Summary:

While the bonfire that is emerging market currencies keeps burning, the systemic interbank risk measures in the US, Europe and China remain benign (for now). TED Spread, Euribor-OIS and Shifon are all less impressed with what's happened thus far in Argentina, Turkey and elsewhere. Fundamentally speaking, history has shown that when these interbank measures show little sign of alarm it has historically indicated a good time to take advantage of fear/weakness. Tactically speaking, however, be mindful that the Hedgeye TREND line of support on the XLF is $21.01 and we'd be cautious about buying weakness in a broken TRADE/TREND environment.

Key Points:

* XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 2.7% upside to TRADE resistance and 0.5% downside to TREND support. The important line in the sand here is the TREND line of support at $21.01.

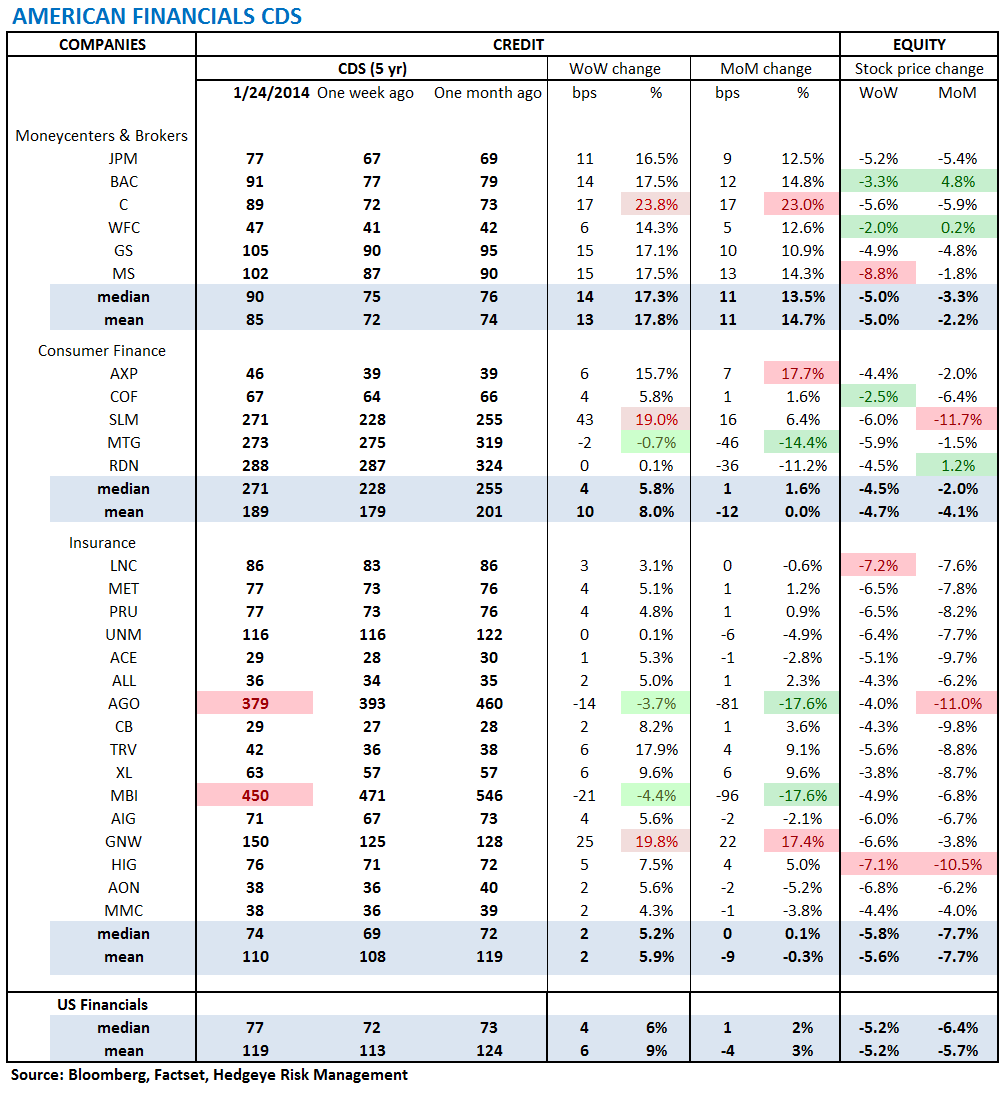

* U.S. Financial CDS - Large cap US banks saw their credit default swap spreads widen sharply last week on the growing concerns around emerging market risk and potential for contagion. Citi saw the biggest move, rising 17 bps to 89 bps. GS and MS were close behind, up 15 bps apiece. While spreads widened almost across the board, the domestic-focused banks were predictably less impacted.

* 2-10 Spread – Last week the 2-10 spread tightened a further 7 bps to 238 bps. In the past month it has compresed 20 bps.

* Euribor-OIS Spread – The Euribor-OIS spread tightened by 1 bps to 11 bps.

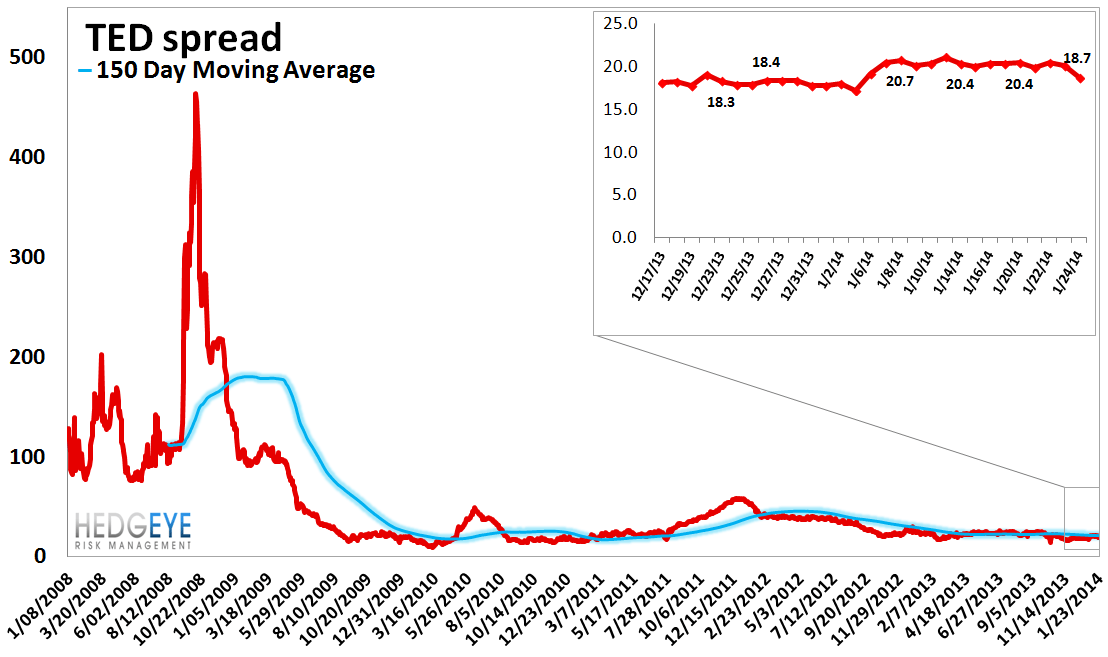

* TED Spread – The TED spread fell 1.7 basis points last week, ending the week at 18.7 bps this week versus last week’s print of 20.36 bps.

* High Yield (YTM) Monitor – High Yield rates rose 11.7 bps last week, ending the week at 5.95% versus 5.83% the prior week.

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 7 of 13 improved / 1 out of 13 worsened / 5 of 13 unchanged

• Intermediate-term(WoW): Negative / 4 of 13 improved / 5 out of 13 worsened / 4 of 13 unchanged

• Long-term(WoW): Positive / 5 of 13 improved / 0 out of 13 worsened / 8 of 13 unchanged

1. U.S. Financial CDS - Large cap US banks saw their credit default swap spreads widen sharply last week on the growing concerns around emerging market risk and potential for contagion. Citi saw the biggest move, rising 17 bps to 89 bps. GS and MS were close behind, up 15 bps apiece. While spreads widened almost across the board, the domestic-focused banks were predictably less impacted.

Tightened the most WoW: MBI, AGO, MTG

Widened the most WoW: C, GNW, SLM

Tightened the most WoW: AGO, MBI, MTG

Widened the most MoM: C, AXP, GNW

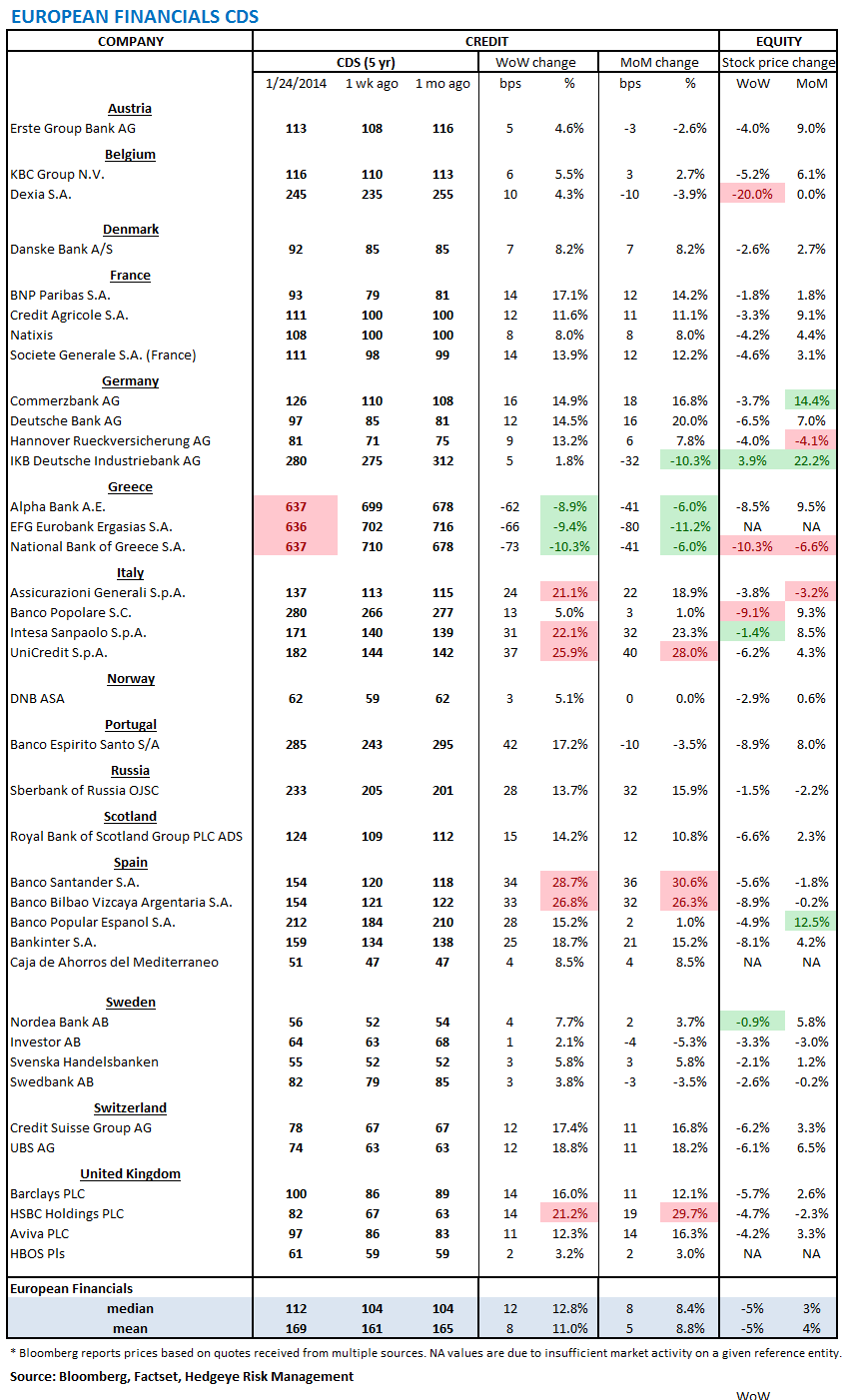

2. European Financial CDS - Swaps were sharply higher across Europe's banks last week. UK banks fared equally poorly alongside their French, German, Spanish and Italian counterparts.

3. Asian Financial CDS - Chinese bank swaps were up sharply last week, extending the month-over-month trend.

4. Sovereign CDS – Sovereign swaps widened almost across the board last week with the biggest moves occurring in Portugal and Italy (+25 and +19 bps). Meanwhile, the US and Germany were unchanged at 28 and 23 bps, respectively.

5. High Yield (YTM) Monitor – High Yield rates rose 11.7 bps last week, ending the week at 5.95% versus 5.83% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index was unchanged last week at 1850.

7. TED Spread – The TED spread fell 1.7 basis points last week, ending the week at 18.7 bps this week versus last week’s print of 20.36 bps.

8. CRB Commodity Price Index – The CRB index rose 1.7%, ending the week at 283 versus 278 the prior week. As compared with the prior month, commodity prices have decreased -0.1% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

9. Euribor-OIS Spread – The Euribor-OIS spread tightened by 1 bps to 11 bps. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose an impressive 88 basis points last week, ending the week at 3.7% versus last week’s print of 2.82%. That said, the index remains down on a month-over-month basis and is still nowhere near its mid-2013 high of over 13%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Markit MCDX Index Monitor – The muni market seems relatively unfazed by what's going on in emerging markets. Last week, MCDX spreads were unchanged at 77 bps. The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. We track the 16-V1.

12. Chinese Steel – Steel prices in China fell 0.5% last week, or 16 yuan/ton, to 3,403 yuan/ton, but have fallen 1.9% in the past month and as the chart below shows the trend is down and rather linear. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened a further 7 bps to 238 bps. In the past month it has compresed 20 bps. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 2.7% upside to TRADE resistance and 0.5% downside to TREND support. The important line in the sand here is the TREND line of support at $21.01.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT