This week begins the annual Consumer Analyst Group of New York (CAGNY) Conference from Boca Raton, Florida. Click here for a program of presenters this week.

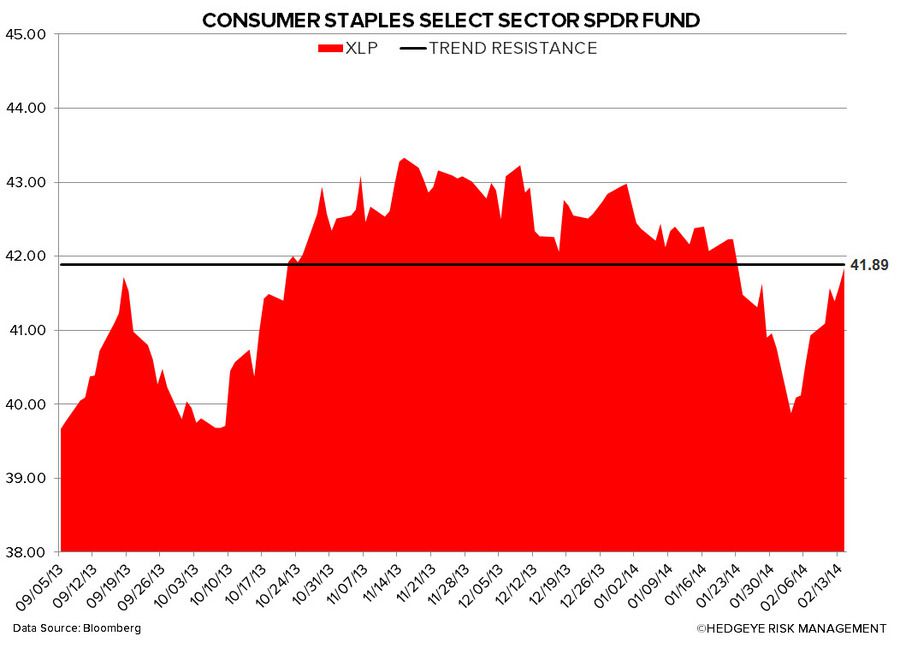

Last week the Consumer Staples (XLP) sector finished up +2.2%, broadly in line with the S&P500 at +2.3%, however, Consumer Staples is underperforming on a year-to-date basis, down -2.7% vs the S&P500 down -0.5%.

The Hedgeye U.S. Consumption Model is flashing predominantly red, as only 5 of the 12 metrics are flashing green.

From a quantitative set-up the sector remains broken across the immediate term TRADE and intermediate term TREND durations, our language for a bearish medium term sector outlook. You’ll see a similar bearish setup for most of the largest names in Consumer Staples.

We continue to believe that the sector is facing numerous headwinds, including:

- U.S. consumption growth is slowing as inflation rises, in-line with the Macro team’s 1Q14 theme of #InflationAccelerating

- The economies and currencies of the emerging market – once the sector’s greatest growth engine – remain weak with the prospect of higher inflation in 2014 eroding real growth

- The sector is loaded with a premium valuation (P/E of 18.8x)

- Less sector Yield Chasing as Fed continues its tapering program

- The high frequency Bloomberg weekly U.S. Consumer Comfort Index has not seen any real improvement over the past 6 months despite a mild increase week-over-week

Top 5 Week-over-Week Divergent Performances:

Negative Divergence: BNNY -11.8%; LO -3.1%; PEP -2.7%; DF -2.7%

Positive Divergence: THS +12.8%; SAM +8.2%; FLO +6.9%; CPB +6.7%; IFF +5.6%

The “Newsy” News Flow:

Nestle Shedding Some of L’Oreal – last week L’Oreal, the world’s largest cosmetics maker, agreed to buy back 8% of its stock from Nestle, through a cash payment of €3.4 billion for 27.3 million shares and in exchange for half of its Galderma skincare JV for a further 21.2 million shares.

TreeHouse Foods Sues Green Mountain Coffee and Keurig on Anticompetitive Conduct - last week THS charged GMCR and Keurig over anticompetitive acts to maintain a monopoly over the cups used in single-serve brewers. As the WSJ specifically points out: Green Mountain has announced that its Keurig 2.0 brewer, to be launched later this year, will contain an anticompetitive lock-out technology that will prevent the Keurig 2.0 brewers from functioning with cups supplied by unlicensed competitors. TreeHouse asserts that these actions are an attempt to eliminate consumer choice and to coerce Keurig 2.0 brewer owners into purchasing only Green Mountain owned or licensed K-cups. In addition, Green Mountain has announced plans to eliminate the current lineup of K-cup brewers, which function with competitive cups, to exclude competition and force consumers to purchase higher-priced Green Mountain cups. TreeHouse's lawsuit maintains that any supposed consumer benefits from the new technology are more than outweighed by the harm to competition and consumers by eliminating their choice and forcing them to pay higher prices for Green Mountain cups.

Last Week’s Research Notes

- BNNY – Stock Hammered on Input Cost Inflation. Buy it?

- RAI—Balancing Profitability and Market Share On Weak Cig Volume

- LO Bulls—Volumes Miss But Outperforming the Industry

Earnings Calls This Week (in EST):

Monday (2/17): Presidents’ Day

Tuesday (2/18): KO 9:30am

Wednesday (2/19): HLF 11am

Thursday (2/20): HRL 9am; NUS (TBD)

Friday (2/21): -

Quantitative Setup

In the chart below we look at the largest companies by market cap in the Consumer Staples space from both a quantitative perspective and fundamental aspect where we can offer one. As you will see over time, sometimes our fundamental view does not align with the quantitative setup (though not often).

Alcohol

BUD – big beta bounce last week (on much lower-volume signals than we saw for the stock on the way down in the weeks prior), but still bearish TREND = 102.93 resistance

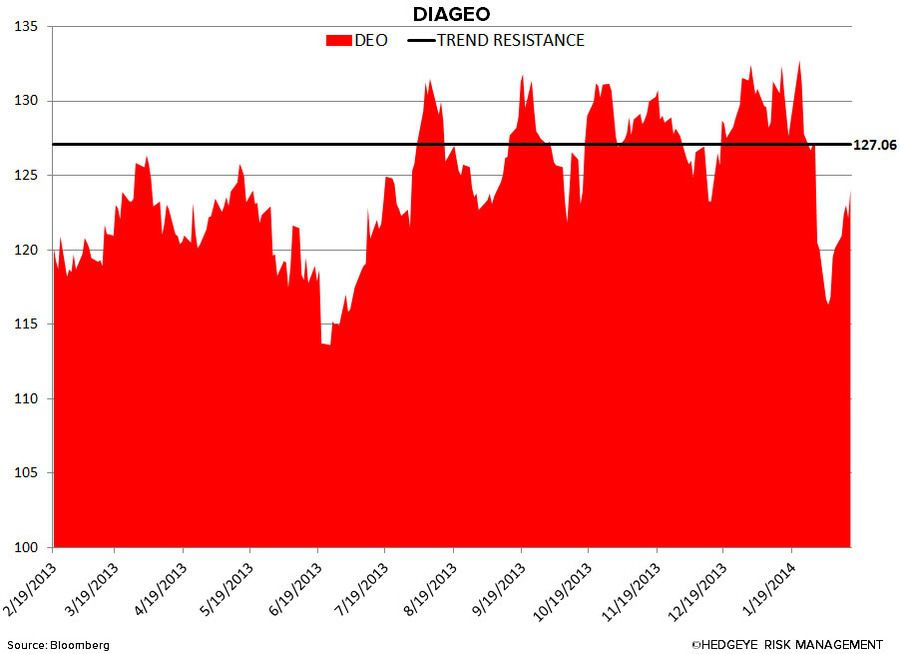

DEO – same quantitative setup as BUD; big v-bottom bounce on decelerating volume signals (that’s bearish) with TREND resistance intact overhead = $127.06

Beverage

KO – looks the same as BUD and DEO; beta bounce on unconvincing volume signals last week – would have to recapture TREND line of $39.97 to change the bearish view

PEP – this chart is what BUD, DEO, and KO can look like again, in a hurry – no volume on the bounce to lower-highs, then wham! Straight back down on big time volume; TREND resistance intact = $81.99

Food

GIS – doesn’t look nearly as bad as the beverage names; TREND resistance recaptured last week (now its support at $48.79)

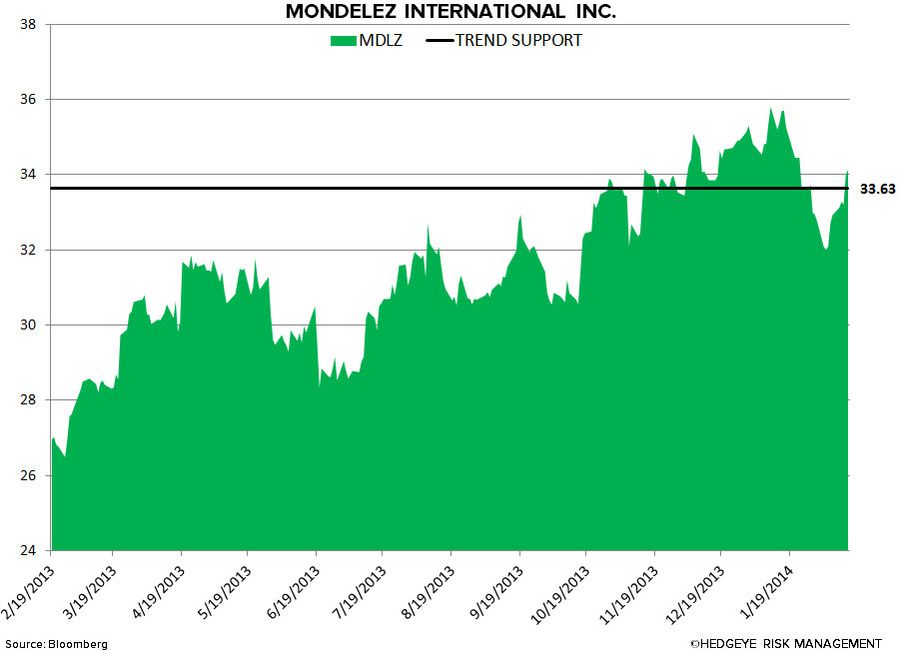

MDLZ – bounce on a better than bad volume signal last week recaptures TREND support of $33.63

Household Products

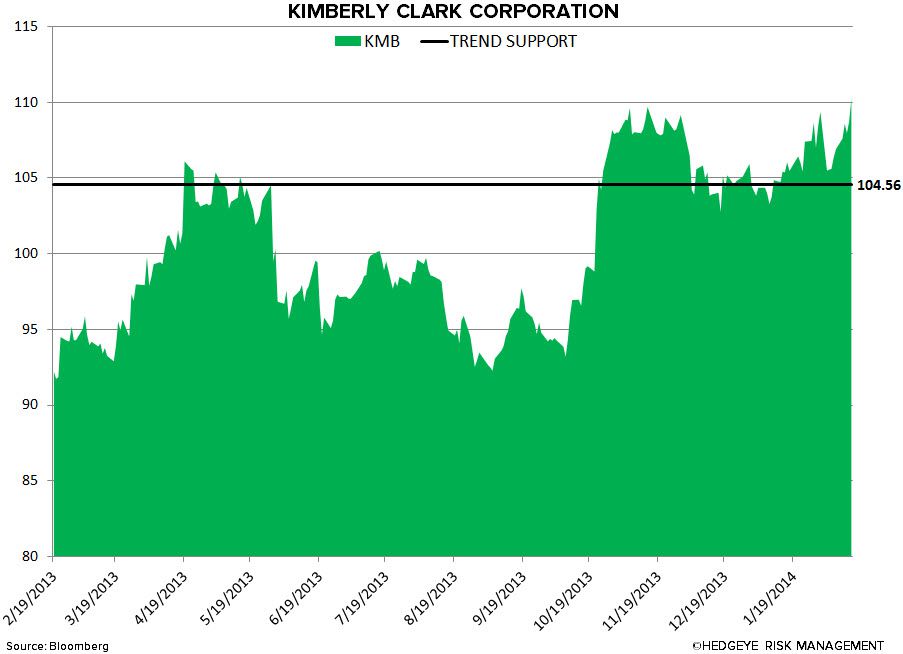

KMB – higher-highs last week on low-volume, but this Kimberly Clark remains the best looking name on this list (TREND support = $104.56)

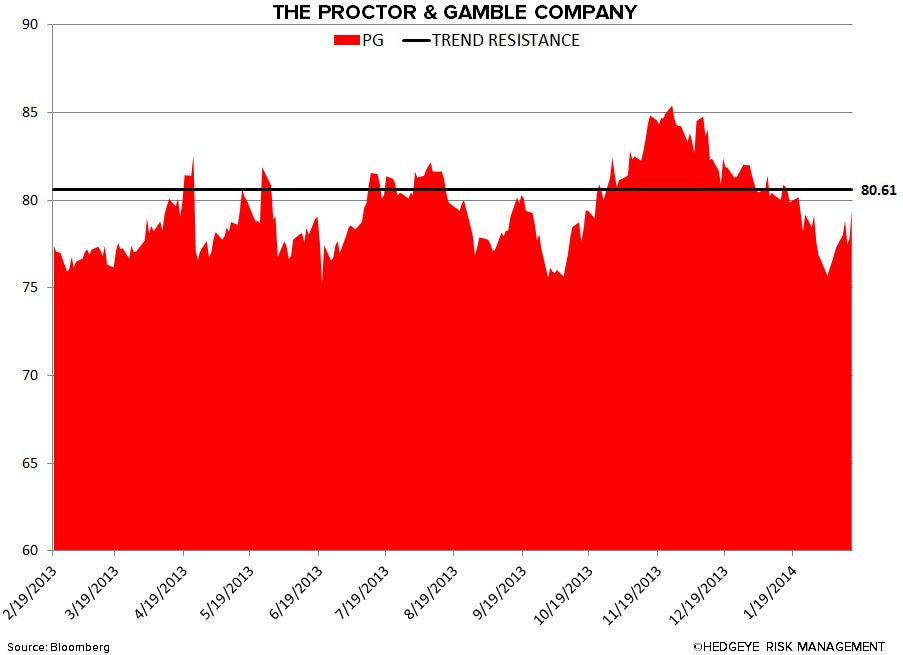

PG – guides down on Venezuela – funny, but the chart isn’t; bearish TREND remains intact at $80.61

Tobacco

MO – v-bottom beta bounce on no volume; bearish TREND resistance remains intact for the dog breath chart up at $36.43

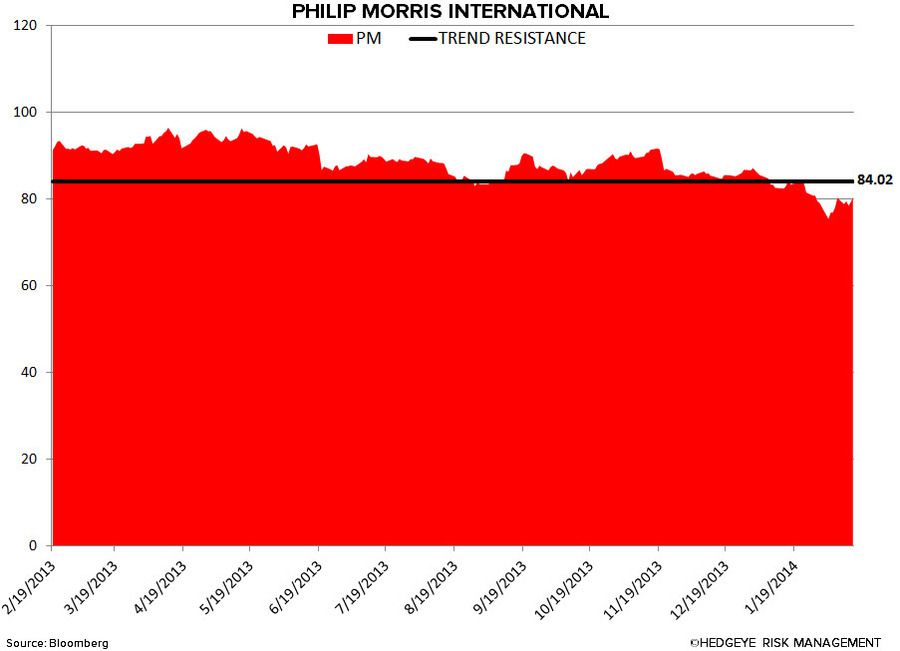

PM – same smelly dog-breath situation as MO; bearish TREND resistance firmly intact overhead at $84.02

Matt Hedrick

Food, Beverage, Tobacco, and Alcohol

Howard Penney

Household Products

(o)