SUMMARY BULLETS

- 4Q13 Earnings Exposes Holes in Business Model: Both Membership Growth and Engagement decelerated meaningfully in 4Q. Street is now questioning the runway for both growth drivers. We believe User Growth is the bigger issue.

- Biggest Hole Yet to Emerge: Monetization has been a considerable growth driver, but running out of runway. Growth likely to decelerate beginning 2H14/2015.

- Consensus Estimates Rising: Estimates are up with the 4Q13 earnings and 2014 guidance beat; the mistake is increasing already-lofty 2015-2016 estimates as well

- But Continue to See Near-Term Upside: We see consensus estimates for 1H14 as more than achievable. Since the stock has already taken a hit, a near-term beat could refuel optimism.

TWTR 4Q13 EARNINGS SUMMARY

- Revenues: 4Q13 Revenue of $245M, beating both our estimate of $218.9M and consensus of $218.1M

- Membership (Reach): Monthly Active User (MAU) growth came in lower than we expected at 30% y/y vs. our estimate of 38%. US Growth decelerated to 20% y/y, vs. 33% in the prior quarter

- Timeline Views/User (Engagement): Declined -3% y/y, decelerating from the 8% growth in prior quarter.

- Ad revenue/timeline view (Monetization): accelerated sharply, up 76% y/y vs. 49% in prior quarter.

- 2014 Guidance: $1.15-$1.20B vs. consensus of 1.13B and our estimate of $1.08B. 1Q14 revenue guidance of $230M-$240M is ahead of our original estimate of $230, and well ahead of prior consensus of $214.

SHORT THESIS SUMMARY

Our original short thesis centered around emerging headwinds to two of TWTR’s core growth drivers 1) Reach (User Growth) and 2) Monetization (Ad Revenue per timeline view).

- Reach (Membership Growth): Our major concern was understated penetration; particularly in the US. We have seen studies suggesting that as many as 50% of twitter’s total users are no longer active; meaning TWTR already penetrated a larger portion of the US population than its Monthly Active Users (MAUs) metrics suggest. Average Revenue per User (ARPU) in the US is considerably higher than the international market (8x greater), so if US slows, international can’t compensate

- Monetization (Ad Revenue per timeline view): This has been an accelerating source of growth for TWTR over the LTM. However, we believe this has a limited runway because it was largely driven by what we call the “Mobile Migration”, which we see as a non-recurring/waning benefit. The “Mobile Migration” is the combination of TWTR introducing its main ad products to its mobile platform (where the company has had greater success with monetization) while users were steadily adopting the mobile app. The former can’t be repeated; the latter is near full penetration. The only other options from here is to introduce new ad products, or the ad load itself; both will test the loyalty of its users.

SHORT THESIS UPDATE

- Reach: TWTR only picked up an additional 1M users sequentially in 4Q13 ( up 2% q/q). For perspective, FB picked up 2M users despite US Monthly Active User (MAU) penetration that is over 3x that of TWTR (73% vs. 22%, respectively). We continue to believe the upside to TWTR’s user growth is limited since total US penetration is higher than its MAU metrics suggest. The emerging question is whether TWTR's addressable market is as large as FB’s, and if it can achieve comparable penetration down the road.

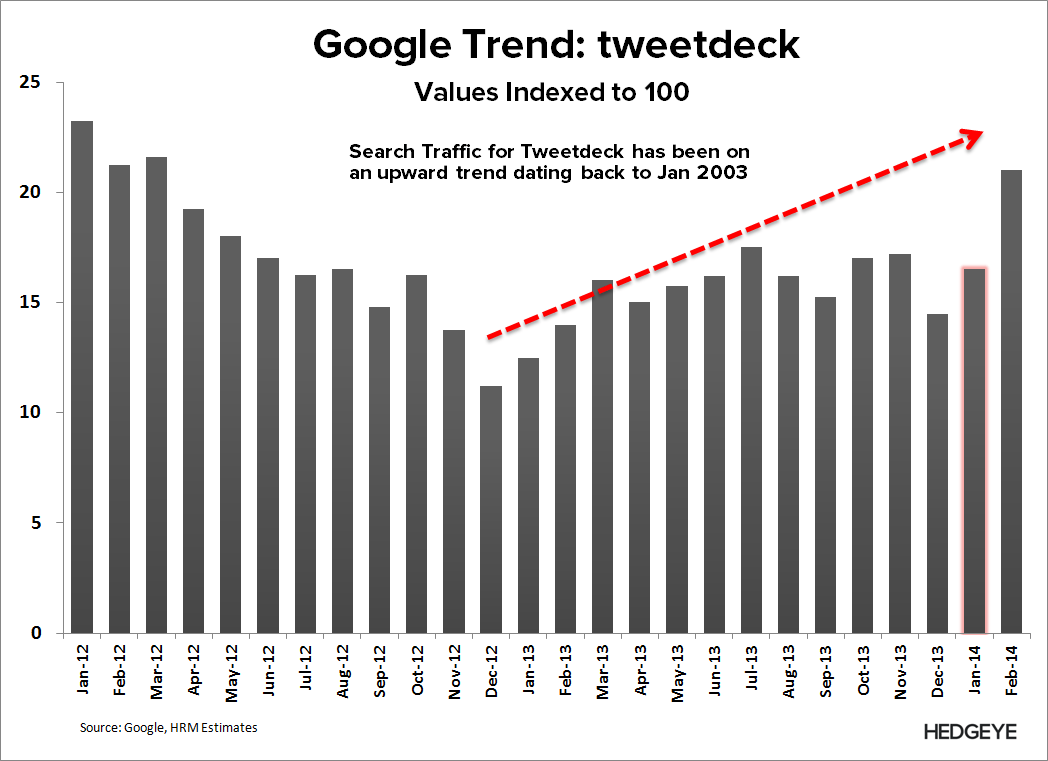

- Engagement: the 4Q deceleration in timeline views/MAU is concerning. Management suggested that user interface improvements limited the need to refresh the site as often, which is how it measures timeline views. While plausible, we believe that users gravitating over to TweetDeck, where the company can’t measure timeline views, may also be partly to blame. The latter would be concerning since we do not believe the company is effectively monetizing the TweetDeck platform.

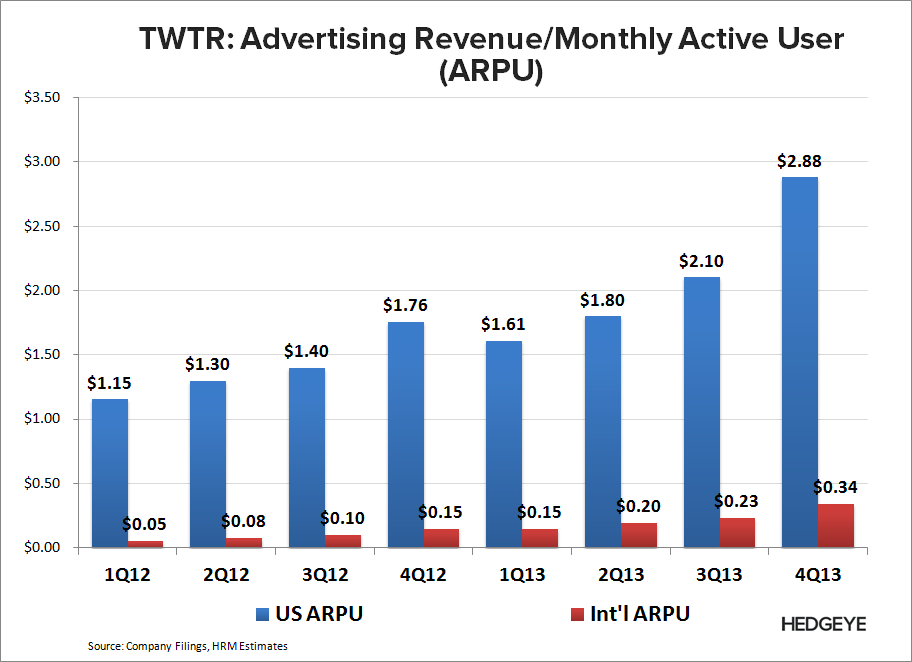

- Monetization: the 4Q acceleration in ARPU suggests the Mobile Migration may have more near-term upside than we originally thought; although we suspect some of that acceleration is due seasonal spike in 4Q ad spending (holiday shopping season). Regardless, our thesis hasn’t changed. Mobile drove substantially all of TWTR’s 4Q13 ad revenue growth. With mobile now representing over 75% of all ad revenue (vs. 55% in 4Q13), the runway gets shorter from here. The comp setup switches from mobile representing the minority to majority of revenue moving forward.

CONSENSUS ESTIMATES LOFTY, BUT MORE REASONABLE NEAR-TERM

Following the beat on both 4Q13 Estimates and 2014 Guidance, Consensus estimates have risen substantially. Where we take issue is 2H14 and 2015; more so on the latter. While it may be premature to look that far out, TWTR’s stock will ultimately trade on growth expectations. While TWTR is down 33% from its highs, it still trades at a premium to social media comps FB and LNKD. As soon as the street realizes that company can’t grow +50% in perpetuity, the stock will lose further momentum.

Timing that catalyst is the challenge; especially since we see upside to 1H14 estimates. TWTR’s 4Q13 results have rebased expectations for the Reach and Engagement operating metrics, so we expect revenue growth will become the more important driver for the stock near-term.

SUMMARY CHARTS

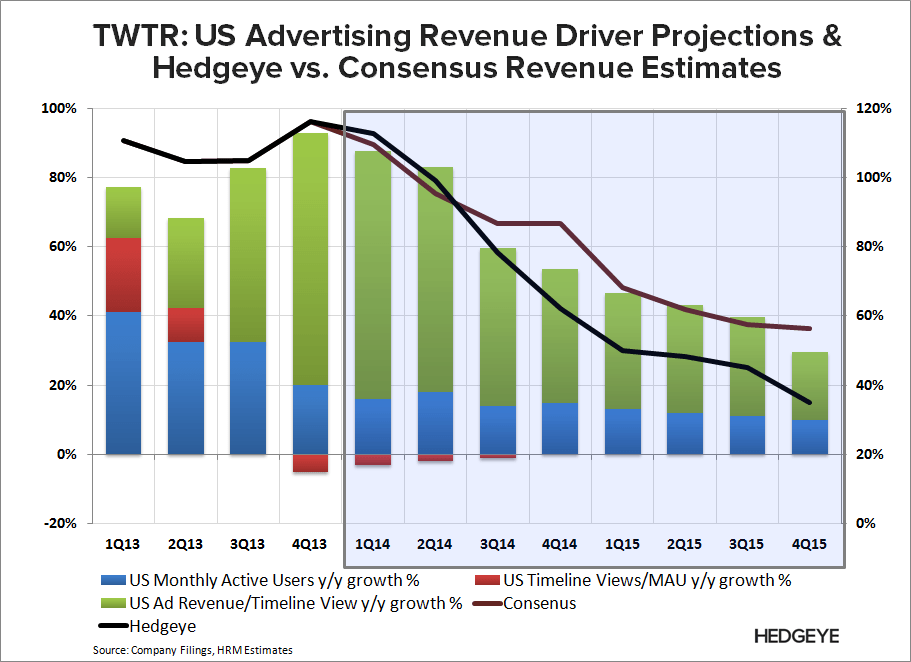

User Growth: Significant Slowdown in US User growth. We suspect TWTR's US penetration is much higher than its MAU metrics suggest given that some users have joined and are no longer inactive. Runway is shorter than many expect.

Engagement: Decelerated Considerably, which management suggest is partly due to Twitter interface improvements, but we believe users migrating to TweetDeck is also to blame. We suspect this could a secular theme, which would pressure ARPU.

Monetization: the Mobile Migration may have more immediate upside than we originally thought, although we suspect some of the 4Q13 acceleration is due the holiday shopping season.

Hedgeye vs. Consensus: We see upside in the near term to consensus estimates, but we expect ARPU growth to slow beginning 2H14 as the mobile tailwind begins to subside. With mobile now representing over 75% of all ad revenue, the comp setup switches from mobile representing the minority to the majority of revenue moving forward.

Valuation: This is just for perspective. TWTR trades at a much higher multiple than its peers, but that can be explained by the lofty growth estimates assumed by consensus. As soon as the street realizes that company can’t grow +50% in perpetuity, the stock will should trade more inline with its peers.

<chart10>

Let us know if you have any questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeHC2