PERFORMANCE vs. THE PRINT: After what feels like a multi-year deference to macro trends and serial crises, forecasting fundamentals has shown a mini-resurgence in 4Q13.

In particular, earnings results relative to expectations have shown a strong relationship to subsequent performance. Bottom line shortfalls continue to be sold hard as eighty percent of EPS misses have gone on to subsequently underperform the market by -5.3% on average.

The relationship between sales beats/misses and subsequent performance has been comparably modest.

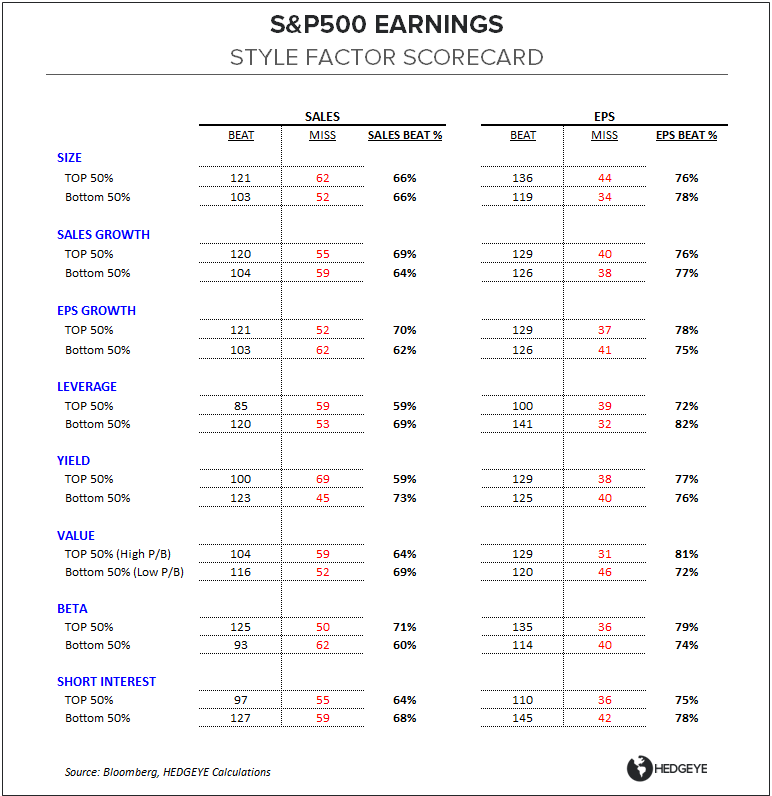

BEAT-MISS: With roughly two-thirds of SPX constituents having reported, Sales & EPS Beat-Miss spreads remain above both the 3Q13 (53%/74%) and TTM (54%/73%) averages as 66% and 76% of companies have beaten Sales and Earnings estimates, respectively. Revenue disappointments out of Consumer Staples companies have emerged as the primary negative divergence.

FUNDAMENTAL PERFORMANCE TRENDS: In contrast to positive Beat-Miss trends, the slope of improvement in operating performance has been decidedly lackluster with just 48% and 53% of companies registering sequential acceleration in sales and earnings growth, respectively.

The percentage of companies reporting sequential operating margin expansion in 4Q13 remained unchanged WoW at an uninspiring 42% according to bloomberg data.

From a sector perspective, Financials and Industrials have led operating performance while Consumer Discretionary and Consumer Staples remained the relative, fundamental laggards.

STYLE FACTOR PERFORMANCE: Reported results vs expectations across style factors has flattened out a bit WoW but High Beta, Low Yield, and Low Leverage equities have performed notably better vs. prevailing topline estimates than their inverses.

Christian B. Drake

@HedgeyeUSA