Editor's note: The excerpt below is a complimentary look at Hedgeye's Morning Newsletter written by CEO Keith McCullough. This morning's missive was delivered by Daryl Jones, Director of Research, who filled in for Keith who is currently meeting with institutional clients in Boston. To learn more about Morning Newsletter click here.

Currently, the SP500, Dax and Nikkei are all broken on the TREND duration (three months or more) in our quantitative model. Conversely, equity market volatility via the VIX and U.S. Treasury bonds are breaking out to the upside.

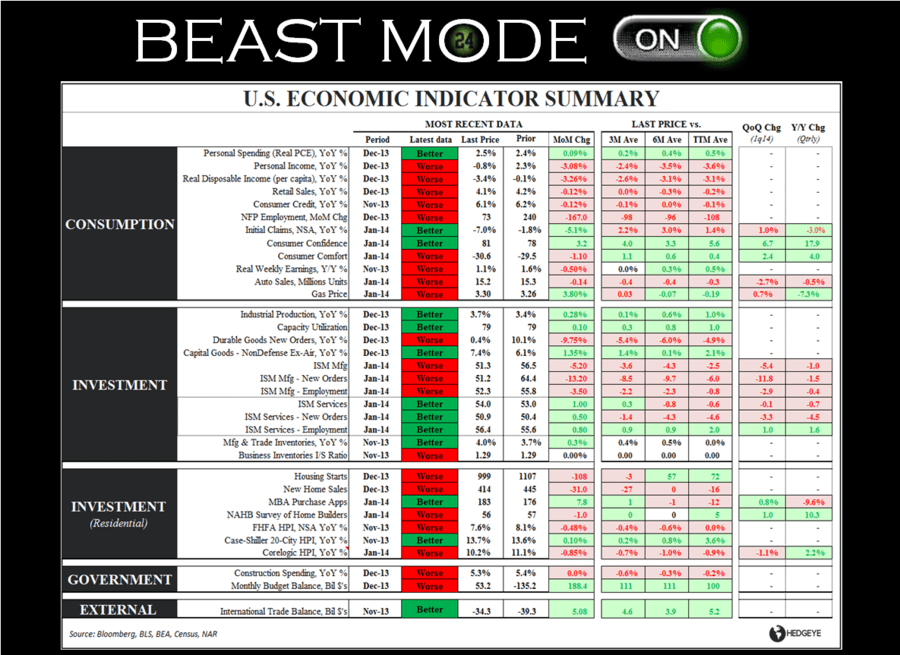

Clearly, the market is signaling that growth is poised to continue to disappoint. In the year-to-date, the score on that front is really crystal clear. In the “Chart of the Day,” we show a summary of the 34 U.S. economic indicators that we focus on. As the table shows, 23 of those indicators slowed from December to January. Not even the best portfolio defense is going to stop an equity market that is going down because of that kind of economic deceleration.

In my mind, the most disturbing recent data point was the ISM Manufacturing New Orders reading for January. On a month-over-month basis, new orders were down -13.2, which is the largest single month decline since December 1980, or more than 30 years ago. The economy slowed from December to January and if forward looking orders are any indicator, it is not out of the woods yet.

Yesterday, the weekly initial jobless claims data was released and they were largely a non-event, though even there we are seeing incremental slowing. We key off the year-over-year rate of change in rolling NSA (non-seasonally adjusted) initial jobless claims. This week the data was better by 5.5% vs the same period last year. However, if you compare that with the preceding three weeks of data, it reflects a modest deceleration. The last four prints have been: -8.5%, -7.9%, -7.2% and -5.5%. So, yes, the strength of the labor market has cooled off modestly.

On the labor and employment front, the January Employment Report at 8:30am will be the main event this morning. Currently, consensus estimates are for 180,000 jobs to be added in January. It is also widely expected that last month’s big miss will be revised significantly higher due to weather. So, the expectations table has been set but, as always, expectations are likely to be the root of all heartache.

…perhaps today’s employment report is highly positive and gets the market back into bullish beast mode, though the probability seems higher that today is a non-event with the potential for a mild disappointment. But, as always, by 8:31 a.m. it is definitely going to be all about that action.

Speaking of action, we finally got some validation on our short thesis on Twitter yesterday as the company reported its first quarterly results as a public company. Admittedly, revenue did beat our number (although that was obviously priced in), but Twitter showed a real deceleration in user growth and user engagement. On that last point, user engagement, as measured by time line views, was down -3% year-over-year . . . not good for a growth company.

… $TWTR remains on our Best Ideas list as a short. Email us at sales@hedgeye.com if you want to review our 50+ page short report on the company.