TODAY’S S&P 500 SET-UP – February 11, 2014

As we look at today's setup for the S&P 500, the range is 80 points or 3.66% downside to 1734 and 0.79% upside to 1814.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.37 from 2.36

- VIX closed at 15.26 1 day percent change of -0.20%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: NFIB Sm. Biz Optimism, Jan., est. 93.5 (prior 93.9)

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 9am: Fed’s Plosser speaks in Del.

- 10am: JOLTs Job Openings, Dec. (prior 4.001m)

- 10am: Wholesale Inventories m/m, Dec., est. 0.5% (pr 0.5%)

- 10am: Fed’s Yellen testifies to House Fin. Services Cmte

- 4:30pm: API weekly oil inventories

- 8pm: Fed’s Lacker speaks at Stanford University

- 8pm: Fed’s Fisher speaks in Dallas

GOVERNMENT:

- 9am: Obama and Hollande hold state arrival ceremony, 9am; State dinner begins 8:30pm

- 10:15am House Ways and Means Committee marks up H.R. 3865 which would delay IRS rules on 501(c)(4) organizations

- 10:30am Senate Budget Cmte hears from CBO Director Douglas Elmendorf on economic outlook through 2024

- House Republicans plan Feb. 12 vote to boost debt limit until March 2015, restore cost-of-living raises for military retirees

WHAT TO WATCH:

- Fed’s Yellen testifies to House Financial Services Cmte

- KKR to close two funds targeting individual investors

- Obamacare delayed until 2016 for businesses w/ <100 workers

- Ackman sells General Growth shrs to exit holding in mall owner

- Barclays to cut up to 12,000 jobs as 4Q profit falls

- L’Oreal to pay $8.2b to buy back 8% of its stock from Nestle

- Blankfein says EMs in better position than during 1998 crisis

- SEC majority wants to review exchanges’ oversight status

- GM’s China sales rise 12% to record in January on Buick demand

- General Motors to invest 1.5b Zloty in Polish plant: Dziennik

- Porsche to exceed 200,000 in deliveries in 2015 on Macan

- Wall St. vets may be removed from arbitration panels: Reuters

- North Carolina agency may delay own deal with Duke Energy: AP

- Virgin America said to pick Barclays, Deutsche for IPO: FT

- Glencore Xstrata’s 4Q copper output increases 32%

- China auditors plan to file appeal of 6-month U.S. ban

AM EARNS:

- CAE (CAE CN) 8:22am, C$0.18

- CVS Caremark (CVS) 7am, $1.11 - Preview

- Dean Foods Co (DF) 7:01am, $0.18

- Entergy (ETR) 7am, $0.83

- HCP (HCP) 8am, $0.56

- Health Net/CA (HNT) 8:15am, $0.29

- Henry Schein (HSIC) 7am, $1.40

- Huntsman (HUN) 6am, $0.37

- Ingersoll-Rand PLC (IR) 7am, $0.61

- IntercontinentalExchange Group (ICE) 7:30am, $1.95

- LPL Financial Holdings (LPLA) 6:05am, $0.59

- Marsh & McLennan Cos (MMC) 7am, $0.56

- Mosaic (MOS) 7am, $0.43

- National Retail Properties (NNN) 8:30am, $0.28

- Omnicom Group (OMC) 7am, $1.14 -

- PG&E (PCG) 9:02am, $0.42

- Regeneron Pharmaceuticals (REGN) 6:30am, $2.09 - Preview

- Reynolds American (RAI) 6:58am, $0.80 - Preview

- Sprint (S) 7am, ($0.36)

- Zoetis (ZTS) 7am, $0.34

PM EARNS:

- Arch Capital Group (ACGL) 4:01pm, $0.96

- Brookfield Residential Properties (BRP CN) 4:09am, C$0.84

- CNO Financial Group (CNO) 4:03pm, $0.29

- Conversant (CNVR) 4:02pm, $0.57

- Covanta Holding (CVA) 4:01pm, $0.22

- DaVita HealthCare Partners (DVA) 4:01pm, $0.98

- Energen (EGN) 4:30pm, $0.82

- FireEye (FEYE) 4:05pm, ($0.37)

- Fossil Group (FOSL) 4:01pm, $2.43

- Packaging of America (PKG) 5pm, $0.89

- PHH (PHH) 4:03pm, $0.08

- Sangamo Biosciences (SGMO) 4pm, ($0.11)

- Seattle Genetics (SGEN) 4:05pm, ($0.24) - Preview

- Service International (SCI) 4:05pm, $0.24

- Trimble Navigation (TRMB) 4:05pm, $0.37

- TripAdvisor (TRIP) 4pm, $0.21

- Western Union Co (WU) 4:01pm, $0.32

- Willis Group Holdings PLC (WSH) 4:41pm, $0.49

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

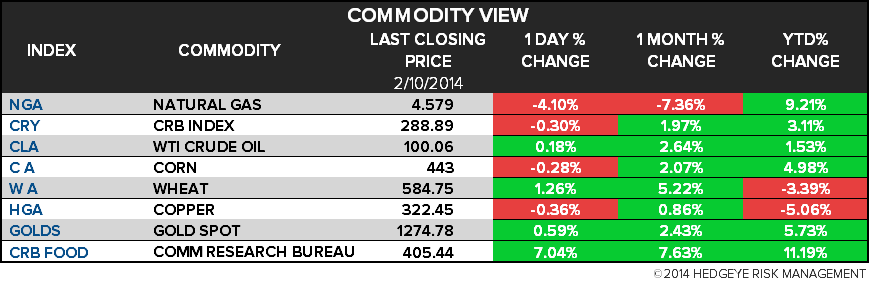

- Natural Gas Rebounds From Three-Week Low on U.S. Winter Storm

- Gold Advances to Highest Price Since November as Dollar Weakens

- Rhodium Bust Ending as Car Sales Fuel Mine Deficit: Commodities

- Sugar Traders Split as Brazil Dryness Weighed Against Surpluses

- Aluminum Trades Near a One-Week High Before Yellen Testimony

- Rebar Touches 17-Month Low as Inventory Gains After Holiday

- Soybeans Extend Losses After USDA Raises Global Supply Outlook

- China Eyes Poultry Consolidation as Bird Flu Cuts Consumption

- Wheat Crop Seen Third-Biggest by Australia on Western Supply

- California Wildfires Erupt Early in Risk to Homes and Vineyards

- Transnet Fights BHP to Win Coal Port Access for Black Miners

- Strong Chinese Steel Demand May Fail to Absorb Iron Ore Glut

- Chinese Coal Firms’ Debt Concerns Sink Shares: Chart of the Day

- WTI Trades Near Six-Week High as U.S. Fuel Supplies Seen Falling

CURRENCIES

GLOBAL PERFORMANCE

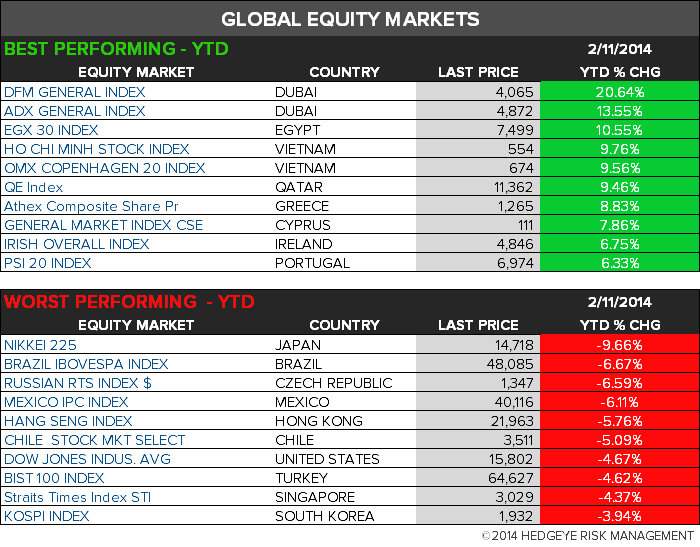

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team