TODAY’S S&P 500 SET-UP – January 30, 2014

As we look at today's setup for the S&P 500, the range is 27 points or 0.97% downside to 1757 and 0.55% upside to 1784.

SECTOR PERFORMANCE

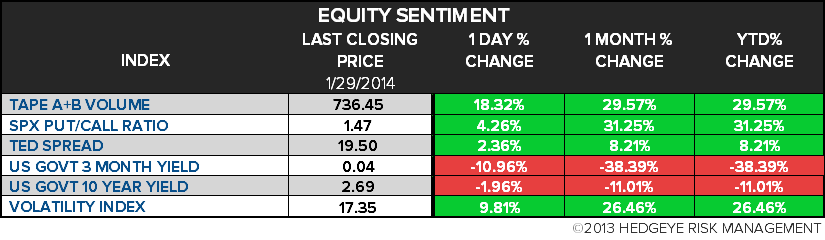

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.34 from 2.33

- VIX closed at 17.35 1 day percent change of 9.81%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Init Jobless Claims, Jan. 25, est. 330k (prior 326k)

- 8:30am: GDP Annualized q/q, 4Q Advance, est. 3.2% (pr 4.1%)

- 9:45am: Bloomberg Consumer Comfort, Jan. 26 (prior -31.0)

- 10am: Pending Home Sales m/m, Dec., est. -0.3% (prior 0.2%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

GOVERNMENT:

- 9:30am: Senate Energy and Natural Resources Cmte meets on whether to end ban on U.S. crude oil exports

- 12:20pm: Obama delivers remarks at GE’s Waukesha Gas Engines plant in Wis.

- 4:15pm: Sen. John McCain, R-Ariz.; Sen. Chris Murphy, D-Conn., speak at CSIS on trans-Atlantic ties

- 4:50pm: Obama in Tenn. for economic opportunity speech

WHAT TO WATCH:

- 4Q U.S. growth probably boosted by stronger spending

- Facebook mobile push fuels bulk of sales to top ests.

- Lenovo to buy Google’s Motorola Mobility for $2.91b

- Google Motorola sale shows limits of Microsoft-Nokia strategy

- Google’s Motorola sale underscores primacy of patent portfolio

- Dassault Systemes offers $750m to acquire Accelrys

- Starbucks CEO Schultz hands daily operations to CFO Alstead

- China’s manufacturing shows first contraction in 6 months

- German joblessness falls more than forecast as economy grows

- Euro-area eco. confidence rises for 9th month on services

- Qualcomm’s profit tops analysts’ ests. on smartphone demand

- Ericsson CEO plans to stay amid interest from Microsoft

- Shell CEO pledges spending cuts, asset sales to restore profit

- Samsung sanctioned by U.S. judge in Apple patent lawsuit

- J&J becomes first drugmaker to open clinical data to academics

- Soros-backed OneWest said to seek buyers as prepares for IPO

- Deutsche Bank suspends NY head of emerging FX trading: Reuters

AM EARNS:

- 3M Co (MMM) 7:30am, $1.62 - Preview

- ADT (ADT) 6am, $0.49

- Airgas (ARG) 7:30am, $1.18

- Alexion Pharmaceuticals (ALXN) 6:30am, $0.84

- Altria Group (MO) 6:58am, $0.58 - Preview

- AutoNation (AN) 6:15am, $0.76

- Ball (BLL) 6am, $0.73

- Bemis Co (BMS) 7am, $0.54

- Blackstone Group LP (BX) 7am, $0.83

- Brunswick (BC) 7:39am, $0.13

- Cameron International (CAM) 7:30am, $0.96 - Preview

- Cardinal Health (CAH) 7am, $0.84 - Preview

- Celgene (CELG) 7:30am, $1.51 - Preview

- CMS Energy (CMS) 7:30am, $0.37

- Colgate-Palmolive Co (CL) 7am, $0.74 - Preview

- ConocoPhillips (COP) 7am, $1.32 - Preview

- Dover (DOV) 7am, $1.27

- Eli Lilly & Co (LLY) 6:30am, $0.73 - Preview

- Enterprise Products Partners L (EPD) 6am, $0.71

- Exxon Mobil (XOM) 8am, $1.91 - Preview

- Franklin Resources (BEN) 8:30am, $0.93

- Harley-Davidson (HOG) 7am, $0.33

- Harman International Industrie (HAR) 7am, $0.94

- Helmerich & Payne (HP) 6am, $1.46 - Preview

- Hershey (HSY) 6:58am, $0.86

- Hillshire Brands Co (HSH) 7:30am, $0.50 - Preview

- Imperial Oil (IMO CN) 7:55am, $0.93 - Preview

- Invesco (IVZ) 7:30am, $0.57

- L-3 Communications Holdings In (LLL) 7am, $1.98

- Manpowergroup (MAN) 7:30am, $1.25

- Northrop Grumman (NOC) 7am, $1.94 - Preview

- Occidental Petroleum (OXY) 7:30am, $1.67 - Preview

- Peabody Energy (BTU) 8am, ($0.10)

- Pitney Bowes (PBI) 6:30am, $0.45

- Potash of Saskatchewan (POT CN) 6am, $0.32 - Preview

- PulteGroup (PHM) 6:30am, $0.45 - Preview

- Quest Diagnostics (DGX) 7am, $0.93 - Preview

- Raytheon Co (RTN) 7am, $1.35 - Preview

- Royal Gold (RGLD) 8am, $0.23

- Sherwin-Williams (SHW) 7am, $1.29

- TECO Energy (TE) 7:30am, $0.20

- Thermo Fisher Scientific (TMO) 6am, $1.38 - Preview

- Time Warner Cable (TWC) 6am, $1.73 - Preview

- Timken Co (TKR) 7:30am, $0.73

- Under Armour (UA) 7am, $0.53 - Preview

- United Parcel Service (UPS) 7:45am, $1.25

- Valley National Bancorp (VLY) 7am, $0.14

- Viacom (VIAB) 6:45am, $1.16 - Preview

- Visa (V) 7:30am, $2.16 - Preview

- Whirlpool (WHR) 6am, $3.03

- Xcel Energy (XEL) 6am, $0.29

- Zimmer Holdings (ZMH) 7am, $1.62 - Preview

PM EARNS:

- Align Technology (ALGN) 4pm, $0.43

- Amazon.com (AMZN) 4pm, $0.69 - Preview

- Broadcom (BRCM) 4:05pm, $0.58

- Canadian National Railway Co (CNR CN) 4:01pm, $0.77 -Preview

- Canadian Oil Sands (COS CN) 5:01pm, $0.48 - Preview

- Celestica (CLS CN) 4pm, $0.23

- Chipotle Mexican Grill (CMG) 4:01pm, $2.52

- Chubb (CB) 4:03pm, $2.04

- CNH Industrial NV (CNHI) 4:44pm, $0.24

- Computer Sciences (CSC) 4:15pm, $0.83

- CR Bard (BCR) 4:05pm, $1.39

- Eastman Chemical Co (EMN) 4:36pm , $1.24

- Google (GOOG) 4:01pm, $12.26 - Preview

- JDS Uniphase (JDSU) 4:05pm, $0.14

- Manitowoc (MTW) 4:25pm, $0.33

- McKesson (MCK) 4:10pm, $1.84 - Preview

- Microchip Technology (MCHP) 4:15pm, $0.61

- NetSuite (N) 4:05pm, $0.07

- PerkinElmer (PKI) 4:05pm, $0.70

- PMC - Sierra (PMCS) 4:05pm, $0.08

- Riverbed Technology (RVBD) 4:05pm, $0.31

- Robert Half International (RHI) 4pm, $0.48

- Validus Holdings (VR) 4:15pm, $1.56

- Wynn Resorts (WYNN) 4:05pm, $1.75

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Aluminum Touches Four-Year Low as China Manufacturing Contracts

- Barclays’s Asia-Pacific Markets Business Said to Lose Eight MDs

- Goldman Sees Gold to Corn Losses After Bear Markets: Commodities

- Gold Horses Lead Chinese Retailers to Profit on Bullion’s Slump

- WTI Rises to Four-Week High as U.S. Chill Boosts Fuel Demand

- Gold Falls on Stimulus, Demand Outlook as Monthly Gain Narrows

- Wheat Recovers From 42-Month Low on Speculation Demand to Build

- Sugar Rebounds as India Fails to Discuss Subsidies; Coffee Gains

- Rubber Near 16-Month Low as Yen Gains After Fed Cuts Bond Buying

- Rebar Caps Worst Monthly Drop in Four on Iron Ore, China Holiday

- Bird Flu Seen by Zhongda Futures Curbing Soybean Demand in China

- Oil, Mining Stocks Face Emerging-Currency Risk: Chart of the Day

- Capital May Shift Toward Gas as Prices Top $5 on Polar Vortexes

- Natural Gas Poised for Biggest Monthly Gain Since 2009

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team