Conclusion: Three months ago, we definitely did not like RL’s quarter. Sales were sluggish, margins were weak, inventories high, and management was in a clear and questionable transition. Fast forward to today’s results, and most of those issues have been addressed. Don’t get us wrong, there was more we disliked than we liked in the 3Q results, but given the horrific operating environment, the company redeemed itself today – even if the market does not agree. To be clear, we still would not buy the stock here. Near-term catalysts are simply nonexistent, and we have to wait another 15 months for double digit EPS growth. The stock has grown into its multiple – so we’re only looking at about 16-17x forward earnings today, which isn’t egregious. But unlike three months ago, there are so many other outstanding businesses with rock solid fundamentals that are simply at fire-sale prices. If the stock is still sitting here in another 9-12 months, we’ll likely be more constructive. But here and now – it’s got no go-juice.

Here are some key takeaways from the quarter…

- Beat, Kind Of: Yes, RL beat the quarter -- which is a feat in itself for any company in this tape -- by $0.06 per share. That’s the good news. We’d note, however, that that’s only about a 2% beat. Still better than the alternative, but this isn’t like what we’ve seen out of some other high-quality consumer companies. On the downside, a lower tax rate accounted for anywhere between $0.05-$0.10 of the $0.06 upside, and lower SG&A spend helped by another $0.02-$0.03 relative to our expectations. Earnings tailwind from SG&A and taxes is never something we look at with a company’s results and get overly excited about. We want sales and gross margin.

- Sales: The top line looked really good this quarter. Can’t take anything away from RL there. To excel on the top line in a climate when consumers generally are not buying anything is a testament to the geographic and category portfolio. Sales were up 9.1% (11% in constant currency) -- an acceleration from the 2.8% level we saw in 2Q. Solid acceleration…

- …But: We at least need to acknowledge the shift in the Chaps business from a license to consolidated wholesale operation. The impact on profitability should not be meaningful at first, but the impact on revenue should be considered. It’s impossible given the information at hand to determine the precise math, but the way we see it, it’s possible that 100% of the revenue growth associated with the Wholesale business is derived from simply switching over Chaps from Licensing to Owned. Here’s our math – Licensing revenue was down about $6mm. That included strength in the core licensing business, which tells us that reallocated Chaps revenue was probably a number in the high single digits. Let’s say $8mm. Now we need to apply a royalty rate to gross it up to a wholesale equivalent. Normally, we’d use something around 7-8%. Let’s be conservative and use 5%. That equates to about $160mm wholesale equivalent, which is the rough amount Wholesale should have been up due to Chaps alone. But wholesale was only up by about $110mm. One could make the case that the business was down excluding Chaps. You can poke holes in our assumptions and royalty rates, but directionally, this is something to consider when applauding the growth rate of the wholesale business. To be clear, this reclassification of licenses has been a core part of the Ralph story for a long time, and it has worked brilliantly. They’ll probably crush it with this Chaps business as well. But we simply want to make people aware of the underlying real organic growth.

- This is stating the obvious, as the stock gave up its 7% pre-market gain (and then some) nearly immediately after the CFO noted profitability trends – but margins are expected to be down in fiscal 2015 (March). This is largely due to global expansion of the POLO brand, higher quality/cost of goods, ecommerce investment to support growth in US, Europe, Asia (Korea, Japan), SAP implementation in Europe Let’s assume that the company can leverage Chaps and its new business initiatives and grow the top line 10% -- at best we’ve got a mid-high single digit growth rate until the 2016 fiscal year. That’s a long time to wait for profitable growth.

- Management surprised us on the upside. Last quarter’s call was almost painful to listen to -- it sounded grossly inconsistent with a company of Ralph Lauren’s caliber. There was no question the company was going through transition in its executive ranks, and the conference call all but confirmed that premise. But today, the group was focused around one brand message, and all were clear and concise. We know, this seems like kind of a fluff point to comment on, but with a company like RL where the people up top are such a driving force behind the product, brand, culture and company we think it matters. Most notable, we were running for the hills after last quarter. Today, this risk is far diminished after this quarter.

- Other Notables

a. Europe - Europe up HSD in C$ YY- Northern Europe is growing and southern Europe is stabilized

i. Opportunities - Polo - Flagship in NY (Fall '14), Flagship in London ('15) - Regent St

ii. Actively looking for property in US, Europe, Asia

iii. Women's Polo (Fall '14)

iv. Men's tailored line (Fall '14)

b. China - will begin to actively open stores beginning in FY '15

i. Hong Kong Ralph flagship next fall

c. E-commerce - grew at a high teens rate

i. 10% of revenue in US retail

ii. Still investing in Europe dot.com which will most likely turn profitable in this Year

iii. Asia (Japan and Korea) just getting started with that investment

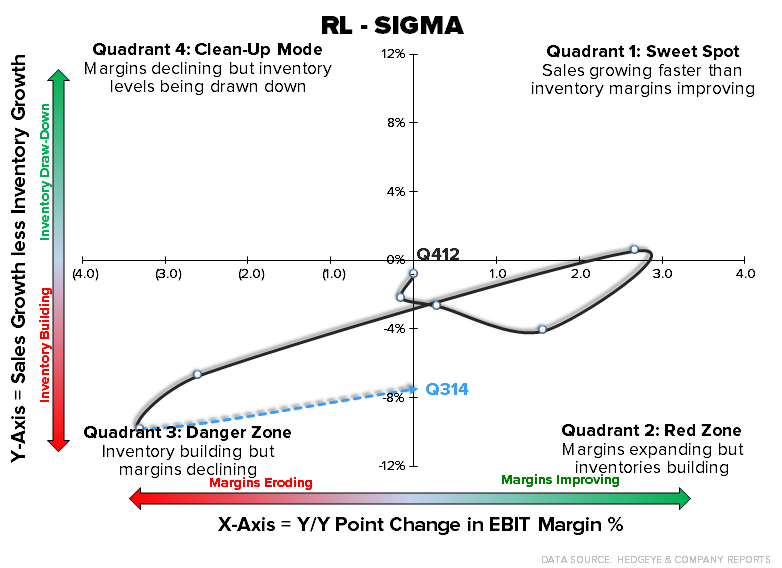

7. SIGMA Analysis Looking Rough

Inventories still not looking good relative to sales. On top of that, the company swung into positive margin territory. While that's better than the alternative, usually when a company has positive margins and a negative inventory spread it proves to be bearish for the stock. That's not our opinion, it's a proven fact based on a few thousand tickers over time. In general, after being in the quadrant where margins are down and inventories are unfavorable, the move the market wants to see is improved inventories, even if it is at the expense of margin. That's almost always a positive stock move.