TODAY’S S&P 500 SET-UP – January 31, 2014

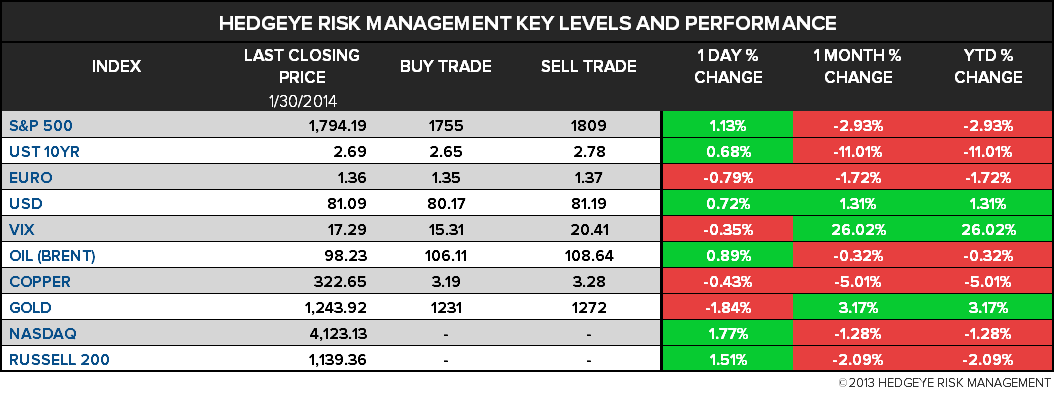

As we look at today's setup for the S&P 500, the range is 54 points or 2.18% downside to 1755 and 0.83% upside to 1809.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.32 from 2.35

- VIX closed at 17.29 1 day percent change of -0.35%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Employment Cost Index, 4Q, est. 0.4% (prior 0.4%)

- 8:30am: Personal Income, Dec., est. 0.2% (prior 0.2%)

- 9:45am: Chicago Purchasing Mgr Index, Jan., est. 59

- 9:55am: U of Mich. Conf, Jan. Final, est. 81.0 (pr 80.4)

- 1pm: Baker Hughes rig count

- 1:15pm: Fed’s Fisher to speak in Fort Worth, Texas

GOVERNMENT:

- Sec. of State John Kerry travels to Berlin for mtgs with German officials ahead of Munich Security Conf

- 9am: President’s Council of Advisors on Science and Technology meets on reproducibility, big data

- 10am: SEC Dodd-Frank investor advisory cmte meets

WHAT TO WATCH:

- MSFT said set to name Nadella CEO, replace Gates at chairman

- Google sales top estimates as retail offsets ad-price drop

- Lenovo said to ask for delayed payment amid Motorola deal rush

- Google looking to buy wearable device cos.: The Information

- Amazon’s boundless spending tested as sales growth slows

- Yahoo identifies effort to break into users’ e-mail accts

- Zynga buys NaturalMotion to boost mobile, is cutting staff

- Keystone report said likely to disappoint opponents on climate

- Euro-area Jan. inflation slows to 0.7% as energy prices drop

- Rowan fighting natural gas well in Gulf of Mexico

- Honda profit misses estimates as demand in Thailand slumps

- LVMH rises most since 2010 on rebound in fashion sales growth

- SEC panel opposes planned test of wider share-price increments

EARNINGS:

- AbbVie (ABBV) 7:51am, $0.82 - Preview

- Aon (AON) 6:30am, $1.51

- Autoliv (ALV) 6am, $1.52

- Avery Dennison (AVY) 8:30am, $0.68

- Booz Allen Hamilton (BAH) 6:30am, $0.33

- Brookfield Office Properties (BPO CN) 7am, $0.14

- Chevron (CVX) 8:30am, $2.57 - Preview

- Consol Energy (CNX) 7am, $0.06 - Preview

- Dominion Resources (D) 7:30am, $0.89

- ImmunoGen (IMGN) 6:30am, ($0.16)

- Lear (LEA) 7am, $1.59

- Legg Mason (LM) 7am, $0.99

- LyondellBasell (LYB) 7am, $1.40

- MasterCard (MA) 8am, $0.60

- Mattel (MAT) 6am, $1.20 - Preview

- Mead Johnson Nutrition (MJN) 7:30am, $0.77

- National Oilwell Varco (NOV) 7am, $1.39 - Preview

- Newell Rubbermaid (NWL) 6:30am, $0.46 - Preview

- Paccar (PCAR) 8am, $0.93

- Simon Property Group (SPG) 7am, $1.22 - Preview

- Tyco International (TYC) 6am, $0.45 - Preview

- Tyson Foods (TSN) 7:30am, $0.64

- WisdomTree Investments (WETF) 7am, $0.12

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Copper Has Longest Losing Streak Since 1998 on China Concern

- RWE Expands in LNG to U.S. Natural Gas as Banks Exit Commodities

- WTI Crude Drops on Speculation Gain to Month-High Was Excessive

- Gold Trades Near 1-Week Low on Outlook for Fed, Physical Demand

- Corn Set for First Monthly Gain Since August as U.S. Sales Climb

- Copper Analysts Are Most Bearish in Year on Fed Tapering, China

- Europe Faces Polar Vortex Flip Side as Power Prices Slide

- U.S. Cattle Herd Shrinking to 63-Year Low Means Record Beef Cost

- Robusta Coffee Climbs to 5-Mo. High on Possible Roaster Buying

- Panama’s $5.3 Billion Canal Expansion Has U.S. Ports Jumping

- Soybean Traders Most Bearish in Four Weeks on Brazil: Survey

- Teapots Boiling in Texas as Shale Spurs Refining Revival: Energy

- Mexico Energy Bill May Draw Private Capital for Infrastructure

- Natural Gas Extends Biggest Decline in More Than Four Years

CURRENCIES

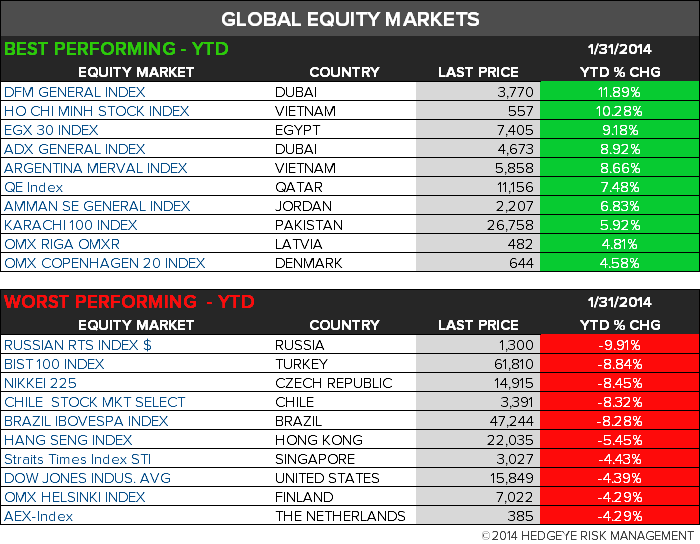

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team