Please see below Hedgeye analysts' latest updates on our high-conviction stock ideas.

In this week's edition of Investing Ideas, we also feature a special market commentary based on our institutional client macro "Flash Call" earlier this week. In it, we highlight specific areas of economic vulnerability and why investors are rightfully nervous right now.

Finally, we are excited to announce the recent launch of Hedgeye's Internet & Media Sector spearheaded by analyst Hesham Shaaban. At the conclusion of this note, we highlight Hesham's latest research on the stock market's current "darling" and explain why we think "Icarus" is a far more appropriate name.

(Please note CEO Keith McCullough's refreshed "Trend" levels for each stock will be sent out later this weekend.)

IDEAS UPDATES

The latest on Hedgeye's high-conviction stock ideas.

CCL — Record bookings in January bode very well for Carnival Cruise Lines with the lowest expectations on the Street. The cruise operator said it took net bookings (new reservations minus cancellations) for more than 565,000 guests last month. That’s a 17% increase from January of 2013.

Meanwhile, Carnival's website had 13 million visits during January, another record. It remains to be seen whether heavy discounting was the catalyst behind the strong bookings. Unseasonably cold weather likely played a positive role. It is critical for prices to hold steady during mid-Wave. We’ll be updating our proprietary cruise pricing database next week.

DRI — Veteran Restaurants Analyst Howard Penny has nothing material to add to his bullish long-term thesis on Darden this week. We are eagerly awaiting the release of Starboard Value’s plan for value creation with respect to Red Lobster, Olive Garden, etc. We expect that to happen sometime within the next couple of weeks.

In the meantime, the company has been making headlines for offering "free babysitting" for parents while they eat at Olive Garden on Friday, Feb. 7th. To be frank, this “Parent’s Night Out” special is another feeble (laughable?) attempt to drive customer traffic.

A large part of Penney’s bullish thesis revolves around the resurrection of the Olive Garden brand. It is becoming clearer by the day that a new management team or structure is needed for this to happen. In other words, Chairman and CEO Clarence Otis needs to go.

FXB — Hedgeye remains bullish on the British Pound versus the US Dollar (etf FXB), a position supported over the intermediate term TREND by prudent management of interest rate policy from the Bank of England. The BOE continues to be oriented towards hiking, rather than cutting as economic conditions improve. In its interest rate decision on Thursday it kept the main interest rate on hold at 0.50% and its Asset Purchase Target on hold at £375B.

Economic data out during the week continues to confirm our bullish outlook on the economy which we believe should influence the currency higher. While the PMI Services and Manufacturing figures for January slightly underperformed expectations and were slightly below December figures, they remain the highest across Western European countries. We see strong through-put in PMI Construction figures that rose to 64.6 in January versus 62.1 in December (an all-time high since the series was recorded in July 2008). Additionally, the housing market remains elevated – according to the Halifax House Price Index prices rose +7.3% in January year-over-year versus +7.5% in December, and though a bit stale, on a year-over-year basis Industrial Production remains elevated despite a slight decline to +1.8% in December versus a recent high of +2.9% in October.

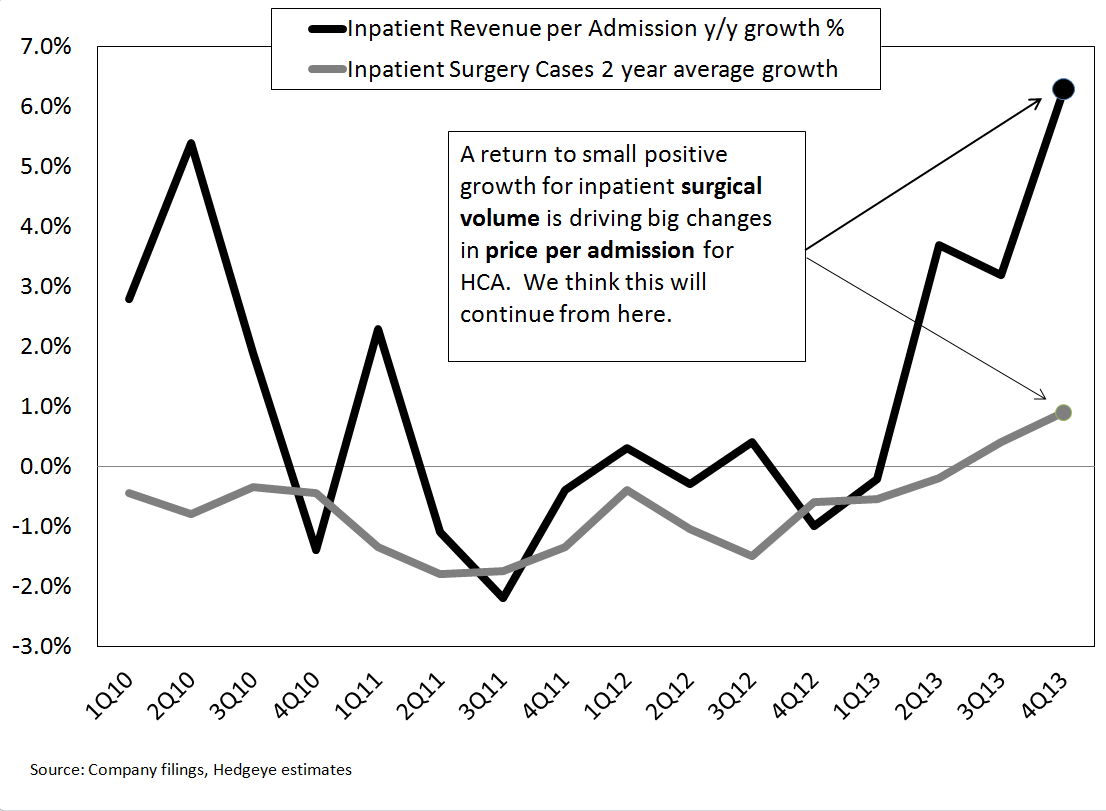

HCA — We've commented frequently in the last few weeks about what appears to be a re-acceleration on surgical case volume across the Orthopedic and Cardiovascular practice areas. These two practice areas, with their high reimbursements and contribution to overall hospital revenue and profits, is critical to the success of any hospital company. For HCA in Q413, it only took a very small recovery in surgical case volume to drive a massive acceleration in their average reimbursement per admission. Staying long HCA or any other hospital is still a difficult decision every day, though. From their Q413 report, which HCA had preannounced, we heard a few new items which on balance we liked. The guidance for 2014 was set reasonably (and low by our estimate) and the incremental profit from the Affordable Care Act was also guided to a very low number at an additional 1-2% of EBITDA for the year, and also likely below what they will realize.

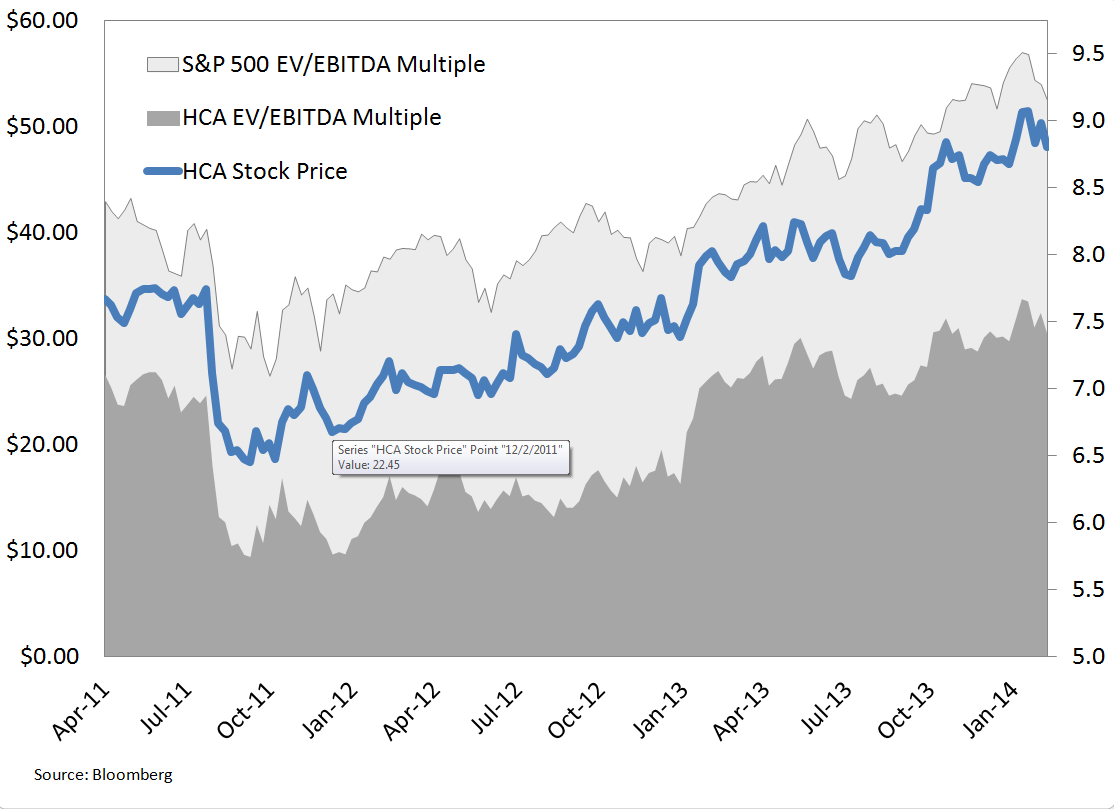

Fundamentals and stock prices can and are often two different things though. But as the charts below suggest, we think the risk from a market move lower is reasonably low from here. Hospitals and HCA typically trade at a discounted multiple to the S&P 500. We've charted the EV/EBITDA ratio for both. With a range of 73% to 89% of the market multiple, HCA's current reading of 80% is right in the middle of the range. Combined with our view that HCA can perform better fundamentally and report better than expected EBITDA numbers, we won't say there isn't any risk, but we're likely in a pretty comfortable position.

We should have the next round of our OB/GYN in the next day or so. We're looking forward to seeing the update on patient traffic and maternity trends. We'll also be sending out a survey to Orthopedic surgeons to ask them about case volume. We were surprised to hear, despite 2 quarters of acceleration and one of the best quarters in the last 5 years, many of the implant manufacturers caution the street heading into 2014 not to expect the trend to continue. Our survey should give us the answer we need.

LVS — Hedgeye Gaming, Lodging & Leisure Sector Head Todd Jordan remains the bull on Las Vegas Sands. While he acknowledges that January gross gaming revenues in Macau were disappointing, he says it could have been due to bad luck in the last couple of weeks of the month. Jordan is much more optimistic on February, given positive anecdotal evidence that we are hearing surrounding the Chinese New Year. For starters, mass traffic has been strong and Las Vegas Sands has several mass-centric properties.

RH — Restoration Hardware is in a particularly dark period now. Not with its business, which we think is still quite healthy, but with its communication with the Street. The company has ended its fourth quarter, but has not yet finalized the books. That process – for some reason we do not understand – takes a particularly long time for RH. The company won’t release earnings for another 1-2 months, which might very well mark the longest ‘quiet period’ for any company in retail. Unfortunately, that lack of information is not RH’s friend. Investors like to speculate about the business, particularly given the horrible results retailers posted in January due to bad weather. Generally speaking, no one speculates that ‘things are going great’. It’s simply not how Wall Street thinks. The good news is that for people who believe in the company’s opportunity, strategy, and execution, weakness in the name based on said factors prove to be a buying opportunity – like we think we have with RH today.

TROW — Shares of T Rowe Price are the second best performing stock in the asset management group year-to-date (behind defensive institutional bond fund manager Legg Mason). With the bulk of substantial outflows from institutional sovereign wealth clients out of the way from the back half of 2013, TROW is now at a positive inflection point to book solid inflows backed by its industry leading performance. TROW’s leading 401k business is still growing above the industry average and with industry-wide retail equity flows having turned up substantially in the middle part of last year, the environment is still incrementally positive for this leading stock fund manager.

We are however getting cautious on the margin that the environment is getting more challenging for U.S. stocks to maintain their upward trajectory but with a solid rebound towards the end of the week in U.S. equities, the environment has stabilized a bit. We are traveling with TROW management at the end of this month and should then get a better idea of if the retail investor is incrementally adding to TROW funds. Until then, TROW shares should rebound with the market after a tough start to the year for equities.

WWW — Wolverine Worldwide is slated to report fourth quarter earnings on Tuesday February 18th before the market opens. While our call on WWW is much more long-term in nature, the reality is that we happen to like it into the print. The stock has gone from $34 to $27 in a month’s time on virtually no news. The company notes that sales were a bit light in quarter relative to expectations, but then it took up its EPS guidance. That’s the kind of company we like – one that offset weakness in the macro climate with its own initiatives to hit financial objectives.

This remains one of the most hated stocks in retail – not quite as much as JCP, but close. We like that – we’d be concerned if it was over-loved. We think that WWW will print upside to earnings, and ultimately will beat every quarter this year (based on current Street estimates).

ZQK — Quiksilver’s female brand, Roxy, was center stage on the first night of Olympic competition in the Women’s Slope Style qualifying run as Roxy endorsed, Torah Bright, kicked off her pursuit to bring home the snowboard triple crown for her home country of Australia. We talked a few weeks back about ZQK’s new endorsement/marketing strategy. In summary – ZQK made the right move to downsize their athlete roster and event sponsorships. Our survey work indicated - ZQK should focus only on the Rockstars to drive brand awareness.

That’s why this Torah Bright development is kind of a double edged sword. On one hand, Roxy has the best female snowboard athlete in the world -- one that could be argued is the female equivalent of Shawn White. We know most people will argue with us on that one. We're huge White fans ourselves. But he is supremely dominant in one event -- the pipe. Torah consistently wins in the halfpipe, snowboardcross, and now slopestyle.

The flip side of this is that Roxy fails to promote her as a top athlete (she’s nowhere to be found on the brands website – check out the image below) -- even though she has a full line of snowboard clothing, and appeals to women and men alike. This just goes to show that ZQK still has underutilized assets at Roxy that could ultimately promote revenue growth.

* * * * * * *

Mr. Market Is Getting a Little Queasy

A Special Economic & Market Update

CEO Keith McCullough led the Macro team earlier this week in a Hedgeye Flash Call, updating our subscribers on our Q1 themes of #InflationAccelerating and #GrowthDivergences. Together with US Macro analyst Christian Drake, Keith walked through the quantitative set-up that has emerged since the beginning of the year.

With the S&P index down roughly 3% year to date, if you own equities, it’s not pretty. As Keith observed in his opening remarks, “Risk has happened pretty fast” since the beginning of the year – just one month, which once again demonstrates that the one certain effect of government attempts to manipulate the economy is to shorten economic cycles, and to increase volatility. From that perspective, the near-universal efforts of the world’s central bankers seem to be having their predicted effect – if not their intended ones.

So Much Inflation, So Early in the Year

The individual investor who finally threw in the towel and bought stocks late last year may be feeling a little bit abandoned right now as they watch the value of their holdings decline almost daily, with nary a pundit in sight to tell them why. Very few of the major Wall Street gurus are talking about the inflation that our macro work sees very clearly. Instead, they are almost uniformly fixated on how much higher the S&P 500 will be at the end of this year – a recent review of top stock market forecasters found the average projection for the S&P this year was 1,955, more than 200 points higher than it was trading as Keith spoke.

Many of these same forecasters underestimated the strength of the market last year, coming in short by more than 15%. We are not sure what continues to qualify them as “top forecasters.” There must by some mystical process at work here to which we are not privy.

Hedgeye’s macro work indicates that commodity prices have begun to break out as other inflationary pressures continue to build. If Fed chair Yellen decides to rescue the equities markets by going back to Quantitative Easing, the impact could re-ignite what has become a Pavlovian response from investors: QE Up, triggering Dollar Down, triggering Yield Chase/Inflation Hedge Assets Up. This would likely spark another round of growth-slowing commodity inflation.

After peaking in 2011-2012, commodity prices subsequently cratered in 2013 as the dollar strengthened and expectations rose for incremental Fed tightening. In that environment pro-growth equities became the asset allocation of choice for both retail and institutional investors.

Notably, the slope of broader inflation – as measured by the CPI – follows the slope of commodity inflation closely. In other words, if commodity inflation accelerates or decelerates sequentially, so does the CPI. So, generally, we can expect broader measures of consumer price inflation to track the move in commodity prices.

Given last year’s price declines, the comps (period-to-period comparisons) are especially easy; thus even a moderate price increase in the commodity complex will look inflationary year over year. This is more an optical effect than an economic reality, but policy is made in response to how things appear, not how things actually are. Even with Princeton PhDs, Washington policy makers generally have no clue how things actually are, while the few people who actually do know how things are can never convince others until it’s too late.

Says McCullough, we are not likely to see 2011-2012 style actual inflation (which by the way the Fed did not see at the time) but as people start to perceive the rise in commodity prices alongside decelerating growth and declining stock prices, there will be speculation that the Fed will again loosen policy in an attempt to help support flagging growth. If Yellen stays the course on the taper, new stock investments could be temporarily good money after bad. If she reverses, then your dollars in the stock market will be the near-term Good Money, while the Dollar in the global context will be Bad and inflation will rise faster. Damned if we do, damned if we don’t.

A Rising Tide of Inflation

We were seeing wage inflation even before President Obama decided to push wage increases through executive order, which is obviously bullish for further wage increases in general. Perhaps more significant, savings rates are declining back towards historic lows as consumption is again displacing saving. Note that, in 3Q13, aggregate household debt growth turned positive for the first time in eighteen calendar quarters (latest data), signaling that credit-driven consumption growth is now back after 5 years of household balance sheet deleveraging. The trend to consumer over-spending is likely to be exacerbated as consumers start to worry about inflation: the propensity to chase rising prices will exert pressure on consumer spending.

On the market side, inflationary pressure is more likely to lead to multiple compression, the very opposite of the expansion most Wall Street strategists are calling for. In Hedgeye’s proprietary four-quadrant model, last year saw Growth Accelerating / Inflation Accelerating. In this scenario, optimism about the economy and enthusiasm about growth lead investors to assign higher P/E multiples to stocks – multiple expansion – and prices rise. But we are rolling out of that scenario – Quadrant 2 in our model. As commodity inflation rises, we risk moving into Quadrant 3: Growth Slowing / Inflation Accelerating. This is the “in-a-box” policy scenario: Damned if you do, damned if you don’t. This stagflationary scenario is not a good place to be, and not an easy one to work out of. There is practically no good policy option except the one that no politician wants to hear: sit tight and wait it out. Meanwhile, consensus is looking for continued multiple expansion this year. Says McCullough, the pundits whose S&P targets fell short by 300 points last year may be on target to overestimate this year’s levels by the same margin.

Investors are not positioned for slower growth and stock price multiple compression. But inflation metrics continue moving forward steadily and quietly. Keith says this could in effect be commodity prices front-running policy; if the Yellen Fed yields to pressure and reverses the tapering process, inflation will charge ahead, as will “the inflation trade.” Already, says McCullough, broad measures of inflation are moving ahead. CRB prices continue to make higher lows. Inflation hedge assets are outperforming, even as stock prices decline – utilities are practically the only equity sector that is working, and gold is regaining its luster. Other inflation indicators are advancing, such as the Prices Paid component in both the ISM Manufacturing and ISM Services Surveys. ISM services new orders – the best lead indicator of future activity in the survey – are back down to the level they were in July 2009, and ISM manufacturing new orders just had its biggest month-over-month decline since December 1980, the eve of a recession that battered the nation for two years.

Durable goods orders, retail sales, consumer trends, housing demand and home prices are all slowing, consumer stock prices are underperforming, and the Treasurys yield spread is compressing, indicating a worsening growth outlook.

Fed Up?

The market appears to be set up for a reversal of the Taper. The minute Yellen hints a return to Quantitative Easing, says McCullough, the full impact of that reversal “will roll right into the CRB.” The markets are already pricing in slower growth and rising inflation and Hedgeye’s macro work indicates the slope of the rate of change in prices continues its upward trend, making the inflationary scenario worse for investors.

Globally, most central banks are engaged in a global bonfire, all rushing to burn their currency faster than their neighbor. Notable standouts include India and the UK, whose central bankers have pushed back on the widespread religion of post-Keynesianism and held the line on their currencies.

Central planners and regulators are busy assuring their citizens that things are under control, but the reality is that regulators don’t know what forces will cause the next crisis. All they can do is make sure the abuses that precipitated the last crisis don’t get out of control again. Meanwhile, we may already be in the midst of the next crisis, as central bankers trash their currencies to stoke price inflation and stimulate exports. The lasting impact of these policies is not economic strength, but greater inequality, with an increasing likelihood of social unrest. Even though pundits here have been discussing the decline in the emerging markets, the US marketplace is not insulated against the possibility of a broad EM collapse.

In this scenario of limited options, the only solid hope on the US policy front would be an unequivocal statement from Yellen that the Fed will continue to taper and continue to tighten. That would strengthen the dollar and help set the US economy back on a growth track. Of course Hope, as McCullough points out, is not an investment process.

Once again the individual investor has been left high and dry. Everyone has been pushing the bull case. Now that it’s not working, no one is trying to unpack the reasons behind the market decline. Keeping their eye on their lofty year-end targets for the S&P, the pundits have taken their eye off the ball: a lot can happen in the coming eleven months.

If the history of market behavior is any guide, by the time the rest of Wall Street wakes up to #InflationAccelerating, it will already be behind us.

* * * * * * *

(Click on the title below to unlock our latest research note on Twitter)

Our original short thesis on Twitter centered around emerging headwinds to two of its core growth drivers 1) Reach (User Growth) and 2) Monetization (Ad Revenue per timeline view). While TWTR is down 33% from its highs, it still trades at a premium to social media comps Facebook and LinkedIn. As soon as the Street realizes that the company can’t grow +50% in perpetuity, the stock will lose further momentum.