Below are Hedgeye analysts' latest updates on our high-conviction stock ideas as well as CEO Keith McCullough's refreshed levels for each stock. At the conclusion of the note, we have selected three institutional research notes we believe offer a valuable look into the current state of the markets, as well as two deep stock dives on the long and short side.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

The latest on Hedgeye's high-conviction stock ideas.

CCL — Carnival was added to Investing Ideas on 11/22/13. Since then, shares have risen 9.2% compared to a 0.7% return for the S&P 500. The Gaming, Lodging & Leisure team will update on CCL next week.

DRI — Activist investor Barington Capital held a conference call this past Thursday to review its strategy for value creation at Darden. The plan called for a separation of the struggling Olive Garden and Red Lobster brands from the higher growth brands. Barington also expressed a desire to improve management focus and operational execution, unlock the value of the company’s real estate portfolio, and further reduce operating expenses.

Barington cited Managing Director Howard Penney’s research several times during the call and ended the session by suggesting the company should immediately “appoint an independent chairman to protect shareholder interests.” As expected, the bull case is gaining steam and we are waiting for the other activist, Starboard Value, to present its plan for value creation in a couple of weeks.

FDX — We removed FedEx from Investing Ideas on Friday. Click here for the full report.

FXB — Hedgeye remains bullish on the British Pound versus the US Dollar (etf FXB), a position supported over the intermediate term TREND by prudent management of interest rate policy from the Bank of England. The BOE continues to be oriented towards hiking, rather than cutting as economic conditions improve.

HCA — The massive acceleration in the US Orthopedic market is having a positive impact on HCA Holdings and the other Hospitals. The big question is ... will it continue? Zimmer, the largest manufacturer of hips and knees, saw a remarkable 9% growth in US Knees. However, they cautioned analysts to not extrapolate the last two quarters of strength through 2014.

For now, we think growth will continue to accelerate based on our macro analysis. We show in the charts below that the housing recovery has led to faster employment growth among municipal governments. Why does this matter? Because municipal workers make up roughly 16% of the workforce, are much older than the average worker, and carry very good health benefits.

But we're not going to leave it at one or two data items. We're planning to run a survey in February to ask Orthopedic surgeons how full their schedule is during Q114. If we're right, we should hear they are all very busy. What does this mean for HCA? Remember, Orthopedics is the single largest revenue driver for Hospitals at 17%. More positive preannouncements from HCA seem likely if the Ortho trend continues.

JPM — Our intermediate and long-term outlook on JPMorgan are unchanged from a week ago – we remain bullish. However, we’re keeping a close watch on the macro risk factors across Emerging Markets, namely the currency dynamics in areas like Argentina and Turkey. Along those lines, we’ve included an excerpt below from JPMorgan’s most recent 10-K (year-end 2012), which shows their risk by country for their top 20 countries in which they do business, excluding the US. We’ve highlighted the three of those countries that appear to be near the top of the risk pile amid this current environment of rising EM concern. The company has some exposure to Brazil, India and Russia, though, for perspective, none of the three are Top-5 exposures, and collectively represent less than 2% of total assets.

While this should offer investors some comfort, the reality is that global banks like JPMorgan will trade, in the short term, largely based on sentiment around the perceived risk – rising or falling – in these emerging markets. From our vantage point, we are much more interested in the “contagion” risk dynamic, which we actively monitor by watching both the TED-spread domestically and the Euribor-OIS spread in Europe – to date, neither of these measures has shown much reaction to what is happening in emerging markets. Were that to change, we would likely change our view on the performance outlook for JPM shares.

The table below shows JPMorgan’s Top 20 exposures by country (excluding the U.S.). The selection of countries is based solely on the company’s largest total exposures by country.

Click to enlarge

LVS — Gaming, Lodging & Leisure Sector Head Todd Jordan added Las Vegas Sands to Investing Ideas earlier this week. Click here for the full report.

RH — In September, Retail Sector Head Brian McGough wrote a research note arguing that people are asking the wrong questions about Restoration Hardware. The key question according to McGough “is when it will earn $8.00 per share. We think the answer is 2018…That’s $6.50 in incremental earnings in 5-years. Put a different way, that’s a 40% earnings CAGR. Use that as ammo next time anyone tells you that RH is too expensive or that ‘they already missed it’.”

While shares have clearly been under pressure since then, McGough remains convinced that RH’s long term growth story is incredibly bullish. His conviction is fueled by square foot acceleration, new categories, and increased store productivity which is currently being obfuscated by the quarterly guessing game. The quarters and share price will and ebb and flow, but there is no change to his $8.00 in EPS thesis by 2018 highlighted in his note.

TROW — In case you missed it, T Rowe Price reported its fourth quarter earnings results this week, beating consensus on both revenues and earnings and also finishing with record all-time assets-under-management (AUM).

Importantly in the quarter, TROW reported slight complex-wide inflows, which broke a streak of 2 quarters of substantial outflows which had been driven by a handful of Asian sovereign wealth management clients.

After speaking to TROW management after its results, we believe that the bulk of sovereign wealth redemption process is completed as remaining assets in those accounts are "substantially diminished" now according to management. Thus as we move forward into the New Year, TROW can again start to put up improved inflows, which has historically driven a premium valuation versus its peer group.

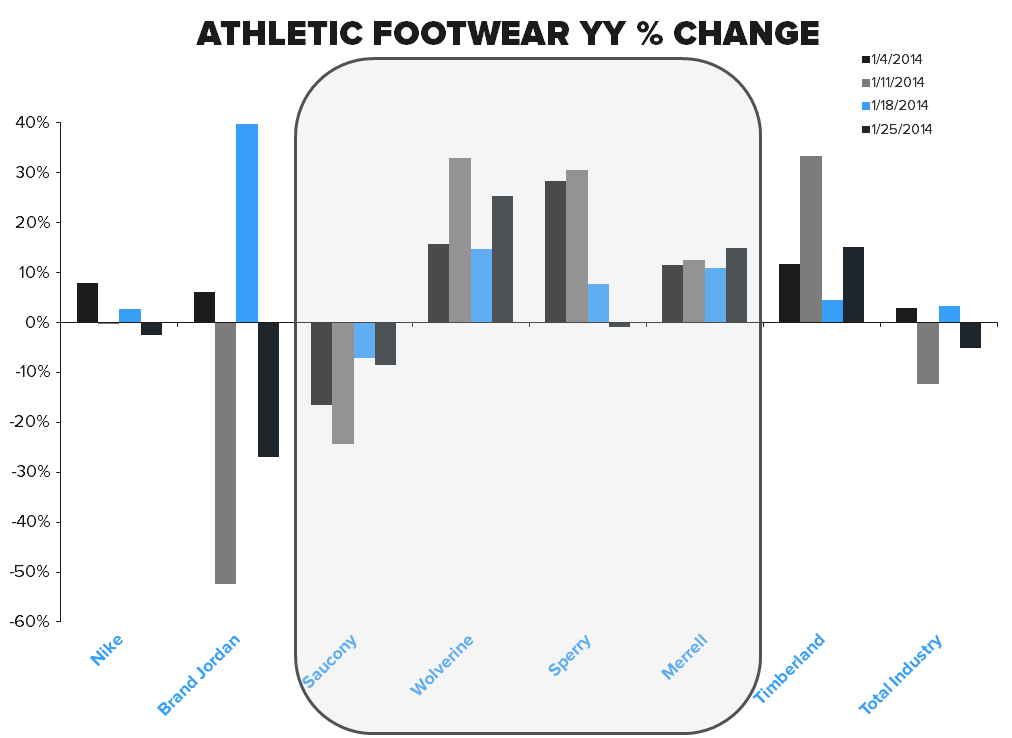

WWW — Wolverine Worldwide has arguably the most diversified brand portfolio in the world. Unparalleled geographic distribution ensures that the company isn’t overly dependent on one market place. The same holds true for its brands. In light of the recent cold weather and The Walking Dead esque photos coming out of Atlanta, we pulled point-of-sale footwear data for the first 4 weeks ending in 2014.

Athletic footwear in general has been soft to start the New Year. Cold weather brands have benefited and athletic-centric brands have seen their sales slide. WWW’s Merrell, Sperry, and their namesake Wolverine have been outpacing the industry average by a wide margin. Below you can see the difference between WWW’s brands (highlighted in gray) and two of the heavy hitters in Nike’s portfolio and perennial cold weather outperformer Timberland. It’s a great example of how WWW’s brand diversity allows it to capitalize on different macro/weather/trend factors better than just about every footwear player in the marketplace.

ZQK — Over 60% of Quiksilver’s sales are generated outside the US market. While that looks like a incredibly diverse business model at face value, it loses some of its luster when you consider that only 19% of Roxy, Quiksilver, and DC’s sales come from undeveloped markets. That revenue is spread across 82 different countries for an average of $4.3mm per country. What’s even more staggering is that revenues from China total approximately $40mm. Yes China, only accounts for 2% of ZQK’s profits. That market alone is a $400mm opportunity.

ZQK is a global brand, but operating inefficiencies have limited the success of its brands in developing markets. With new management’s rationalized brand portfolio and emphasis on global operating efficiency we believe that the company is in a good position to leverage its strong brands in what have historically been underpenetrated markets.

* * * * * * *

Click on the titles below to unlock the institutional research notes.

Making Sense of Equity Style Factors Year-to-Date

There are three key takeaways in this deep macro dive from analyst Darius Dale:

1) Investors are debating the growth outlook.

2) Our Q1 macro theme #InflationAccelerating is working.

3) Hedge funds are regaining confidence in short selling

WTW: Initiating Short in WeightWatchers

This could be WeightWatcher’s worst winter selling season in the last seven years according to analysts Tom Tobin and Hesham Shaaban. Issues could be secular.

EAT: Blueprint for Success at Brinker

We often articulate our view that EAT is one of the best managed companies in the restaurant space. This morning’s press release and subsequent call merely adds conviction to this belief. It was nothing short of an awesome quarter. Mind you, this performance comes amid a less than favorable macro backdrop and a three-month period in which we suspect the majority of casual dining companies struggled.

![]()

Hedgeye Cartoon of the Week