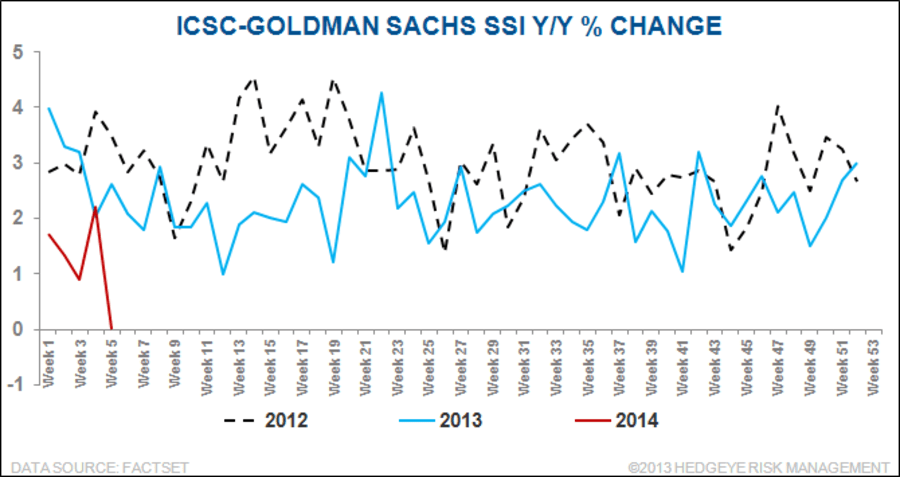

Takeaway from Hedgeye Retail Analyst Brian McGough: This is simply abysmal news for retail. We haven't seen a flat year-over-year reading like this in the ICSC-Chain Store Sales Index (an index of 80 chain store retailers) since February 2010. Now, you can call it weather, you can call it whatever you want. We keep it simple here at Hedgeye. We just call it terrible.

Something is wrong here.