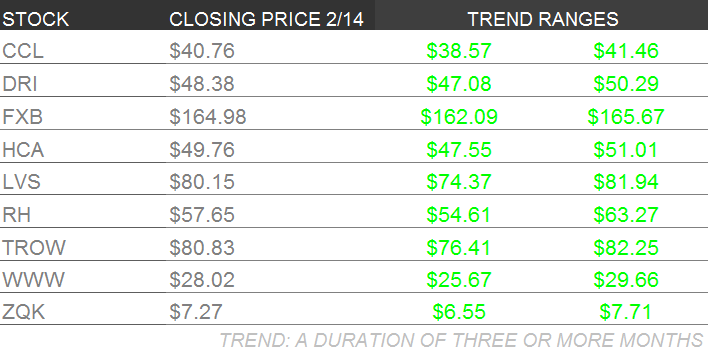

Please see below Hedgeye analysts' latest updates on our high-conviction stock ideas and CEO Keith McCullough's updated levels for each stock.

At the conclusion of this week's edition of Investing Ideas, we feature three institutional research pieces we believe offer valuable insight into the markets.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

CCL – Shares of Carnival are up 13.6% since it was added to Investing Ideas versus a 2.4% return for the S&P 500. Investors will be keeping a close eye on Norwegian’s (NCLH) earnings next Tuesday to see if there’s any indication of a price war in the Caribbean. CCL has the easiest comps among the big 3 operators, so even if discounting picks up, CCL has the most cushion. We remain bullish on CCL.

DRI – Earlier in the week, activist investor Starboard Value expressed its intent to “hold the board accountable for its actions” if the company decides to follow through with its plan to spin-off, or sell, the struggling Red Lobster chain. Darden has plans to act upon this plan before the company’s annual meeting at the end of March and if they do, Starboard plans to assume control of the company through a shareholder vote.

Red Lobster has significant real estate value that Starboard argues would be lost if the company were to divest the brand. Managing Director Howard Penney sides with Starboard, citing Darden’s real estate value as one of the many features that makes this company so valuable. All told, the activist pressure continues to build.

We continue to like Darden as a long-term investment and believe the company has the potential to create substantial shareholder value with the right management team in place.

FXB – Hedgeye remains bullish on the British Pound versus the US Dollar (etf FXB), a position supported over the intermediate term TREND by prudent management of interest rate policy from the Bank of England (BOE). We received updated economic and monetary policy guidance this week from the BOE’s Quarterly Inflation Report. 2014 GDP was revised higher to 3.4% from 2.8% previously forecast and the unemployment rate is expected to reach the 7% threshold target in January. In response, this week BOE governor Mark Carney amended his “forward guidance” to increase rates at the 7% unemployment level to signal that the Bank is not yet ready to hike rates despite the improvements seen in the economy and unemployment level.

The GBP/USD acted favorably to the news, up +1.83% week-over-week.

HCA – There is clearly a lot going on these days with hospitals. Earlier this week, reports from Health and Human Services indicated a million people had signed up for Obamacare last month, a huge number. Unfortunately, in a separate report, only a fraction of those who enrolled in the previous months paid their first bill, which means after going through the hassle to fill out the forms, they did not actually get health insurance.

We received the latest update of our doc survey this week. The big finding, and negative for our HCA position, was a huge drop in patient visits for patients with private insurance. If it persists through the quarter AND the balance of our other inputs such as orthopedic case volume and Obamacare enrollment, will probably get us to close the HCA long. But we will run the survey two more times before getting to that point. We are monitoring this closely.

LVS – Chinese New Year off to a rocking start in Macau. Through February 9, daily table revenues averaged $1.464 billion up 78% over comparable period last year. The more appropriate comp is the 3rd week of February last year when table revs averaged HK$1.107 billion – so peak CNY is up about 32%. While it’s still early, Las Vegas Sands is the market share leader at 25.3% thanks to its success in the mass business. We expect another strong week of revenues as VIP high rollers start rolling into town. For the month of February, we expect revenue growth to exceed 20%.

RH – We hosted a conference call with our Institutional subscribers earlier this week to address issues facing Restoration Hardware over the 3 durations that we typically look at when making investment decisions. Those of course are Trade (3 weeks or less), Trend (3 months or more), & Tail (3 years or less). RH is still our favorite long in the retail space by a long shot. Here is a quick summary of the points we addressed as it relates to the Trade duration.

During the retail meltdown during December and January – RH was hit far worse than the rest of the retail sector. We’d argue that silence hurt the company more than anything. In our opinion, the market is severely overestimating the impact that the competitive retail environment and cold weather will have on RH. Remember, nearly 50% of RH sales come from the dot-com channel. We are going to have to wait to hear the company’s 4Q numbers – likely until late March, but we think that the company will report numbers in line with their previous guidance, which calls for revenue growth in the mid-to-low 20’s and earnings growth in the high-20’s to low-30’s range.

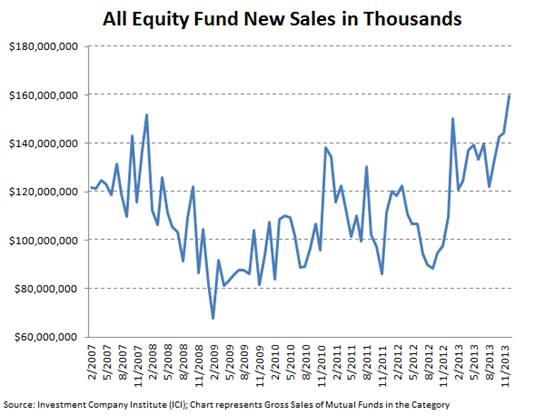

TROW – The historical relationship of lagged retail mutual fund flow to performance continues to hold into the first part of 2014 with equity mutual fund flow continuing to be positive despite a negative start to the year for U.S. stocks. Our research shows that over a 12 year period, fund flow has trailed performance by an average of 6 months which means that the +30% return in the S&P 500 in 2013 can create continued stock fund inflow through the first half of 2014 (barring any major change to the trajectory of stocks).

While most fund flow surveys focus on net flows (which is new fund sales less fund redemptions) a snap shot of solely mutual fund sales shows the strength in stocks and the continued weakness in bonds. Through December of last year, all stock fund sales are breaking to new highs which means that demand from retail investors continues to increase.

Conversely, all bond fund sales continue to trend lower from their all time highs in early 2013, in an indication of decreasing demand from retail investors. T Rowe Price is well positioned to benefit from this environment as a leading stock fund manager with 85% of its assets in equities. TROW also has de minimus exposure to emerging markets which could be a real negative theme for 2014 and beyond.

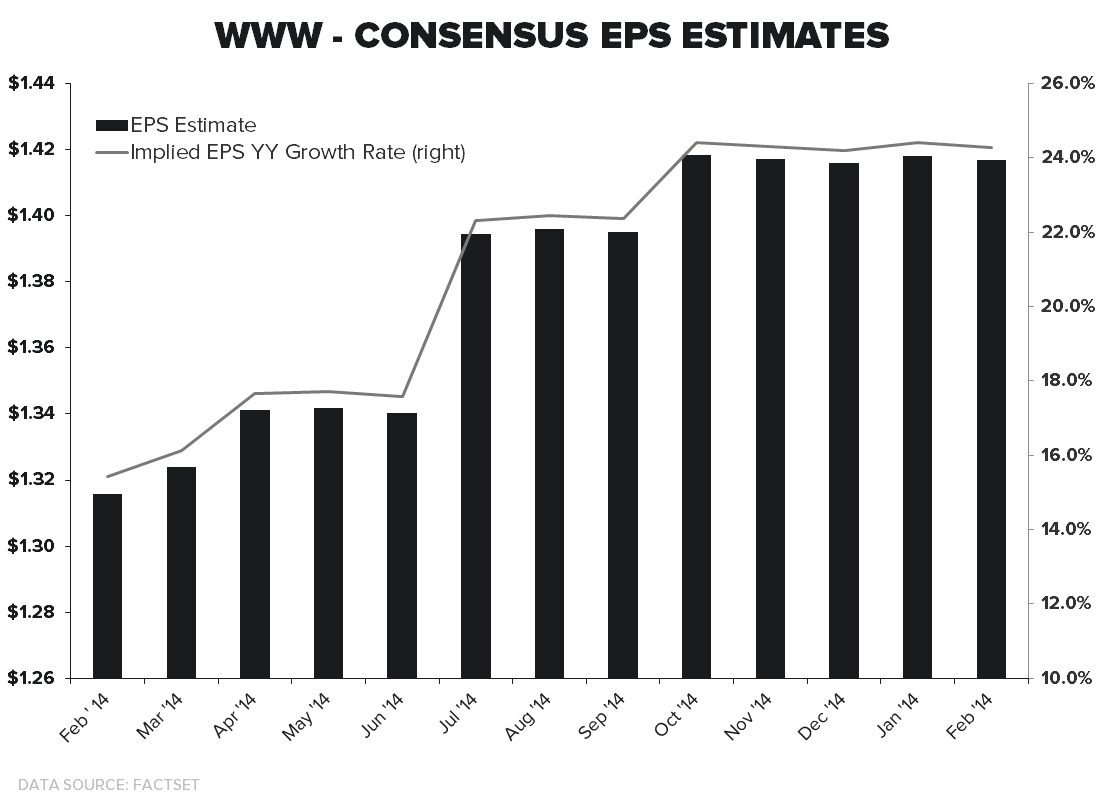

WWW – Wolverine Worldwide reports its 4Q Earnings on Tuesday (2/17). While we don’t expect any fireworks on the call due to the company’s preannouncement in early January - we do like WWW going into the print and think that it will print upside to earnings. One thing that we will be looking for on the call is an update on the company’s new international partnership agreements for the recently acquired PLG brands. Other than that, everything has been pretty much spelled out in the company’s press release and at its presentation at the ICR conference.

The company already gave preliminary guidance for FY14 and it called for “mid-single digit” revenue growth and “solid double-digit” earnings growth. One thing to keep in mind is that WWW may be the best company in retail at managing the Street’s expectations. In the chart above you can see the change in consensus’ ’13 EPS estimates since the company reported earnings in February of 2013. Originally the Street was looking for 15% earnings growth. That number has inched its way up to where it currently sits at 25%. We expect more of the same in ’14.

Consensus is seriously underestimating the top line growth potential for the acquired PLG brands in the international marketplace. We continue to see upside potential in these markets and expect to see continued strength in WWW’s core brands.

ZQK – The key callout for ZQK comes from Friday’s less-than-stellar VF Corp results. VFC management noted that the #1 use of cash is for acquiring other businesses. Of course, that is only intensified during times like this when organic growth is tough to find, like they’re faced with today. Management noted quite clearly that debt-to-capital is 19%, lower today than when they bought Timberland. In other words -- 'we can buy something big'. We still think that VFC will ultimately own ZQK. The only catch is that VFC is not good at buying things that are broken. And ZQK -- though there is an exceptional plan in place to fix the company -- is broken. Our sense is that VFC will have a greater appetite for buying ZQK when at $12 once it starts growing again, than at $7 when its' top line is struggling. But it's a matter of time, in our opinion.

* * * * * * * * * *

Click on the title below to unlock the institutional note.

Why Is Gold (and Gold Miners) Ripping?

We’ve been calling for investors to get longer of inflation-oriented assets in lieu of consumption-oriented assets, at the margins, as it becomes increasingly likely the Fed stops tapering (or incrementally eases) over the intermediate term.

The Cheesecake Factory (CAKE) remains on the Hedgeye Best Ideas list as a SHORT. The company delivered disappointing 4Q results earlier this week. When in doubt, blame the weather!

ICI Fund Flow Survey: Record Divergence In ETFs...Mutual Funds Carry On

An historic week within ETFs with record outflows in equities and record inflows into bonds...trends unchanged within mutual funds.