘Merrell is over’. But now that Merrell has come roaring back – even without the full contribution yet from Gene McCarthy, all anyone talks about is how Sperry (a warm weather brand) is down (in what might be the worst winter on record). Yes, Sperry is important – and we think it has another $300-$400mm worth of growth ahead of it. But it’s not WWW’s biggest brand. Yes, that distinction belongs to Merrell, and even as Sperry succeeds, it will probably always be number 2.

OUR LONG TERM THESIS

This is the most global footwear company in the world (legacy WWW). It sells about 65% of its units outside the US, and has seamless and sophisticated systems (SAP) such that all distributors speak the same language. The PLG brands, which we think are better quality overall, sell only 5% overseas, and that's simply because its former owner (Collective Brands) spent capital first on Sperry, then on US Payless stores, and did not have anything left in the kitty for international distribution of PLG brands. So now WWW can scale this superior content over its existing lean/mean infrastructure. We think it will drive an incremental $2bn in revenue over 5-years and an extra 400bp of margin. In the end, we get to earnings power of about $4.30, which is 50% ahead of what management guided at its recent analyst meeting. We're the first to admit that WWW probably won't make you rich here, as it will likely take a good 4-5 years to double. We'd admittedly rather get more aggressive on a pullback. But we know people who have been waiting for a pullback for the last 50%. In the meantime you're paying a high-teens multiple for mid-20s EPS growth -- and this company has one of the best track records of anything in consumer.