CAKE remains on the Hedgeye Best Ideas list as a SHORT.

Blame the Weather!

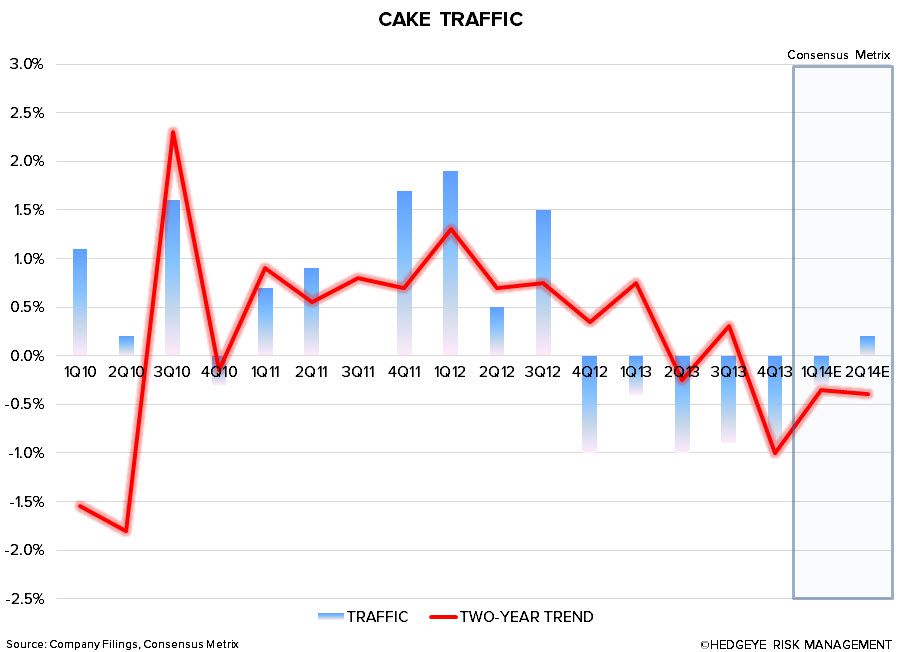

CAKE delivered disappointing 4Q results yesterday after the close, missing comp, traffic, revenue and EPS estimates by 90 bps, 100 bps, 191 bps and 256 bps, respectively. Total comparable sales (+0.9%) and traffic (-1.0%) in the fourth quarter represent sequential slowdowns on a two-year average basis of 80 bps and 130 bps, respectively.

Management blamed unfavorable weather for the poor comp performance in the quarter, estimating that it impacted comparable sales by approximately 70 bps. This number strikes as us rather arbitrary and facile, particularly when considering this estimate excludes a positive impact from favorable weather on the West Coast and a positive impact from lapping Hurricane Sandy.

Our skepticism, however, doesn't end here. We also believe the estimate ignores any pent up demand as a result of unfavorable weather. A couple of weeks ago, we heard CMG management speak directly to this point, noting that higher volume days typically followed periods of poor weather. We didn't hear any of this on the CAKE call. Management also denied any benefit from patio utilization, particularly on the West Coast, which benefitted from record dry and warm weather. Back on the 2Q13 earnings call, management was quick to blame the inability to fully utilize patio space for the disappointing comp performance. The point is, we have reason to believe the underlying trends are weaker than management is leading on.

Any way you slice it, these trends need to be reversed for CAKE to appease investors. Traffic has now been declining for the past 5 quarters (both in favorable and unfavorable weather environments) and, unless fixed, will begin to manifest in margins.

Guiding Down 1Q14 Numbers

Management did its best to reign in 1Q14 expectations during the call by guiding to EPS of $0.48-$0.50 ($0.51 estimate) on 0-1% comp growth (+1.5% estimate). An unfavorable calendar shift (Easter and spring break pushed into 2Q14) and poor weather are expected to negatively impact comps by 50 bps and 90 bps, respectively, in the first quarter. The estimated negative impact from weather (storms in the Northeast, Southeast, and Midwest) factors in everything as of February 11th.

Prior to the release, we surmised the street was too bullish on 4Q13 and 1Q14. This has now been confirmed. We believe the street will need to revise down 1Q14 estimates and, subsequently, FY14 estimates.

Maintaining Full Year Guidance?

Despite the negative recent trends and downward 1Q14 guidance, management reaffirmed FY14 EPS guidance of $2.29-$2.41 on comp growth of 1-2%. Management cited a better than expected outlook for food cost inflation in 2014 (now 3-4%), largely due to a benefit from lower meat, some cheese, and grocery costs. Dairy prices continue to rise and management noted there is not any less risk associated with the potential continuation of this trend.

We believe the bar for FY14 is set too high for CAKE and wouldn’t be surprised if management is forced to guide down full-year numbers after a disappointing 1Q14. The street is currently looking for full-year EPS of $2.38 on comp growth of 1.8%, both of which are at the high end of management’s guidance. We continue to believe a slow start to 2014, softening trends, and downward estimate revisions will lead to multiple contraction throughout the year.

Call with any questions.

Howard Penney

Managing Director