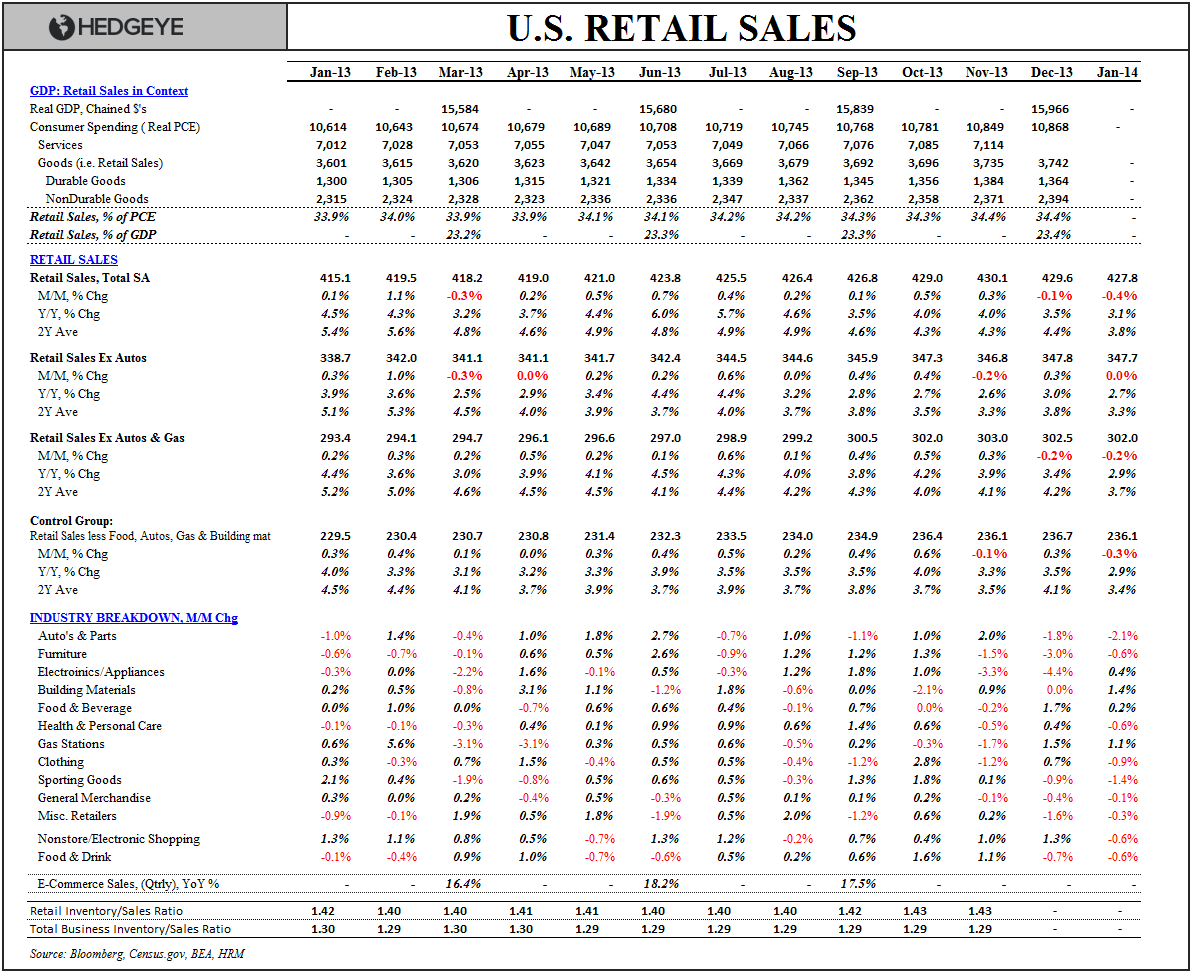

Outside of the now ubiquitous ‘weather’ caveat, it’s hard to paint the January Retail Sales data with a panglossian brush.

JANUARY WEAKNESS: The weakness in auto sales was well telegraphed and drove the decline in the Headline reading for January, but December was revised lower as well and the softness was pervasive with the primary sub-aggregates (Ex-Auto’s, Ex-Auto’s & Gas, Control Group) declining across every rate of change measure – MoM, YoY, 2Y ave.

With respect to calculated GDP, the Control Group decelerated 60bps and 70bps on a YoY and 2Y basis, respectively, while the -0.3% MoM decline was the largest since December 2011.

UPHILL BATTLE: Labor market trends remain okay and the anniversary-ing of the ending of the payroll tax holiday in 2013 should serve as a modest support to retail sales growth this year.

However, with wage growth (at ~2%) running at a negative spread to consumption (at +3.6%) and the savings rate holding little incremental downside (ie. little upside for consumption) the outlook for a material acceleration in retail sales isn’t particularly strong.

Further, If housing continues to decelerate and stocks fail to repeat last year’s performance, luxury and higher end durable sales, driven principally by the top income quintiles, may reverse the notable acceleration observed in 2013.

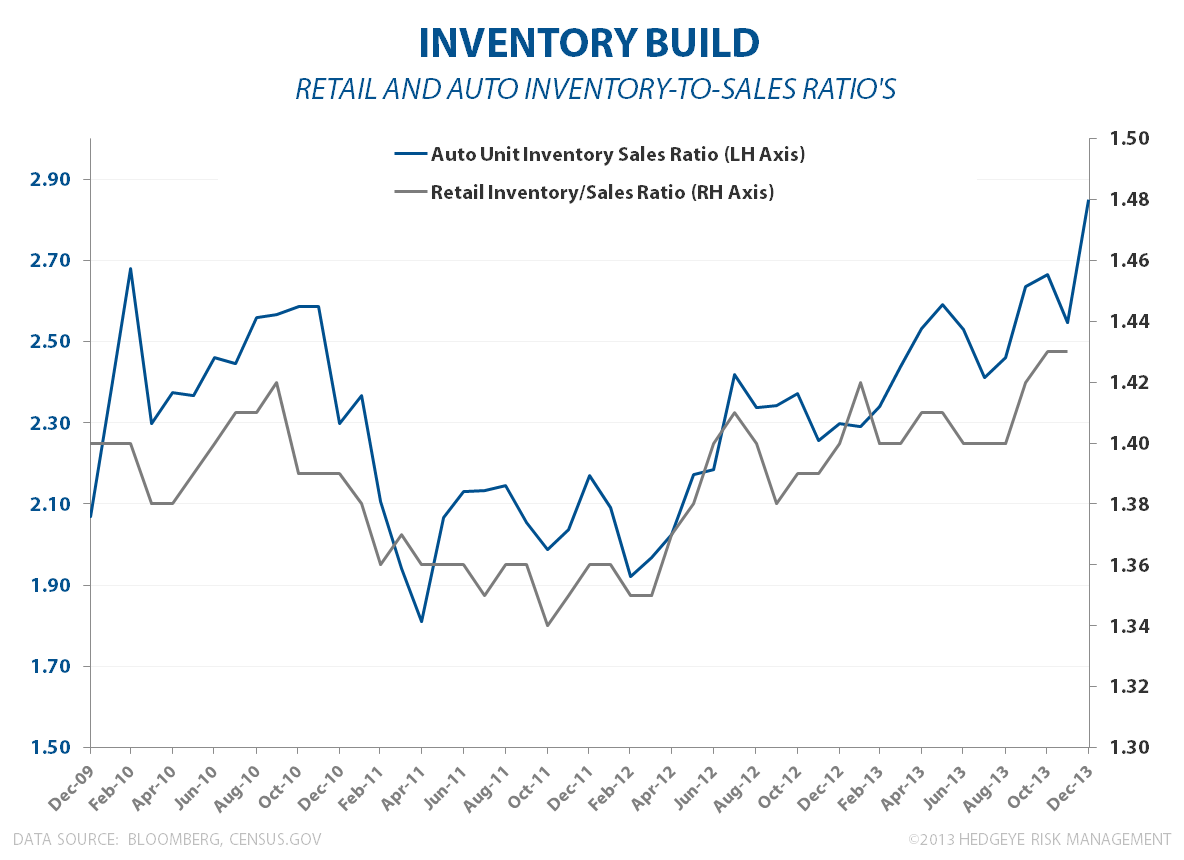

PERFORMANCE RISK: More broadly, a deceleration in sales alongside burgeoning inventory levels at the retail level does not generally augur rising profitability.

Sequential deterioration in operating performance has already begun to manifest in consumer companies in 4q13 earnings and is likely to continue if #InflationAccelerating continues to play out.

As we’ve been highlighting for 6 weeks now, growth isn’t falling apart (yet) but the slope of growth is definitely decelerating on the margin – and macro alpha is (still) typically a game of divining better/worse, not good/bad.

Christian B. Drake

c

@HedgeyeUSA