Long term hurdles remain but we’ve got some reasons to believe these stocks could outperform over the short term.

September and December were horrible months for regional gaming companies. Q3 earnings were impacted but Q4 will likely prove far worse. The bad news: regional gaming faces a long-term secular headwind of demographics so growth will continue to be difficult to achieve. The good news: December’s swoon was more math driven than a further deterioration in demand. The upshot: despite very poor weather, January should outpace very low expectations and mark an upward trend, culminating in a potential flat February. By comparison to December, a flat February will make these stocks look like growth companies.

So bad news seems reflected in the stocks:

- All states have released December GGR – cat’s out of the bag

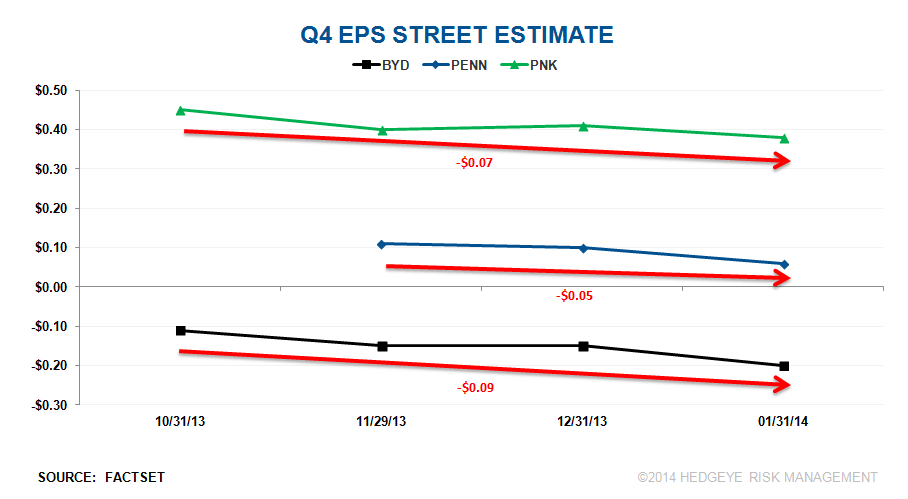

- Earnings have come down dramatically – buy side even lower we think

- Stocks have been blasted YTD

- BYD pre-announced yet stock climbed 10% on Friday

- Investors are expecting an even worse January given the weather

With the bad news mostly in – there is a risk of further 2014 estimate reductions during earnings season – it may not take much for a reversal with the right catalyst. Our regional gaming model predicts sequential improvement December to January (even with the weather) and from January to February which could actually be flat YoY. A couple of positive data points could be the short term tonic these stocks need.

What happened to these once loved real estate plays?

Since the11/15/12 PENN announcement that it was splitting into a REIT and an operating company, regional gaming stocks exploded. Lost through the new real estate lens was the fact that regional gaming revenue growth was lagging badly behind other consumer sectors despite a growing economy. Earnings estimates have consistently shrunk over the same period. Investors didn’t care until the states released September gaming revenues (down 9% in the aggregate) and companies generally missed earnings expectations. However, the stocks came surging back through the end of the year.

This time it’s different

Pushed on by a bad stock market and the bad December GGRs, investors punished regional gaming stocks. BYD, PENN, and PNK are down 12%, 20%, and 20%, respectively, YTD as can be seen in the chart above. The December (and September) downtowns were entirely predictable and similarly, a January/February recovery may be in the works.

In our October 10/31/14 note “OCTOBER SURPRISE”, we correctly predicted the October rebound from the awful September – also correctly predicted. On January 3, we released “THE DECEMBER SURPRISE” calling for a near 10% decline in December regional gaming revenues”. What is our point? Our point is that our model works and the model is now predicting sequential improvement in January despite the bad weather and – hold on to your seat – actual flat YoY February. Hooray! See below.

Bad demographics should continue to pressure regional gaming revenues. Younger generations are just not interested in slot machines. We’ve written extensively about this secular headwind so we won’t rehash here. However, these volatile stocks can move significantly with ‘on the margin’ catalysts. We think the emergence of 2 sequentially better data points will be those catalysts. BYD, PENN, PNK should all benefit.

BYD probably maintains the most upside if they can fix operations. Their properties run at significantly lower margins and revenue per gaming position than the competition in most of the company’s markets. A senior management addition or change is probably necessary to affect the turnaround but no doubt the potential is there. Since BYD pre-announced EPS already, it is the lower risk play into earnings. Not surprisingly, PENN is furthest from its recent peak and without a real estate angle, is a pure play on regional gaming with no real estate angle. The luster has worn off of PNK – the Wall Street darling of the bunch until recently.