TODAY’S S&P 500 SET-UP – February 6, 2014

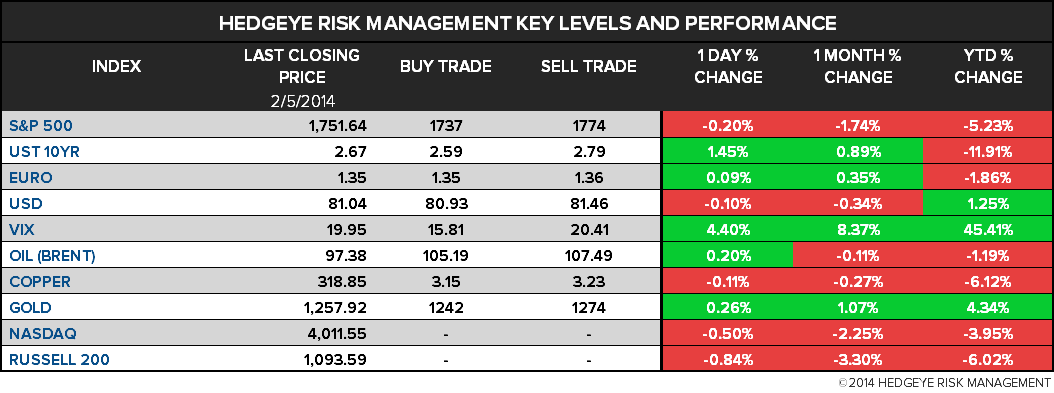

As we look at today's setup for the S&P 500, the range is 37 points or 0.84% downside to 1737 and 1.28% upside to 1774.

SECTOR PERFORMANCE

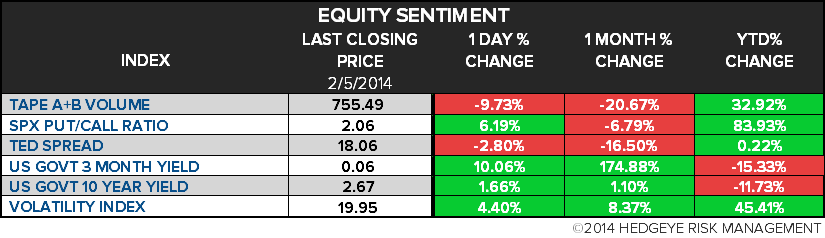

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.36 from 2.36

- VIX closed at 19.95 1 day percent change of 4.40%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: RBC Consumer Outlook Index, Feb. (prior 51.5)

- 7:30am: Challenger Job Cuts, y/y, Jan. (prior -5.9%)

- 8:30am: Trade Balance, Dec., est. -$36b (prior -$34.3b)

- 8:30am: Nonfarm Productivity, 4Q preliminary, est. 2.8%

- 8:30am: Initial Jobless Claims, Feb. 1, est. 335k (pr 348k)

- 9:45am: Bloomberg Consumer Comfort, Feb. 2 (prior -31.8)

- 10am: Fed’s Tarullo Senate testimony on financial stability

- 10am: Freddie Mac mortgage rates

- 10:30am: DOE Energy Inventories

- 5:30pm: Fed’s Rosengren speaks in Sarasota, Fla.

GOVERNMENT:

- 9:30am House Oversight and Govt Reform Cmte hearing on IRS targeting investigation

- 10am: Fed’s Daniel Tarullo testifies before Senate Banking Cmte’s “Oversight of Financial Stability and Data Security"; w/Treasury Under Sec. Mary Miller; FDIC Chairman Martin Gruenberg; Comptroller of the Currency Tom Curry; SEC Chairwoman Mary Jo White; Acting CFTC Chairman Mark Wetjen

WHAT TO WATCH:

- Coca-Cola to buy 10% stake in Green Mountain for $1.25b

- Twitter’s easy growth stalls as CEO vows to address slowdown

- Jan. retail sales seen hurt by clearance, weather

- Sony sees full-yr loss; plans job cuts, sale of PC business

- Disney’s profit tops ests. as "Frozen" heats up box office

- Apple removes Bitcoin program Blockchain from app store

- SoftBank said to seek decision on T-Mobile bid within wks

- Buyout firms CVC to Carlyle said to weigh bid for Deoleo

- Credit Suisse 4Q profit misses ests. on legal provisions

- GM adds Nissan-built cargo van to take on Ford Transit Connect

- U.S. said near deal with EU on reprieve for swap-trading rules

- IBM to spend $100m to bring Watson technology to Africa

- Ford to cut third of Australia plant jobs as demand declines

- Amazon buys video game developer Double Helix: Re/code

AM EARNS:

- Advance Auto Parts (AAP), 8:30am, $0.81

- Aetna (AET), 6am, $1.36

- AOL (AOL), 7am, $0.61 - Preview

- Apollo Investment (AINV), 7:30am, $0.21

- Carlisle (CSL), 6am, $0.87

- Cummins (CMI), 7:30am, $1.97 - Preview

- Diamond Offshore Drilling (DO), 6am, $0.81 - Preview

- Dunkin’ Brands Group (DNKN), 6am, $0.40

- Exelon (EXC), 7:30am, $0.54

- Flowers Foods (FLO), 6am, $0.19

- Fortis (FTS CN), 7am, C$0.48

- Gartner (IT), 7am, $0.69

- General Motors (GM), 7:30am, $0.87 - Preview

- Graphic Packaging Holding (GPK), 7:30am, $0.10

- Kellogg (K), 8am, $0.82 - Preview

- KKR (KKR), 8am, $0.89

- Monster Worldwide (MWW), 7:30am, $0.11

- New Gold (NGD CN) 7:30am, $0.04 - Preview

- New York Times (NYT), 8:30am, $0.16

- Nu Skin Enterprises (NUS), 7:30am, $2.01

- Och-Ziff Capital Mgmt (OZM), 7:30am, $0.83

- Patterson-UTI Energy (PTEN), 6am, $0.22

- Perrigo (PRGO), 7:42am, $1.60

- Philip Morris International (PM), 6:59am, $1.37 - Preview

- PPL (PPL), 7am, $0.50

- Sally Beauty Holdings (SBH), 7:30am, $0.36

- Saputo (SAP CN) 11:59am, C$0.74

- Sealed Air (SEE), 7:30am, $0.37

- Shoppers Drug Mart (SC CN) 7:45am, C$0.86

- Sigma-Aldrich (SIAL), 7am, $1.01

- Snap-on (SNA), 7am, $1.56

- Spirit Aerosystems Holdings (SPR), 7:30am, $0.65

- Teradata (TDC), 6:55am, $0.85

- Teva Pharmaceutical Industries (TEVA), 7am, $1.40 - Preview

- Towers Watson (TW), 6am, $1.33

- Twenty-First Century Fox (FOXA), 8am, $0.33 - Preview

- USG (USG), 8:30am, $0.10 - Preview

- Wisconsin Energy (WEC), 7am, $0.59

PM EARNS:

- Activision Blizzard (ATVI), 4:05pm, $0.73

- Expedia (EXPE), 4pm, $0.85 - Preview

- Fifth Street Finance (FSC), 4:37pm, $0.25

- FMC Technologies (FTI), 4pm, $0.65

- Genpact(G), 4pm, $0.26

- LinkedIn (LNKD), 4:05pm, $0.38 - Preview

- Lions Gate Entertainment (LGF), 4pm, $0.47

- NCR (NCR), 4:02pm, $0.79

- Neurocrine Biosciences (NBIX), 4:02pm, ($0.17)

- News (NWSA), 4:05pm, $0.19

- Noble Energy (NBL), 5pm, $0.59

- ON Semiconductor (ONNN), 4:05pm, $0.14

- Republic Services (RSG), 4:05pm, $0.46

- Tempur Sealy (TPX), 4:03pm, $0.62

- Ubiquiti Networks (UBNT), 4:05pm, $0.45

- VeriSign (VRSN), 4:05pm, $0.60

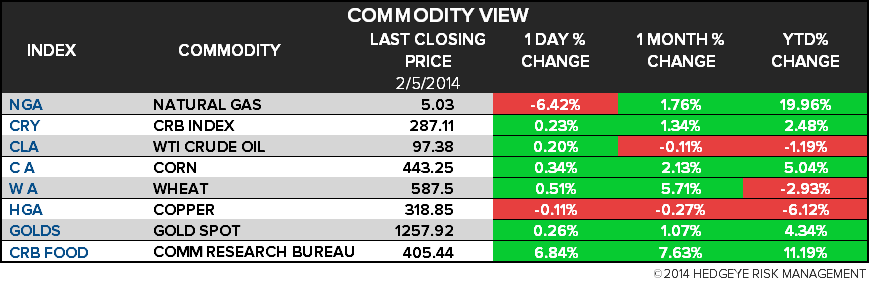

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Crude Rises a Third Day as U.S. Chill Erodes Fuel Stockpiles

- Cotton Crop in Australia Declining to Three-Year Low on Drought

- Virus Killing 5 Million Pigs Spurs Hog-Price Rally: Commodities

- U.S. Natural Gas Rises as Inventories Seen Declining on Weather

- Nickel Rises Amid Speculation Stainless Steel Will Fuel Demand

- Gold Reversal May Signal Lows for U.S. Stocks: Chart of the Day

- Wheat Trades Near Highest in Three Weeks Amid Signs of Demand

- Arabica Coffee Falls First Time in 8 Days; Sugar Little Changed

- Japan Turns to U.S. Wheat Amid Delays in Shipments From Canada

- Rice Farmers in Thailand Urge Stockpile Sales to Meet Payments

- World Food Prices Drop to 19-Month Low as Sugar to Grains Slide

- Tightly Knit Europe Gas Grid Matches Local Need With Global Feed

- Oman’s $3 Billion Railroad Plan to Blunt Iran Oil Risk: Freight

- Gold Holds Below 1-Week High as Silver Extends Best Run in Month

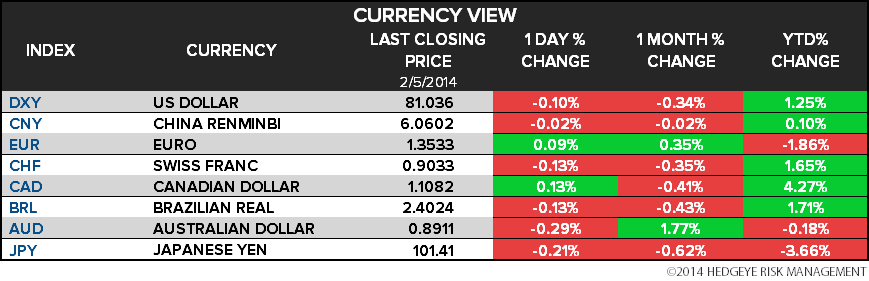

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

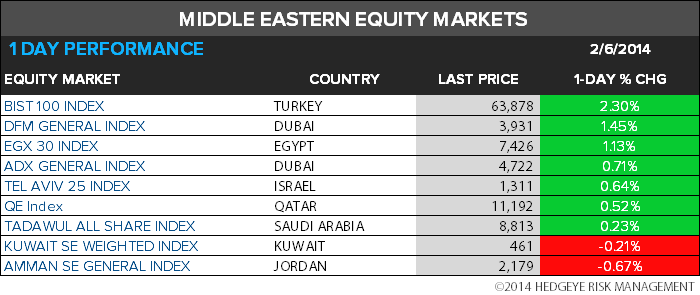

MIDDLE EAST

The Hedgeye Macro Team