Summary:

Last week's risk monitor argued for being cautiously opportunistic on the long side as the interbank risk measures remained benign, Euribor-OIS & TED Spread, in spite of the growing concern around EM market and currency risks. This week is a different story. On Friday of last week we saw the Euribor-OIS spread hockey stick higher. We also saw a notable upward move in the TED Spread. These have historically been two of the most accurate risk gauges in signaling when to move from an aggressive to a defensive posture. They're indicating fairly clearly now that the situation is deteriorating. Couple that with our quantitative line of intermediate-term support (TREND: $21.36) in the XLF being broken, and there are clear, bright-red warning signals flashing. We'll heed them until they tell a different story.

Key Points:

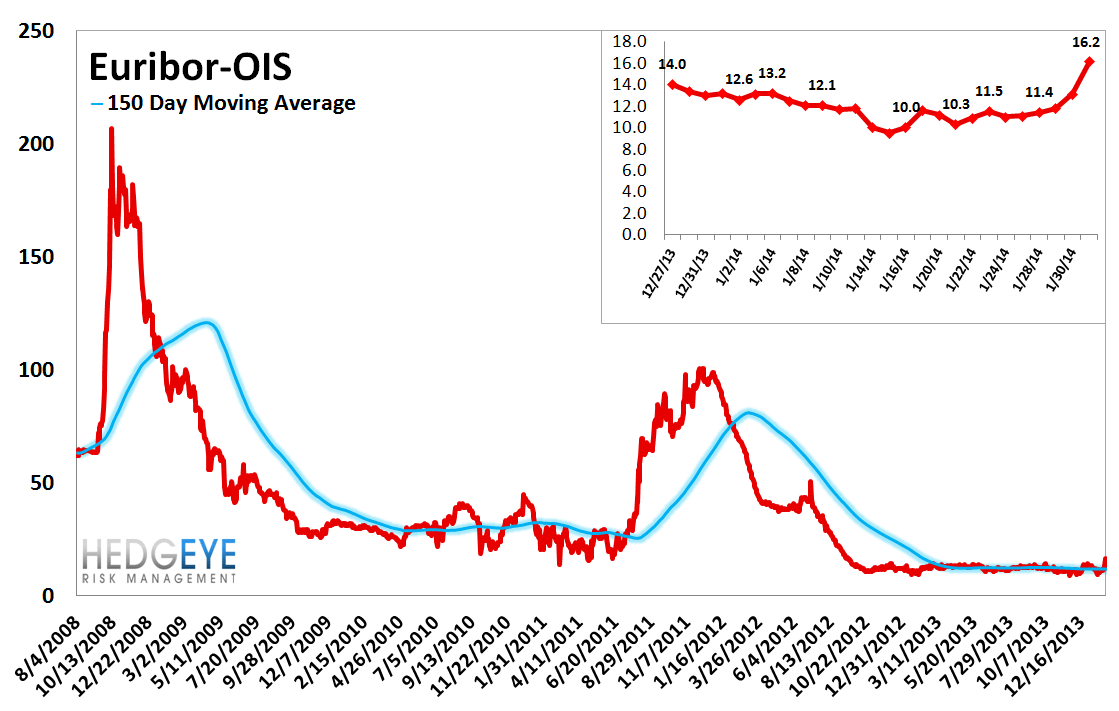

* The Euribor-OIS Spread widened by 5 bps to 16 bps.

* The TED Spread rose 2.7 basis points last week, ending the week at 21.4 bps

* U.S. Financial CDS - Citi continues to lead the charge among the large cap banks as north of 40% of its revenue comes from Emerging Markets. Its swaps widened 6 bps vs last week and are now 23 bps wider month-over-month. Mortgage insurers, MTG & RDN, both saw sizeable upticks in their swaps week-over-week as well. The insurance complex is also buckling amid falling rates.

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 0 of 13 improved / 8 out of 13 worsened / 5 of 13 unchanged

• Intermediate-term(WoW): Negative / 1 of 13 improved / 10 out of 13 worsened / 2 of 13 unchanged

• Long-term(WoW): Positive / 5 of 13 improved / 0 out of 13 worsened / 8 of 13 unchanged

1. U.S. Financial CDS - Swaps widened for 23 out of 27 domestic financial institutions. Citi continues to lead the charge among the large cap banks as north of 40% of its revenue comes from Emerging Markets. Its swaps widened 6 bps vs last week and are now 23 bps wider month-over-month. Mortgage insurers, MTG & RDN, both saw sizeable upticks in their swaps week-over-week as well. The insurance complex is also buckling amid falling rates.

Tightened the most WoW: TRV, JPM, SLM

Widened the most WoW: AIG, MET, HIG

Tightened the most WoW: AGO, MBI, MTG

Widened the most MoM: C, AXP, GNW

2. European Financial CDS - Swaps were slightly wider, on average, across European banks last week, but, looked at on a month-over-month basis, continue to push higher. Italian banks are showing some of the worst performance on a month-over-month basis.

3. Asian Financial CDS - It was a mixed week for Asian Financial CDS as swaps were mostly wider across China, Japan and India, but a few banks posted substantial tightening.

4. Sovereign CDS – Sovereign swaps were modestly wider last week, outside of Japan and Portugal.

5. High Yield (YTM) Monitor – High Yield rates rose 6.7 bps last week, ending the week at 6.02% versus 5.95% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 1.0 points last week, ending at 1849.

7. TED Spread Monitor – The TED spread rose 2.7 basis points last week, ending the week at 21.4 bps this week versus last week’s print of 18.74 bps.

8. CRB Commodity Price Index – The CRB index rose 1.0%, ending the week at 283 versus 281 the prior week. As compared with the prior month, commodity prices have increased 2.1% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

9. Euribor-OIS Spread – The Euribor-OIS spread widened by 5 bps to 16 bps. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

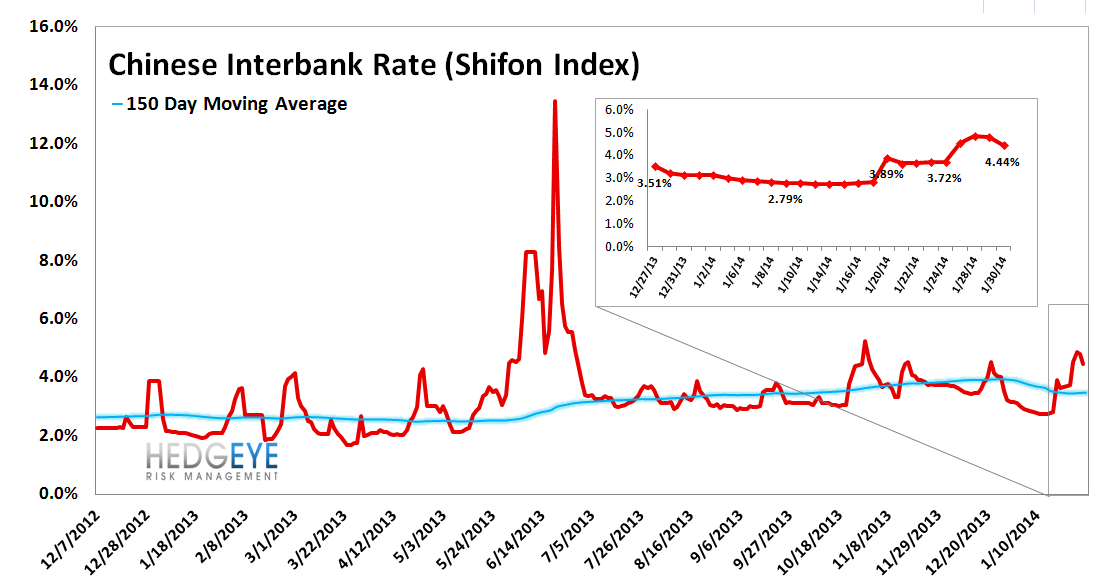

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 72 basis points last week, ending the week at 4.44% versus last week’s print of 3.72%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

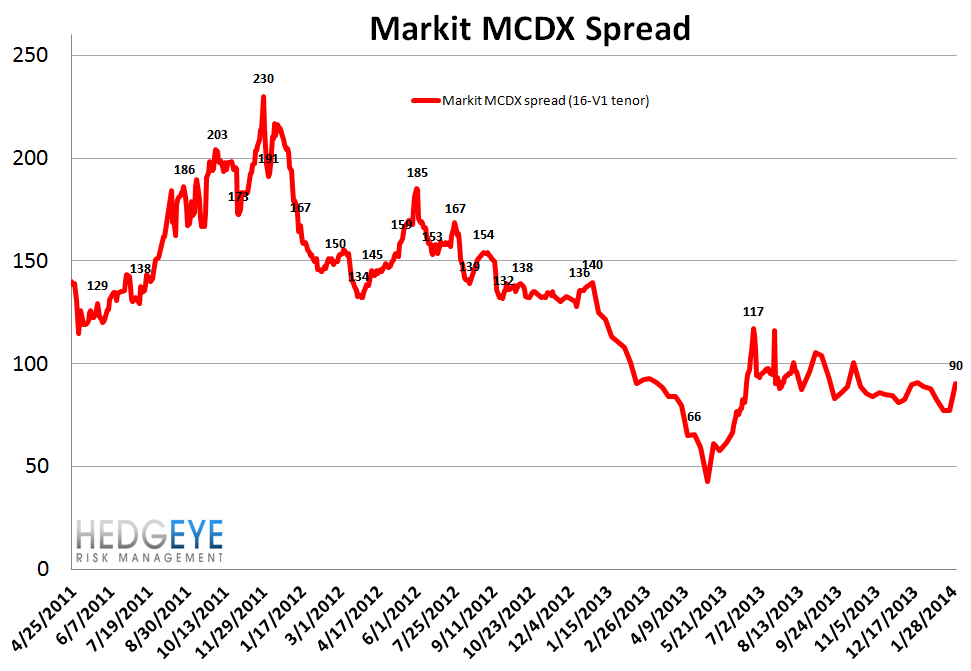

11. Markit MCDX Index Monitor – Last week spreads widened 13 bps, ending the week at 90 bps versus 77 bps the prior week. The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. We track the 16-V1.

12. Chinese Steel – Steel prices in China were unchanged last week but remain down 2.7% month-over-month at 3,404 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 232 bps, -6 bps tighter than a week ago. The yield spread is now 29 bps tighter month-over-month. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Quantitative lines of support in the XLF are now broken on both a TRADE (short-term) and TREND (intermediate-term) basis. Our Macro team’s quantitative setup in the XLF shows 3.0% upside to TRADE resistance and 2.1% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT