“Emotions are short lived.”

-John Coates

Whereas “a mood is slower, more like a long-term attitude, a background and slow-burning emotion which slants our view of the world” (The Hour Between Dog and Wolf, pg 107).

I don’t know about you, but up until a few weeks ago, my view of the being long stocks was pretty damn bullish. That’s a good thing, because the US and many European stock markets kept hitting all-time highs. Now they aren’t.

And while there was definitely some emotion associated with fear (VIX) ripping +45.8% last week, I’m not so sure consensus is yet in the mood to sell every bounce. Too many bear scars from 2013, and the mood of those stock market bears doesn’t matter on the margin here anyway. It’s the mood of the bears who turned bullish too late that I think matters most.

Back to the Global Macro Grind…

When my man Nouriel Roubini went bullish in December, that definitely got my attention. Then the #OldWall (sell-side economists and strategists) rolled out their bullish US growth and SP500 targets for 2014, and a credible contrarian bear case for US stocks began.

As I pointed out in yesterday’s rant, while he may call the Barron’s Roundtable, god doesn’t call me with a super-secret market multiple for the SP500. There isn’t one. That said, #history fans will note that the stock market’s multiple:

A) Goes UP with #InflationSlowing and Consumption #GrowthAccelerating

B) Goes DOWN with #InflationAccelerating and Consumption #GrowthSlowing

The lowest multiples in post WWII US stock market #history go to the dogmatic Republican/Democrat Keynesian presidential duos of:

- Nixon/Carter

- Bush/Obama

Both duos had bearish US Dollar TRENDs because:

- FISCAL POLICY = spend, spend, spend

- MONETARY POLICY = print, print, print

And, with the Purchasing Power of The People burning (US Dollar DOWN) and #InflationAccelerating, the SP500 traded at 7-11x EPS. Seven times earnings? Yep. Ole Jimmy Carter was a beauty.

I’m not saying the SP500 is going to 7-11x earnings. I’m saying that the probability of the SP500 seeing multiple compression from 16x (instead of consensus multiple expansion) goes up as A) inflation accelerates and B) growth slows.

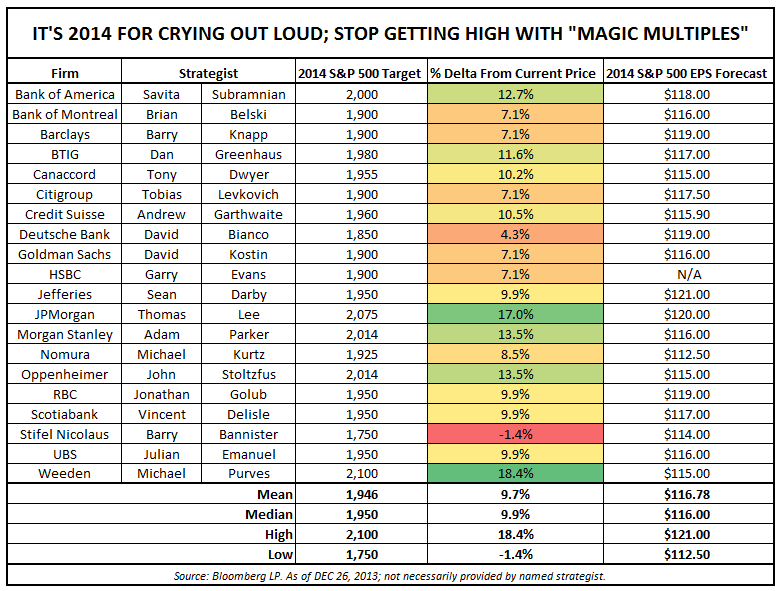

Consensus multiple Expansion? Yep, here’s where my friends wash out on this (after having a mean estimate of 1528 for the SP500 for 2013 – nice call):

- #OldWall mean estimate for 2014 year-end = 1946

- Abby Joseph Cohen = 2088 target for 2014

- Tom Lee = 2075 target for 2014

Then you have the funny guy at Morgan Stanley who had the SP500 target of 1434 in 2013 (Adam Parker) who takes himself very seriously with his 2,014 SP500 target for, uh, 2014. It’s a good thing the sell-side has learned from 2008 and evolved…

The #OldWall’s magic-multiple thing is based on a consensus estimate for SP500 earnings of around $117/share. Tom Lee is up at $120, so he slaps a 17x “multiple” on that. Meanwhile Abby goes with the 18x, and there you have it – tah-dah!

But what if they are wrong on growth, inflation, and the SP500 earnings numbers? That’s when the consensus poop hits the fan. So watch out for stepping in that. Bear Droppings can ruin your bullish mood.

What about that Hedgeye Macro Theme #1 (#InflationAccelerating)?

- CRB Index (19 Commodities) was up another +0.8% yesterday (with the SP500 -1%) to +1.7% YTD

- Natural Gas Prices (for those of you who don’t live in a government hotel) = +30.3% YTD

- Oats (yes, I eat Oatmeal, every day!) = +18.9% YTD

So the other Goldman guy who is running the NY Fed now (Dudley) eats iPads and I eat oatmeal. No one cares. What Mr. Macro Market cares about is the 2nd derivative move – the slope of the line – the rate of change! And the fact of the matter is that #InflationAccelerating right now alongside US Consumption #GrowthSlowing is bearish for consumer stocks.

That’s a big reason why US Consumer Discretionary stocks (XLY) are -6.2% YTD and why the US stock market (SPX) is -4.0% YTD vs the CRB Index +1.7%. Dollar Down, Rates Down = Stocks Down. God called me on that too – it’s called a real-time US GDP #GrowthSlowing signal, and America’s mood will be changing if it becomes a reflexive one.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.67-2.80%

SPX 1

VIX 14.91-20.39

EUR/USD 1.35-1.37

Nat Gas 4.79-5.49

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer