“I’m just about that action, boss.”

-Marshawn Lynch

Admittedly, being from Canada, I didn’t grow up a huge football fan. But like most of the world, I am drawn to the Super Bowl. This year was set up to be a dandy with the best offense facing the best defense. As we now know, the game was not even close with Seattle beating Denver like a rented mule.

Despite the lopsided game, there were a number of characters off the field that garnered a fair amount of attention. In my view, the most interesting character to emerge was Seattle running back Marshawn Lynch, who is better known as Beast Mode.

Lynch is notorious for avoiding the media, so much so that the NFL fined him $50,000 earlier in the season for not going to press conferences (which Seattle fans subsequently repaid for him!). At the Super Bowl he spent about seven minutes in a media scrum and also did a brief interview with Deion Sanders. During these brief appearances, it became clear that Lynch wasn’t media shy per se, but wanted his actions to speak for him. As he told Sanders:

Deion Sanders: What is your thing?

Marshawn Lynch: Laying back, kick back. (Yeah) Mind my business, stay in my own lane.

Deion Sanders: Yeah. So you’re just going to sit in the cut and just chill. That’s what you do.

Marshawn Lynch: Just kick back. Game time, though I’ll be there.”

True to his limited words, at game time Lynch was there and was all about the action, rather than the words beforehand. In theory, this is probably good advice for a lot of us, even those of us who don’t play in the NFL.

Back to the global macro grind . . .

Speaking of action, many of the key global markets we monitor every day are increasingly about that price action. Currently, the SP500, Dax and Nikkei are all broken on the TREND duration (three months or more) in our quantitative model. Conversely, equity market volatility via the VIX and U.S. Treasury bonds are breaking out to the upside.

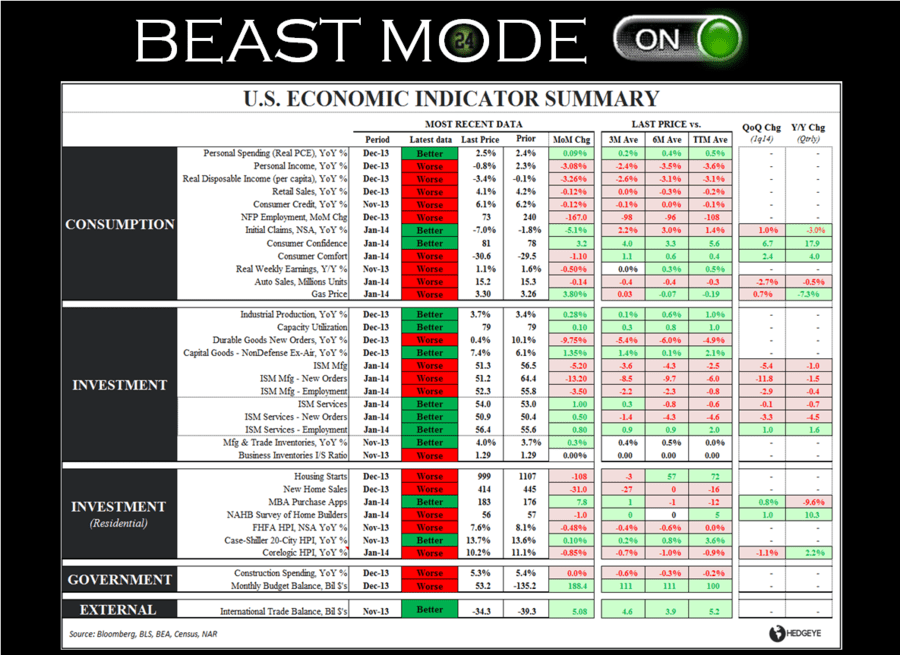

Clearly, the market is signaling that growth is poised to continue to disappoint. In the year-to-date, the score on that front is really crystal clear. In the Chart of the Day, we show a summary of the 34 U.S. economic indicators that we focus on. As the table shows, 23 of those indicators slowed from December to January. Not even the best portfolio defense is going to stop an equity market that is going down because of that kind of economic deceleration.

In my mind, the most disturbing recent data point was the ISM Manufacturing New Orders reading for January. On a month-over-month basis, new orders were down -13.2, which is the largest single month decline since December 1980, or more than 30 years ago. The economy slowed from December to January and if forward looking orders are any indicator, it is not out of the woods yet.

Yesterday, the weekly initial jobless claims data was released and they were largely a non-event, though even there we are seeing incremental slowing. We key off the year-over-year rate of change in rolling NSA (non-seasonally adjusted) initial jobless claims. This week the data was better by 5.5% vs the same period last year. However, if you compare that with the preceding three weeks of data, it reflects a modest deceleration. The last four prints have been: -8.5%, -7.9%, -7.2% and -5.5%. So, yes, the strength of the labor market has cooled off modestly.

On the labor and employment front, the January Employment Report at 8:30am will be the main event this morning. Currently, consensus estimates are for 180,000 jobs to be added in January. It is also widely expected that last month’s big miss will be revised significantly higher due to weather. So, the expectations table has been set but, as always, expectations are likely to be the root of all heartache.

Since the r-squared between the ADP number and non-farm payrolls on a rolling 3-month basis is 0.71, it does seem likely that we get a print of close to 180,000. This disappointment may come on the expectation of a meaningful revision upwards from December. In fact, we did a study last month on the trend in revisions and in general over the last four years, the magnitude (and direction) of revisions hasn’t correlated particularly well with deviations from trend. Historically, according to Bloomberg data, months in which big weather was a factor have been revised higher only ~60% of the time.

So, perhaps today’s employment report is highly positive and gets the market back into bullish beast mode, though the probability seems higher that today is a non-event with the potential for a mild disappointment. But, as always, by 8:31 a.m. it is definitely going to be all about that action.

Speaking of action, we finally got some validation on our short thesis on Twitter yesterday as the company reported its first quarterly results as a public company. Admittedly, revenue did beat our number (although that was obviously priced in), but Twitter showed a real deceleration in user growth and user engagement. On that last point, user engagement, as measured by time line views, was down -3% year-over-year . . . not good for a growth company.

After winning the Super Bowl, Marshawn Lynch answered when asked about his touchdown run that he had:

“Kicked it all off, boss.”

Given the dramatic price decline and acceleration in volume, it will be interesting to see what Twitter kicked off yesterday. $TWTR remains on our Best Ideas list as a short. Email us at if you want to review our 50+ page short report on the company.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.59-2.80% (bearish)

SPX 1 (bearish)

Nikkei 139 (bearish)

VIX 14.91-20.41 (bullish)

Gold 1 (neutral)

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research