This note was originally published at 8am on January 29, 2014 for Hedgeye subscribers.

“Daddy, that looks like bird poop.”

-Jack McCullough

Nah, he wasn’t talking about the complexion of yesterday’s stock market bounce or Obama’s class warfare speech. My son was talking about the risk-on trade my 2.5-week old baby girl placed all over my shirt last night.

Risk happens fast, and slow.

Back to the Global Macro Grind…

Given that the Russell 2000 hit an all-time high on January 22nd, I think most of you will agree that the “risk-on” trade in being long of big US equity beta happened pretty fast.

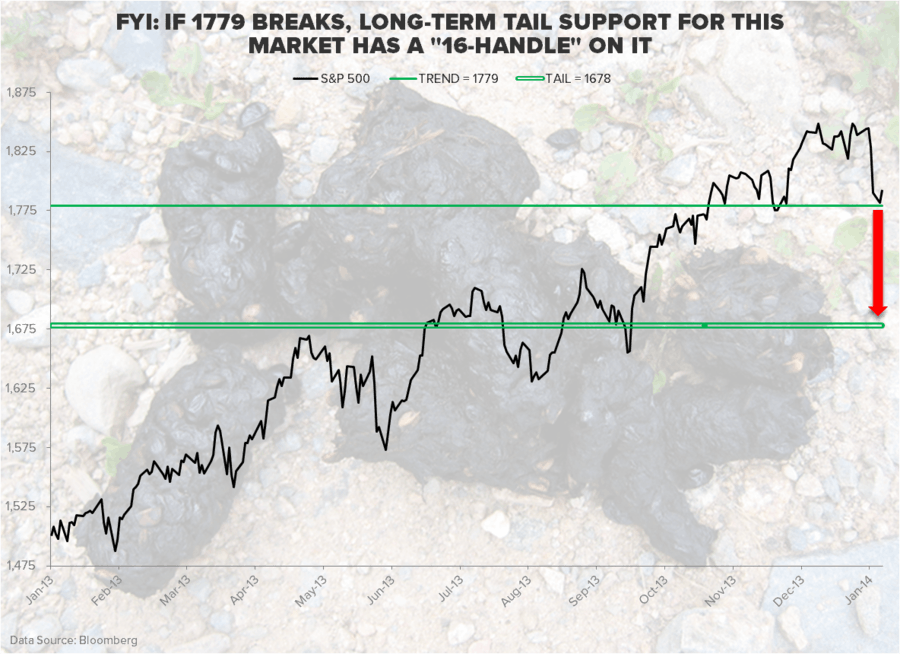

The speed of an information surprise (real-time prices) to the downside can kill both confidence and returns. And I think this is what will keep volatility above @Hedgeye TREND support (VIX TREND = 14.91) for longer than consensus might think.

While consensus isn’t as bullish as it was 4 weeks ago, here’s one way to contextualize sentiment:

- The II Bull/Bear Spread (one of my favs) peaked at +4650 basis points wide to the bull side in DEC (all-time high)

- This morning’s Bull/Bear Spread is +3780 bps wide (that’s a 16% correction)

- The peak in Bulls was 61.7% and this morning it’s down to 53.1% (that’s a 14% correction)

As for the Bears, there still are none that survived all of 2013. By the time it was all over, very few long-only managers were allowed to remind clients they’d been bearish for the last 12 months. Even after last week’s -2.6% drop in the SP500, Bears went from 15.1% to 15.3%. I know, #scary.

Unlike the last three 3-4% US stocks market corrections that we told you to buy, this one has a glaring difference – rather than accelerating both month-to-month and quarter-over-quarter, on the margin, US growth is slowing.

Slowing? Yes. And very evidently so in some of the big stuff that matters:

- HOUSING: New Home Sales missed big on Monday and Case/Shiller Home Prices declined m/m (both are new)

- CONSUMPTION: from Retail Sales to ISM Services and every company check from my analysts = #GrowthSlowing

- ECON CYCLE: yesterday’s New Orders in the DEC Durable Goods report dropped -4.3% m/m (vs +2.6% last)

And sure, people who are in the business of being bullish will give you plenty of excuses (including the weather) as to why slowing is occurring, but few made the call 2-4 weeks ago when the call needed to be made.

Blame Turkey.

No thanks. Did consensus seriously think all these dysfunctional emerging market countries could try what we did (burn their currencies) and not see local inflation rise, consumption growth slow, and social unrest rip?

NEWSFLASH: devaluing the purchasing power of The People is called inflation.

And inflation pays the rich and starves the poor.

Obviously that whole money printing and political power thing (which crushes upward mobility in a society) didn’t make it into last night’s State of The Storytelling. But I digress.

Political digressions, transgressions, and obfuscations aside, what markets cannot seem to get away from is this thing called economic gravity. So let’s try an if/then risk management exercise. If…

A) #InflationAccelerates

B) #GrowthSlows

Then… the stock market sees multiple compression. Period.

If stagflation gets really amped up (think 1970s when American socialists perpetuated it through things like currency devaluation, price controls, and government spending), stock market multiples really get whacked.

Sorry Abby (as in Goldman’s Cohen, who says the SP500 is going to 18x EPS = 2088 this year). If inflation continues to ramp and growth continues to slow, you might have to slap a lucky 13 on that super-duper-magic-market-multiple thing you do.

Actually, god just called and told me 13 “feels a little low.” How about 14x the 2014 consensus EPS = 1624? Jack, that would look and feel like bear poop to me.

Our immediate-term Macro Risk Ranges (with bull or bear TREND in brackets) are as follows:

UST 10yr Yield 2.72-2.80% (bearish)

SPX 1771-1819 (bullish)

Shanghai Comp 1984-2071 (bearish)

VIX 14.91-18.55 (bullish)

USD 80.16-80.79 (bearish)

Pound 1.64-1.66 (bullish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer