This note was originally published at 8am on January 10, 2014 for Hedgeye subscribers.

“One friend in a lifetime is much; two are many; three are hardly possible. Friendship needs a certain parallelism of life, a community of thought, a rivalry.”

-Brooks Adams

As many of you may have noticed already, my colleagues and I have a bit of a fascination with the sport of hockey. In particular, Ivy League hockey, since many of us played at Yale (and our firebrand energy analyst Kevin Kaiser played at Princeton). So, if you will, please tolerate my enthusiasm for just a minute here as this weekend is effectively our Super Bowl.

Specifically, this Saturday at 8pm Yale will be playing Harvard at Madison Square Garden. In as much as I would like to wish my friends at Harvard good luck this weekend, I would, honestly, not really mean it. But I sincerely do hope the Crimson don’t totally embarrass themselves, or next year we will have to invite Cornell to play us on the world’s biggest hockey stage.

Now admittedly Harvard did once win a NCAA championship, albeit it was more than three decades ago. On the other hand, Yale is the defending NCAA champion and over the last five years has amassed a record of 111 – 53 – 12. Over the same period, Harvard hockey is 53 – 87 – 24. As if having Larry Summers on their team wasn’t bad enough... ;)

In Malcolm Gladwell’s new book, “David and Goliath”, he digs into the idea that underdogs do disproportionately well in competition. He cites a study from political scientists Ivan Arreguin-Toft that looked at all wars between small countries and much larger countries over the past two hundred years. He found that the much larger country only win 71.5% of the time. Further as Gladwell writes:

“What happens in wars between the strong and the weak when the weak side does as David did and refuses to fight the way the bigger side wants to fight, and instead uses unconventional or guerilla tactics. The answer: in those cases the weaker party’s winning percentage climbs from 28.5% to 63.6%. To put that in perspective, the United States population is ten times the size of Canada’s. If the two countries went to war and Canada chose to fight unconventionally, history would suggest you ought to put your money on Canada.”

So, who knows, if Harvard hockey were to do something totally unconventional, like say put their football team on skates, maybe they will have a chance this weekend!

Back to the Global Macro Grind...

Yesterday, Keith presented our top three global macro themes for Q1 2014. Like clockwork, we’ve been doing these themes for the last five years. Those three themes are as follows:

- #InflationAccelerating – CPI comparisons globally are easy and commodities are basing, as a result we are expecting a re-acceleration in reported inflation. From a sector perspective, the three sectors we like in this scenario are technology, healthcare and energy;

- #GrowthDivergences – This could be the year in which global growth divergences increasingly matter for stocks, especially as rates begin to normalize, and Europe looks set up to see accelerating economic growth. Conversely, we are starting to question whether Japan’s recovery is losing steam; and

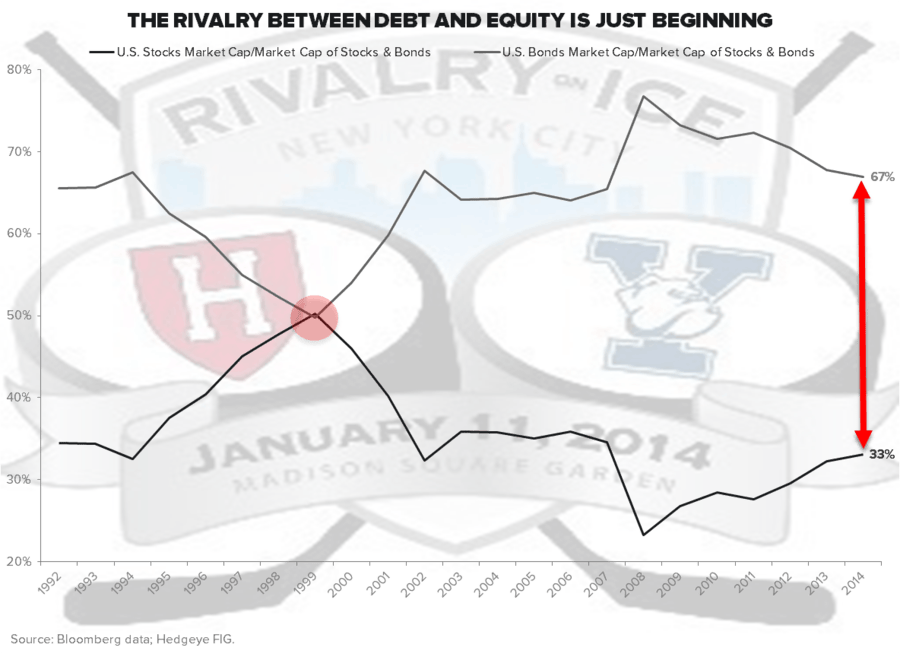

- #FlowShow – In a world in which 75% of the global financing stock outstanding is in debt, there is a lot money that can flow out of bonds and into equities. In the Chart of the Day below, we again emphasize that the ratio of debt-to-equity was 50/50% in 1999.

One key supporting point for the idea that Europe could well be the global growth leader, at least on a percentage change basis, is the fact the European sovereign debt markets have all but recovered. Remember that sovereign debt crisis from a few years ago? Well, the European credit markets barely do.

This morning the Spanish 10-year yield is trading at 3.70%. This is a mere 74 basis points wider than the U.S. 10-year yield. In fact, last night Spain kicked off its funding program and raised $7.2 billion in five year debt, overshooting its target. Further, this debt was sold at 2.411%, which was the lowest funding rated of the Euro era for Spain.

Now in the long run, the Spanish economy still has excesses built up from the parabolic housing bubble it experienced. Nonetheless, in the short run as the likes of Spain, Italy, France and Portugal are able to sell debt at reasonable rates, this is both a real positive for their governments and their governments’ ability to spend, but more importantly for banks. As broad borrowing rates go down, this will eventually filter back to corporations who can then borrow at low rates to more aggressively fund capital expenditures and expand.

Since we are on the topic of housing, I should flag that the U.S. housing market is at the top of our list for worries as it relates to the U.S. economy. In fact, mortgage applications are down 22% from their 2014 peak reading.

Even if it’s not clear yet that housing headwinds will derail the U.S. economy, it is setting up for some interesting short ideas. In particular, our Financials team just added Nationstar Mortgage (NSM) to our Best Ideas list this week. Previously, this had been a top long idea for us, which played out well as our earnings estimates were higher than the consensus.

Conversely, our view is now that the consensus earnings estimate of north of $5 for 2014 could come in as low as $1.

Now, how’s that for a downside surprise?

We are doing a deep dive on the name and will outline the thesis this Monday at 11am EST. (Email sales@hedgeye.com to subscribe for access.) NSM trades more than $30 million in volume per day, so there’s lots of stock out there to short, especially if you believe our Financials team that the best case scenario is that the stock will get cut in half.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research