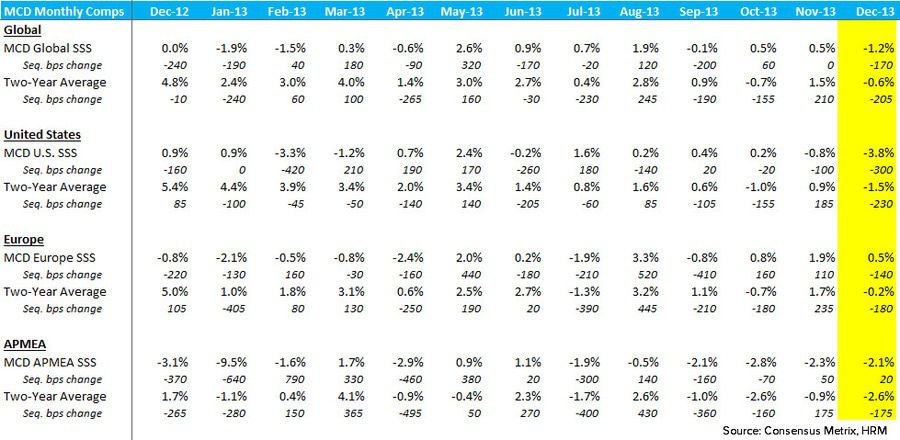

McDonald’s reported mediocre 4Q13 results this morning, as revenues ($7.093B) and global comp sales (-0.1%) missed expectations of $7.106B and +0.5%, respectively. EPS, however, surprised to the upside ($1.40) versus expectations of $1.39. 4Q was highlighted by disappointing performance across the board, save for Europe, which delivered respectable comp sale growth led by strength in France, the UK and Russia. December was the weakest month in 4Q, highlighted by disappointment in every region.

4Q Same-Store Sales

- Global: -0.1% vs +0.5% (consensus estimate)

- United States: -1.4% vs -0.2% (consensus estimate)

- Europe: +1.0% vs +1.1% (consensus estimate)

- APMEA: -2.4% vs -1.3% (consensus estimate)

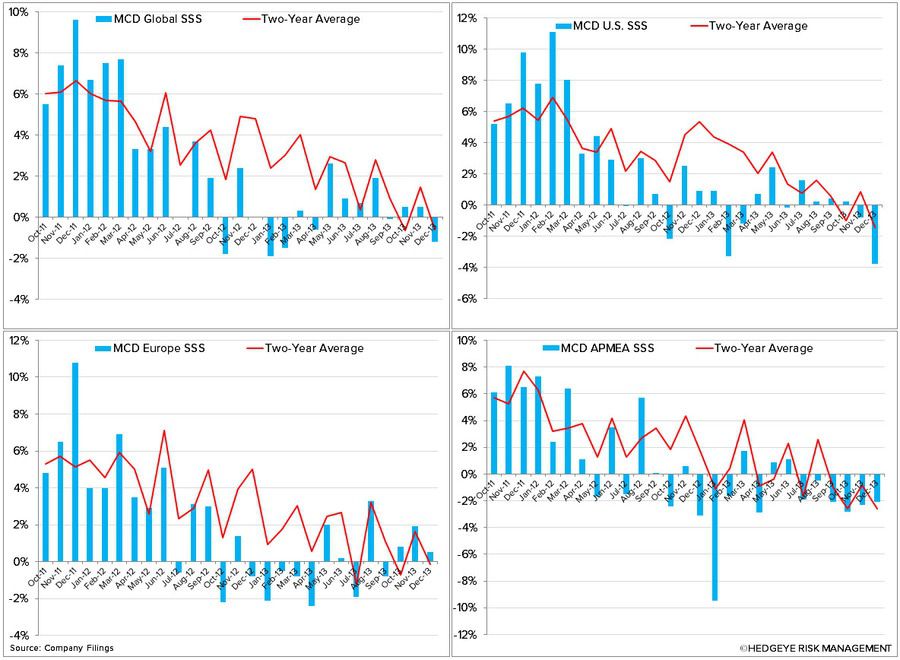

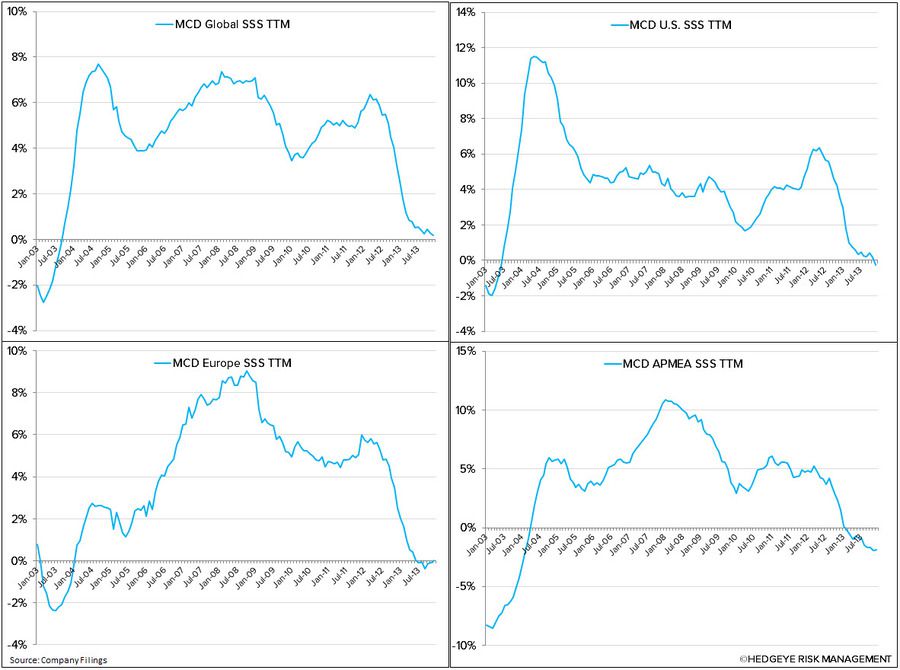

Overall, 2013 proved to be another subpar year for MCD as the company only managed to grow EPS by 3% on 2% revenue growth. As management reiterated several times on the call, top line sales are critical to driving continual margin improvement and to the overall health of the business. This growth has been difficult to come by, however, as full year global comp sales (+0.2%) missed expectations of +0.5%. After a less than stellar two years, it is no surprise that global same-store sales continue to decline on a two-year basis.

We have been bearish on MCD for quite some time now and continue to believe the company has issues in its underlying, core business. While we believe management has realized they have problems, we have little faith that they have found the proper solutions.

To their credit, they have been proactive in their attempt to reverse the current downward momentum of the business. To this extent, they recently introduced a number of initiatives (Dollar Menu and More, new refrigerators, high density prep tables, additional drive thru windows) to operationally “enhance” the U.S. business. However, these initiatives are not guaranteed to improve operations and, in fact, could negatively impact the business.

Franchisees have voiced their discontent with the Dollar Menu and More, noting that it provokes customers to order multiple, smaller margin, products rather than a single, higher margin, product. This tends to slow service times. Another complaint is menu complexity. We have called for MCD to simplify their menu multiple times. This would not only help customers order meals quicker and help the kitchen deliver the food faster, but also improve speed of service, the guest experience and franchisee morale. Instead, MCD continues to try to be all things to all people. This desire has led to the manifestation of high density prep tables which are being put in place, at least hypothetically, to organize the kitchen, allow for additional customization, and speed service times. How those last two points correlate, however, is lost on us. We think this level of customization could in fact slow production times – a concern that has been shared by multiple franchisees. We questioned management on this point during the earnings call, to which they pointed out that the additional capacity would help organize the kitchen by keeping employees relatively stationary and eliminating cluster. Although we could be wrong, this response did not do much to allay our concerns.

We often hear the bulls refer to MCD’s structural advantages (global footprint, strong asset base, significant FCF generation, etc) in support of the stock. While these are important, they shouldn’t give anyone reason to ignore a slowing top line. The fact of the matter is, the street is still too bullish on McDonald’s in 2014. The company delivered 2% and 3% EPS growth on 2% and 2% revenue growth in 2012 and 2013, respectively. What would make anyone believe they will deliver 7% EPS growth on 5% revenue growth in 2014? Personally, we do not have enough confidence in the sales drivers management has in place to make this leap of faith.

When we look at the overall business, we see a challenged top line that has shown zero signs of improvement, declining traffic, shrinking margins, and a diminishing competitive advantage. With that being said, we believe 2014 expectations will be revised down over the course of the year and lead to multiple contraction.

Howard Penney

Managing Director