The weather, expiration of investment tax credits, exclusion of commercial aircraft orders in the advance estimate (Boeing orders that will probably show up in the Jan data) and seasonality will all be held out as potential distortions in the December figures.

With Durable Goods being one of the more volatile series, subject to significant revision, and negatively diverging from the ISM mfg data for December, we may indeed see a positive revision and sequential acceleration next month, but the reality is that the deceleration reflected in this morning’s durables data agrees with the sequential slowdown observed more broadly across the domestic macro data.

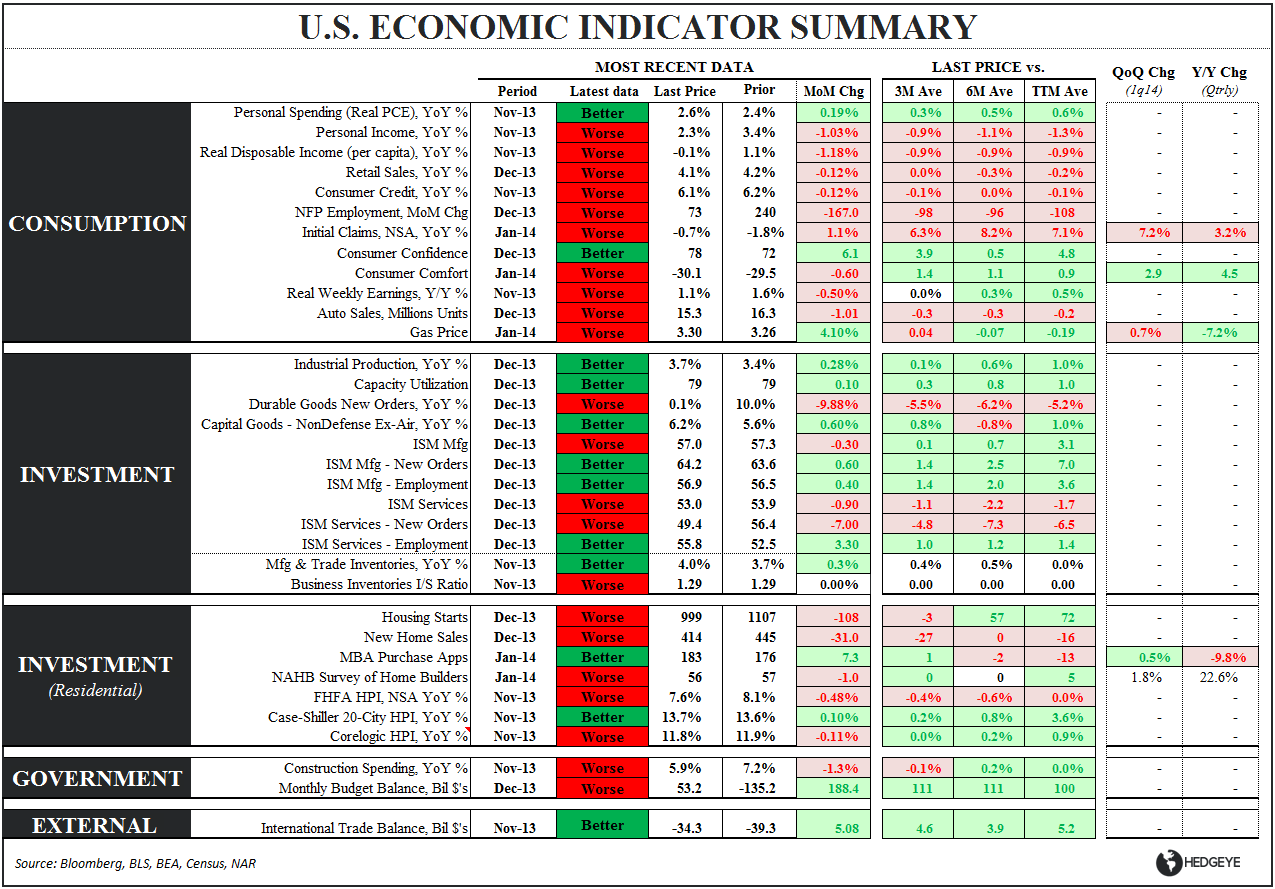

Headline Durable Goods printed its worst number in five months, accelerating to the downside sequentially with New Orders declining -4.3% MoM while decelerating meaningfully on both a YoY and 2Y basis.

Core Capex Orders growth accelerated to the downside as well, declining -1.3% MoM and >300bps on a 2Y. If there was a lone positive in the release, it’s that core capital goods orders growth did accelerate 70bps sequentially to 6.2% from +5.6% in November.

Additionally, both headline New Orders and Core Capex figures for November were revised lower by -80bps and -150bps, respectively.

No silver linings to be had in the sub-aggregates either with (perhaps) the cleanest read on household consumerism - New Durable Goods Orders Ex-Defense & non-defense Aircraft - decelerating on a MoM, 1Y and 2Y.

In short, today’s durable goods data agrees with our expectation for a sequential slowdown in domestic growth and suggests some emergent weakness in what has been a key source of macro strength over 2H13 (with wage inflation still muted and services consumption growth flagging).

As we highlighted in our 1Q14 Macro themes call (HERE), easy 1H14 inflation comps and our expectation for a deceleration in the rate of change in reported growth has us incrementally more cautious on U.S. equities than we have been over the TTM.

Now, with the risk management/price signals flashing red with a breakout in equity volatility above TREND resistance and the S&P500 flirting with a TREND breakdown (SPX Trendline = 1779), in the more immediate term, we’ll keep our net exposure to domestic equities relatively tight.

Christian B. Drake

@HedgeyeUSA